.svg)

With sales exceeding $148 billion in 2023, The Kroger Co. is a leading player in the grocery store space. In addition to its flagship eponymous brand, the company owns a variety of regional banners, including (among others) Fred Meyer, Harris Teeter, Ralphs, Smith’s Food and Drug, Fry’s Food Stores, King Soopers, and Food 4 Less.

We dove into the data to see how key Kroger chains are faring in 2024 – and to explore the different audiences served by the company’s varied portfolio.

Setting the Stage: A Portfolio Breakdown

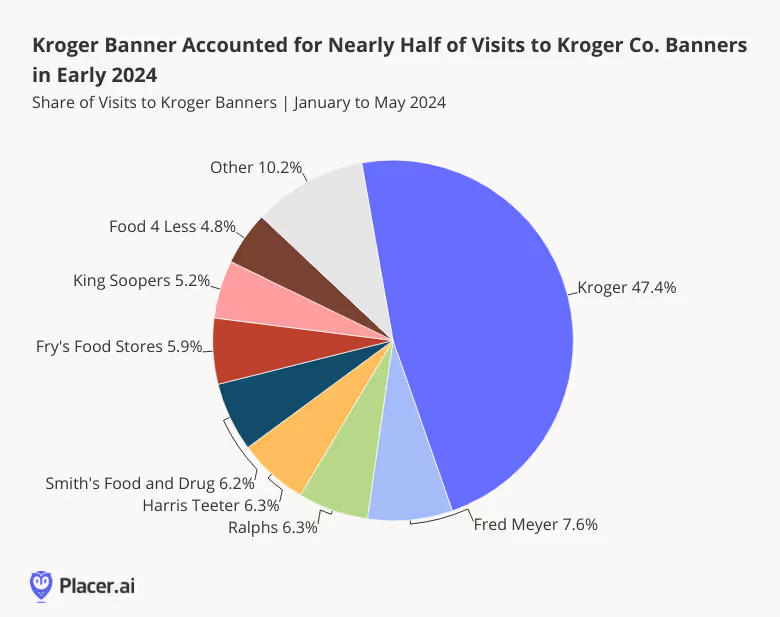

With some 1255 locations across 19 states, Kroger is The Kroger Co.’s largest grocery banner by far. And between January and May 2024, visits to the chain accounted for 47.6% of overall foot traffic to the company’s grocery portfolio. The remaining 52.4% of visits went to The Kroger Co.’s smaller banners – with Fred Meyer, Ralphs, and Harris Teeter leading the charge.

A Regional Deep Dive

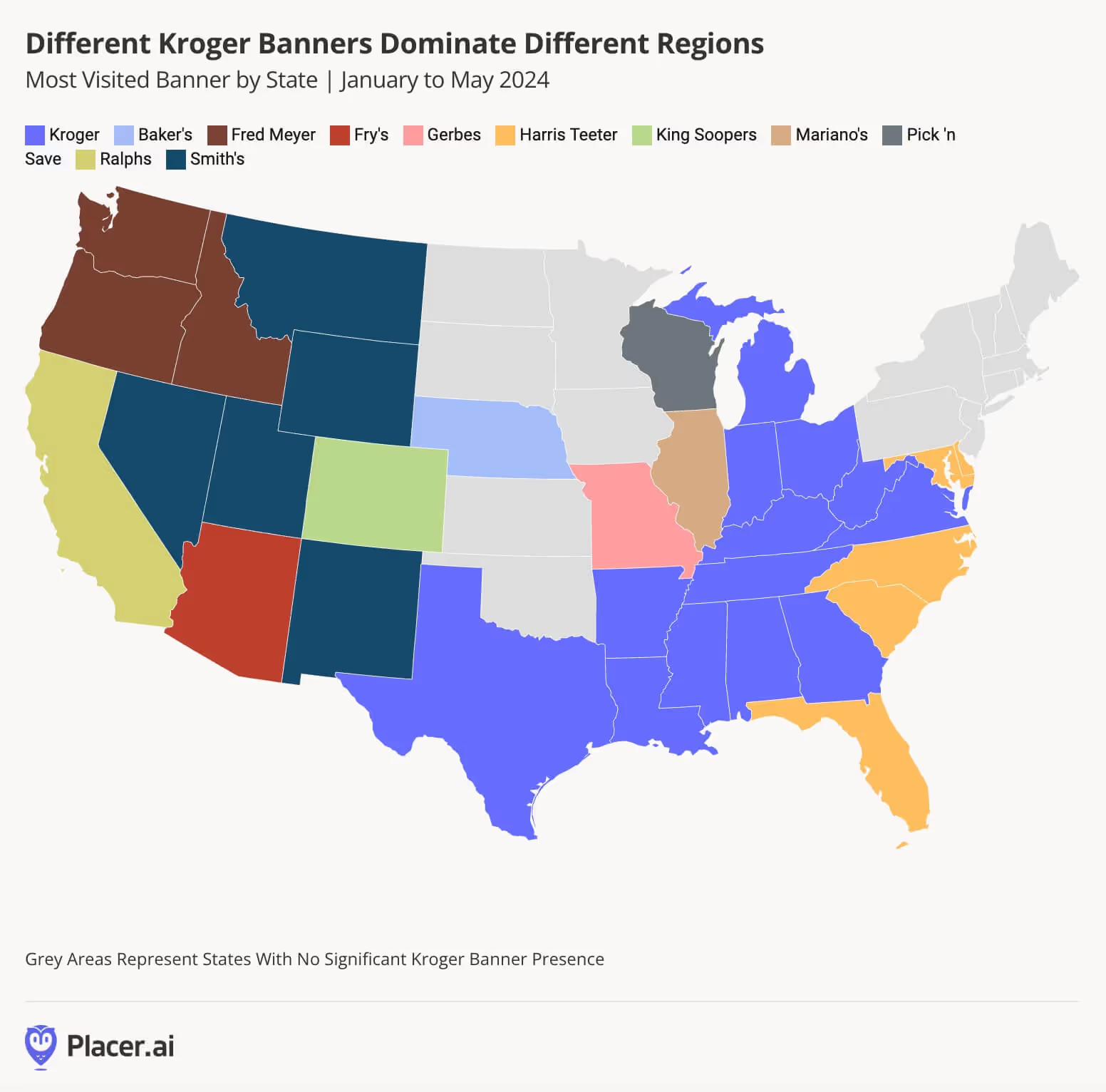

And drilling down deeper into the regional distribution of the company’s various grocery banners shows that each chain serves a different area of the country.

