.svg)

The Kroger Co. has come a long way from its humble beginnings as a single grocery store in downtown Cincinnati, Ohio, in 1883. Today, the brand operates over 2,700 stores under its numerous grocery store banners.

We analyzed the visitation patterns at some of Kroger’s largest chains to see how these brands have fared over the past few months, and looked at what last year’s visit data can tell us about the upcoming Thanksgiving holiday.

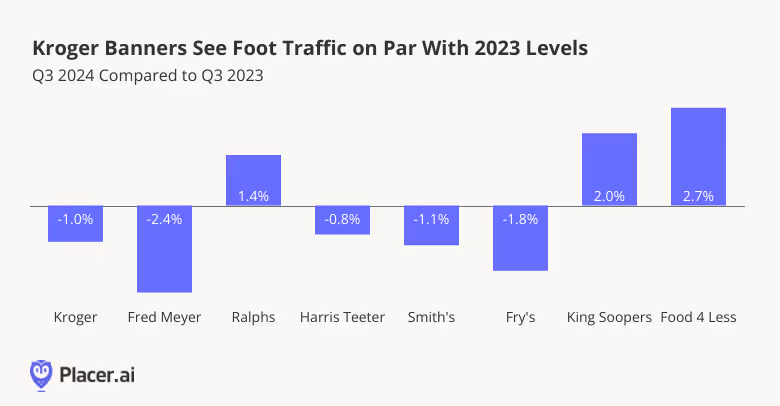

Visits To Kroger Banners Show Stability in Q3

The Kroger Co.’s various grocery banners vary in size and scale, with its eponymous banner Kroger – more than 1200 stores across much of the midwest and south – attracting the largest visit share relative to the company’s full grocery portfolio. Kroger’s other major regional chains, including Harris Teeter (mid and south atlantic states); Ralphs (California), King Soopers (primarily Colorado), Food 4 Less (California, Illinois, and Indiana), Smith’s (Mountain states), Fry’s (Arizona), and Fred Meyer (Pacific northwest), lend the company considerable presence nationwide.

On the whole, visits to the analyzed Kroger chains remained fairly close to 2023’s levels, with visits to Kroger, Fred Meyer, Harris Teeter, Smith’s, and Fry’s sustaining minor YoY visit gaps. No-frills value chain Food 4 Less enjoyed 2.7% YoY visit growth in Q3, likely buoyed by the same trading down behaviors that have propelled growth at other low-cost supermarkets this year. Ralphs and King Soopers also saw YoY visit growth, perhaps aided by California and Colorado’s relatively high median household incomes (HHIs) – $94.1K and $89.1K, respectively, according to data from STI: PopStats, compared to the nationwide baseline of $76.1K.

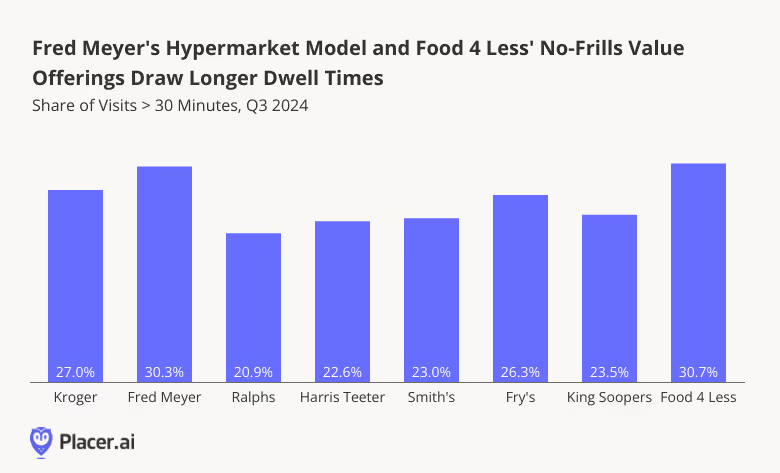

Shoppers Lingering at Discount, Hypermarket Options

Kroger’s extensive reach allows it to appeal to a wide range of grocery shoppers. The company operates both discount grocery chains, such as Food 4 Less, more upscale ones like Harris Teeter, and everything in between.

Diving into the share of visits lasting 30 minutes or longer at individual Kroger banners reveals substantial variation, with Fred Meyer and Food 4 Less receiving the highest shares of long visits among the analyzed chains. In Q3 2024, 30.3% of Fred Meyer visits and 30.7% of Food 4 Less visits lasted over 30 minutes – a stark contrast to Ralphs (20.9%), Harris Teeter (22.6%) and King Soopers (23.5%).

This variance in dwell times may reflect the differing offerings of each chain. Hypermarket Fred Meyer provides a wide range of services beyond groceries – including pharmacies, department stores, and jewelry offerings – which could encourage shoppers to spend more time exploring. And Food 4 Less falls squarely into the discount grocery segment, one that often sees customers spending more time in-store searching for the best deals.

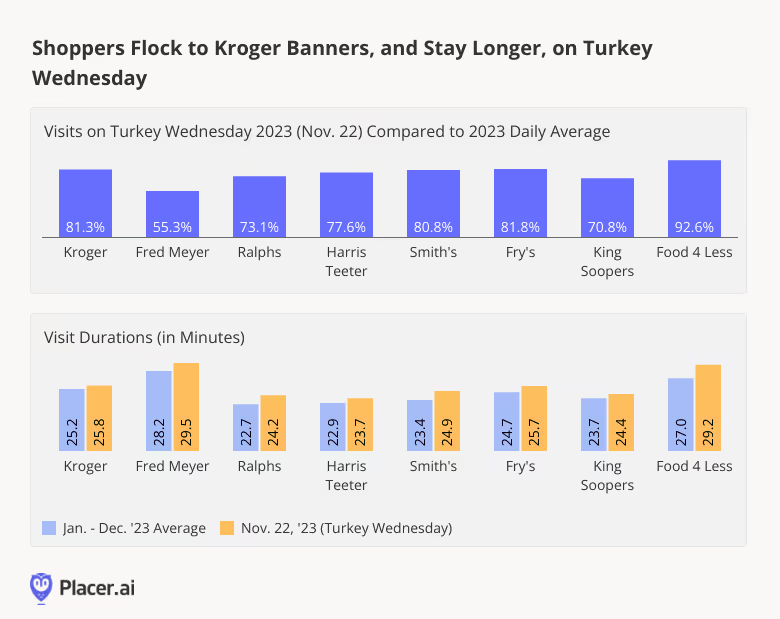

Turkey Wednesday Poised to Bring the Crowds

While not (yet!) an official holiday, Turkey Wednesday – the day before Thanksgiving – is one of the most important days of the year for grocers as shoppers flock to stores to pick up last-minute items for their upcoming feasts.

And while Thanksgiving is still over a week away, analyzing trends from previous years can help grocers prepare for the coming frenzy. On November 22nd, 2023 – the day before Thanksgiving – visits across all analyzed Kroger chains shot up between 55.3% and 92.6% compared to the daily visit average for 2023. And visitors at each of the chains stayed longer in-store than they typically did during the rest of the year.

With visits to Kroger’s major banners either nearly on par with or ahead of last year’s levels, the company appears well-positioned to enjoy another year of strong Turkey Wednesday visits.

Final Thoughts

If previous years are any indication, Kroger’s grocery banners should be preparing for a surge in Thanksgiving shopping. Will visits outpace those of last year?

Visit Placer.ai to keep up with the latest data-driven grocery insights.

.avif)