.svg)

Pandemic restrictions ushered in a new age of remote work that slashed commuting and office-wide coffee orders. But the coffee space has adapted to changing consumer behavior, and category leaders – Starbucks, Dunkin’, and Dutch Bros. Coffee – have found success in the new normal.

With Q1 2024 in the rearview mirror, we took a closer look at how visitation to the coffee space has changed since the pandemic.

Key Takeaways

- Since 2019, Starbucks, Dunkin’, and especially Dutch Bros. have expanded their footprints – driving their pandemic recovery.

- Year-over-year visits to the coffee leaders are also on the rise, indicating that the space is continuing to grow.

- Starbucks, Dunkin’, and Dutch Bros each have a unique hourly visitation pattern, suggesting that – despite the apparent crowding in the coffee space – coffee demand is varied enough to sustain multiple major players.

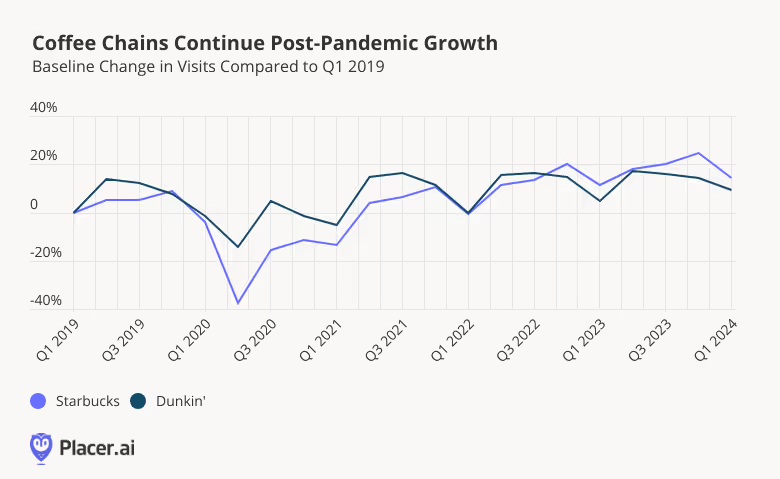

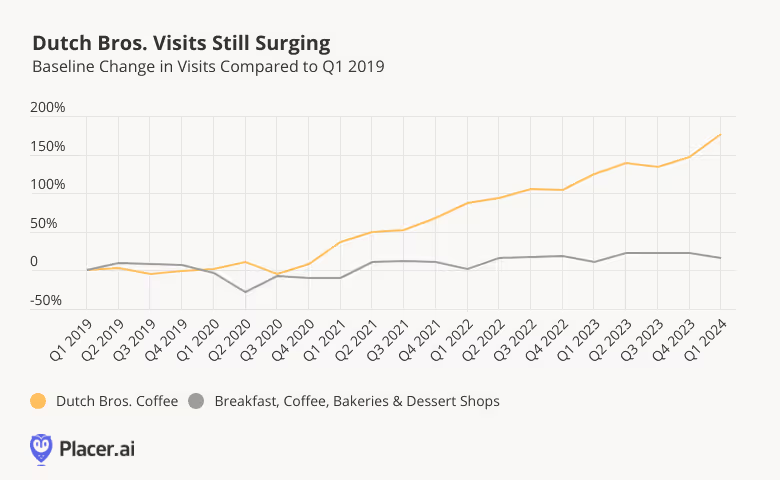

Coffee’s Recovery Since COVID

Over the last few years, Starbucks, Dunkin’, and Dutch Bros have expanded their footprints, helping drive visits in a turbulent retail environment. Notably, visits to all three chains have remained above pre-pandemic levels nearly every quarter since Q2 2021, signifying a rapid and robust foot traffic recovery for the space.

Starbucks and Dunkin’ have both implemented expansion plans recently, with Starbucks focusing on smaller-format stores and Dunkin’ going after non-traditional sites such as airports, universities, and travel plazas. The store fleet growth likely contributed to both chains’ visit increases – in Q1 2024, foot traffic to Starbucks and Dunkin’s was up 14.5% and 9.5%, respectively, compared to Q1 2019.

Meanwhile Dutch Bros.’ physical footprint has grown exponentially since 2019, and the chain is now working on developing its digital footprint, including the rollout of mobile ordering.The company’s aggressive expansion contributed to Dutch Bros.’ significantly elevated visits in Q1 2024 – 177.6% above the Q1 2019 baseline. (The chain’s considerably larger year-over-five-year visit increases compared to Starbucks and Dunkin’ can be attributed to Dutch Bros.’ substantially smaller starting footprint, so that every opening brings a larger visit boost to the chain as a whole.)