Kroger’s eponymous banner holds sway throughout much of the Midwest and South – while Harris Teeter serves shoppers in Maryland, Florida, and the Carolinas. Meanwhile, Fred Meyer, Smith’s, Ralphs, Fry’s, and King Soopers dominate the Western United States. And throughout some parts of the Midwest, Kroger draws consumers with a variety of smaller banners.

Like that of Albertsons, Kroger Co.’s strategy of acquiring and maintaining regional brands has allowed the company to expand its footprint across the country – while catering to the needs and preferences of local shoppers. Indeed, Kroger’s footprint now extends across three of the four U.S. regions – the West, South, and Midwest – with only the Northeast lacking a Kroger Co. presence.

Visits on the Rise

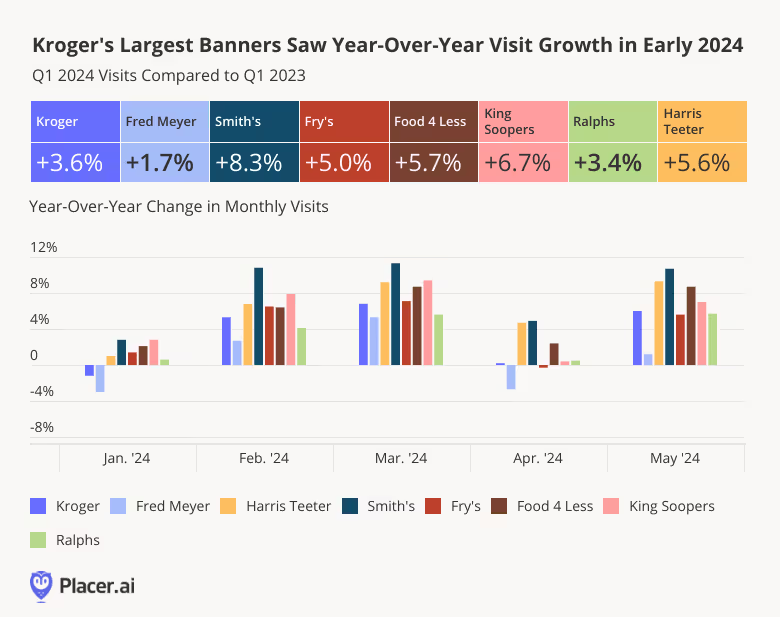

A look at recent visitation trends for Kroger Co.’s largest banners – i.e. those with at least 100 locations – shows that all experienced positive YoY visit growth in Q1 2024. The most impressive foot traffic bumps were seen by Mountain region banners Smith’s and King Soopers, followed by value-oriented Food 4 Less, and the South Atlantic-focused Harris Teeter.

On a monthly basis, too, The Kroger Co.’s major Banners saw nearly uniform YoY visit growth between January and May 2024.

Reaching Different Audiences

Analyzing demographic differences among the trade areas of Kroger’s different chains shows how the company leverages its portfolio of banners to serve distinct customer bases.

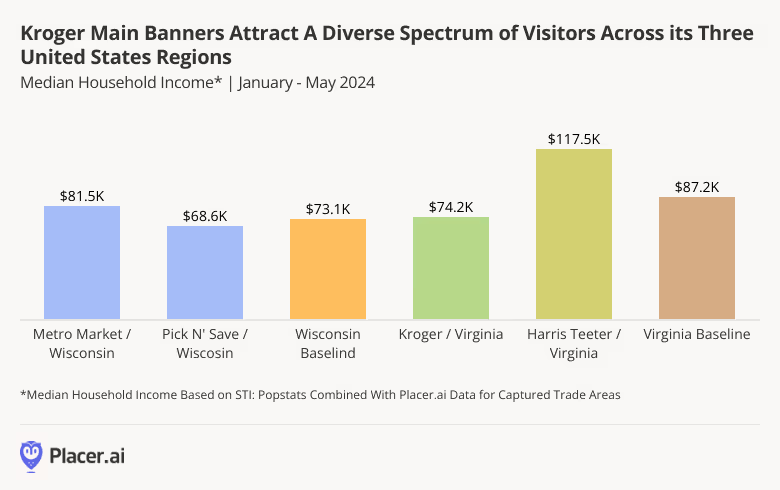

Virginia, for example, is served by two Kroger Co. banners – Kroger and Harris Teeter. And while the former draws shoppers from areas with a median HHI below the statewide baseline of $87.2K, the latter – with somewhat more upscale, pricier offerings – attracts a much more affluent audience. Similar differences can be observed in Wisconsin – where Pick ‘n Save and Metro Market serve different demographics.

By offering a diverse spectrum of shopping experiences, The Kroger Co. strategically positions itself to maximize market penetration and appeal to a broad range of consumers.

Looking Ahead

The Kroger Co. entered 2024 with a bang. With its extensive reach and adaptive approach, can the grocery leader maintain its positive momentum throughout the rest of the year?

Visit our blog at Placer.ai to find out.

.avif)