.svg)

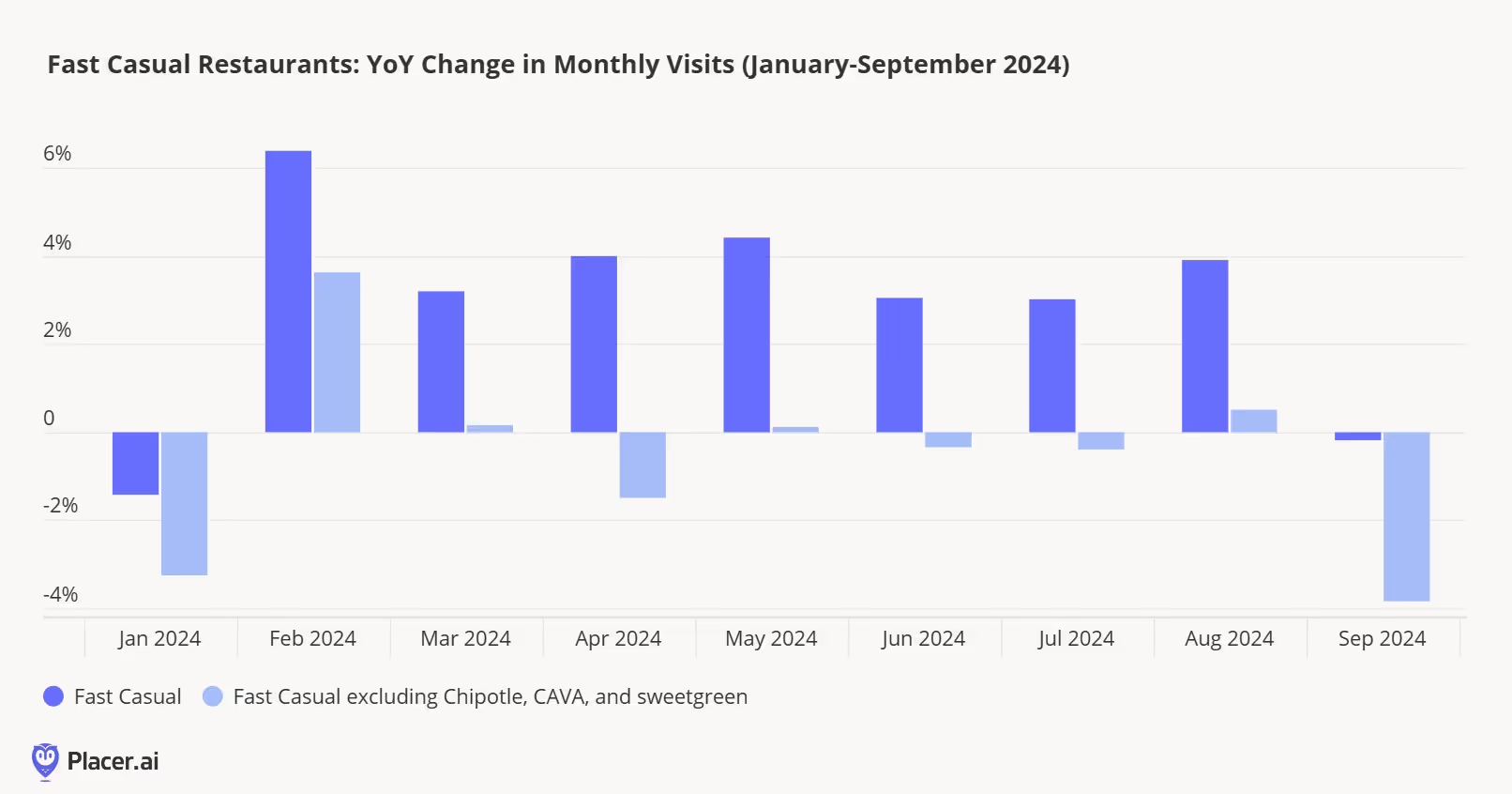

Most chains attending the 2024 Fast Casual Executive Summit in Denver acknowledged that this year has been difficult (unless you happen to be Chipotle, CAVA, or sweetgreen). We’ve highlighted a number of the challenges restaurant operators faced this past year, including inclement weather to start the year, the restaurant value wars of 2024, encroachment from other food retail channels, and the rising cost of operating a restaurant, which has resulted in increased bankruptcies. Our data validates this stance–our data shows that the fast casual category excluding the three aforementioned chains has seen year-over-year visitation declines.

Why are these three chains outperforming? As we’ve discussed in the past, we believe it comes down to (1) innovation; and (2) operational excellence. Recently, we looked at the importance of Chipotle’s Chicken al Pastor relaunch for Q2 2024 sales trends, sweetgreen’s increase in comparable visits that was helped by the launch of Caramelized Garlic Steak as a protein option, and CAVA’s exceptionally strong visitation trends due the launch of grilled steak at the beginning of June. However, innovation is only part of the outperformance, as each of these chains have also done a great job integrating their digital ordering platforms and in-store assembly line efforts, allowing for greater customization (something consumers appear to be willing to pay a premium for) and driving some of the strongest throughput numbers we’ve observed with our data.

The executives we spoke to at this week’s event had a gameplan to overcome these challenges in 2025.

- Navigating value wars. Most operators we spoke to at the event acknowledged that the Restaurant Value Wars of 2024 and more promotional pricing by grocery stores/superstores, and increased competition from c-stores has been a headwind this year. Despite consumers being very deal-driven consumers, most fast casual operators we spoke to planned to follow in Chipotle, CAVA, and sweetgreen’s innovation to drive improved visits rather than utilizing bundled value meals.

- Shift in consumer daypart preferences changes restaurant operations. Changes in consumers’ daily routines was a frequent topic at the event, including fewer visits during the early morning daypart, steady visit trends in the late morning, and early afternoon dayparts, but also an increase in dinner and late night dayparts (a topic we’ve looked at with Chipotle in the past as well). Some chains have reallocated labor or increasingly utilizing third-party delivery companies to accommodate these changes in demand.

- “Familiarity” and its role in market expansion. One executive we spoke with believed “familiarity” was a key motivating factor for consumers in a more challenging macroeconomic environment. Put another way, consumers have less discretionary dollars after years of elevated food, rent, healthcare, and insurance inflation, so when they choose to dine out, they are turning to brands they are familiar with and trust. As such, this preference for familiar brands may be negatively impacting brands when they enter a new market. Historically speaking, a restaurant brand that opens a location in a new market expects to see 75% of the sales/visits that a location in an established market does. It varies by concept and market, but our data suggests that new restaurant visit trends are much lower for those chains that are expanding to new markets for the first time. Not surprising, many operators told us their 2025 expansion plans would focus more on in-filling existing markets rather than expanding to new markets.

Another executive told us that the currently challenging backdrop would ultimately make chains better operators. Not every chain can be Chipotle, CAVA, or sweetgreen, but there are still a lot of their strategies that restaurants can adopt to improve their own operations.

.avif)