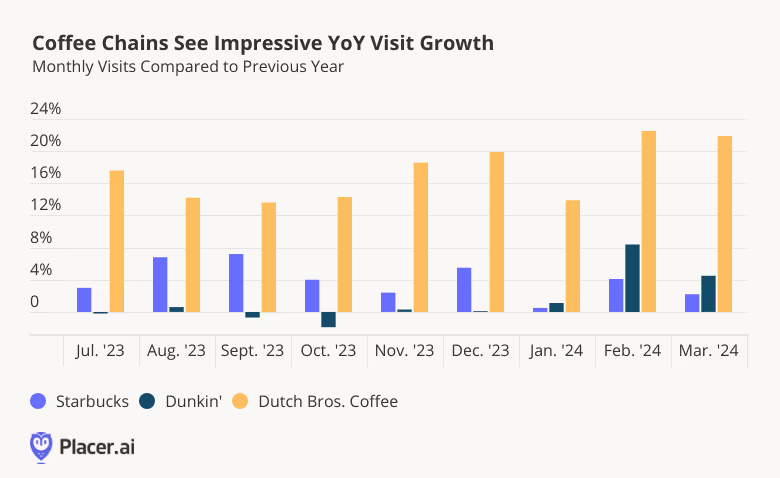

Monthly Momentum for Coffee Leaders

Zooming in on visits since the halfway point of 2023 shows that the coffee space’s post-pandemic momentum continued in recent months, with year-over-year (YoY) monthly visits to all three chains positive since the beginning of 2024.

Dutch Bros.’ ongoing aggressive expansion once again gave the Oregon-based chain the largest year-over-year boost, and Starbucks and Dunkin’ also sustained YoY visit growth nearly every month.

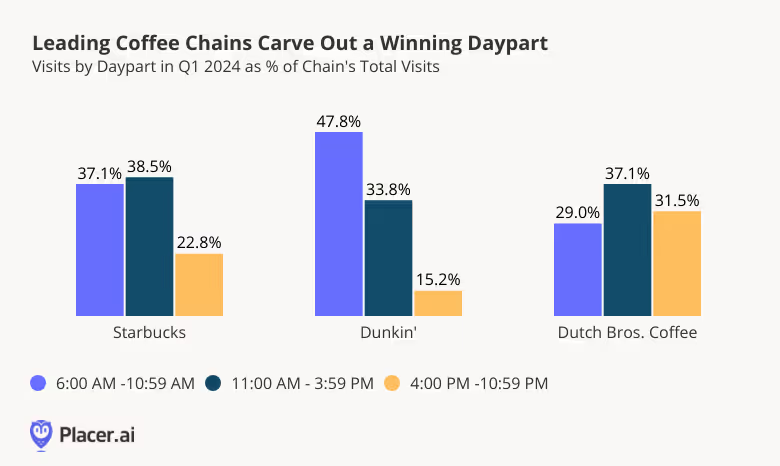

Each Coffee Brand Fills a Different Need

The visit growth for the three coffee leaders analyzed shows that there is enough consumer demand to support across-the-board growth in the space. And analyzing the Q1 2024 hourly visit distribution for Starbucks, Dunkin’, and Dutch Bros. reveals that visits to each chain follow a unique pattern – suggesting that every brand plays a unique role in the wider coffee landscape.

Dunkin’ received almost half (47.8%) of its visits before 11:00 AM, indicating that many guests visit Dunkin’ primarily for coffee or other breakfast fare. Starbucks’s guests tended to visit a little later in the day – with 38.5% of Starbucks visits taking place between 11:00 AM and 3:59 PM – so many consumers may be visiting the Seattle-based chain for a midday pick-me-up. Meanwhile, Dutch Bros. saw the largest share of late afternoon and evening visits (between 4:00 and 10:59 PM) relative to the other two chains – perhaps thanks to the chain’s wide variety of non-caffeinated beverages.

The variance in the hourly visit distribution between the three chains shows that the coffee space is big enough for multiple players and bodes well for the three chains’ performance in 2024.

For more data-driven pick-me-ups, visit Placer.ai.

This blog includes data from Placer.ai Data Version 2.0, which implements improvements to our extrapolation capabilities, adds short visit monitoring, and enhances visit detection.

.avif)