.svg)

Sprouts Farmers Market, the Phoenix, Arizona-based natural foods chain with some 419 locations across 23 states – up from 391 in July 2023 – is firmly in expansion mode. The chain reported a strong Q2 2024, including a 6.7% increase in comparable store sales.

But how did Sprouts perform in Q3? We dove into the data to find out.

Sprouting Ahead of the Pack

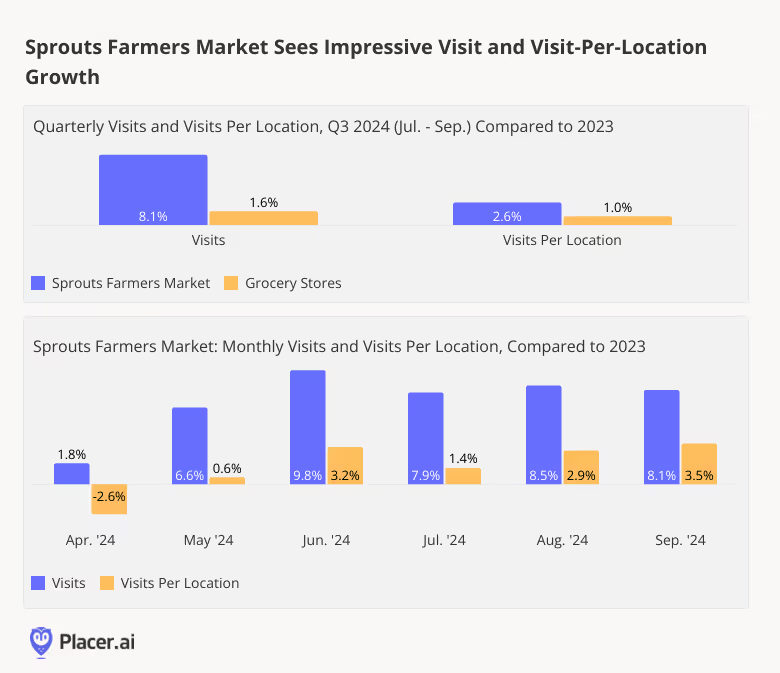

Given its rapidly-growing footprint, Sprouts’ strong year-over-year (YoY) foot traffic growth – 8.1% in Q3 2024, far above the industry average of 1.6% – may seem unremarkable. After all, a bigger fleet means more locations to contribute to the chain’s overall visit count. But for Sprouts, expansion is just part of the story. Throughout Q3 and most of Q2, the average number of visits to each of Sprouts Farmers Market’s locations also increased YoY, showing that the chain’s growing store count is meeting robust demand. And though the wider grocery space also saw a YoY uptick in visits per location, the increase was significantly lower (1.0% in Q3 for the segment as a whole, compared to 2.6% for Sprouts).

Turkey Wednesday, Here We Come!

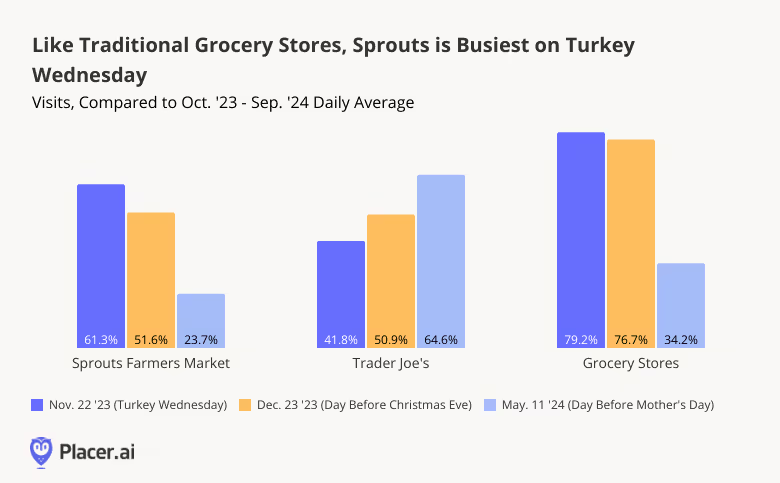

What can Sprouts expect this holiday season? In the past, location analytics have shown that while Turkey Wednesday – the day before Thanksgiving – is a major milestone for traditional grocery stores, specialty grocers like Trader Joe’s see smaller visit peaks on the big day.

But though Sprouts Farmers Market is certainly positioned as a specialty grocer, it is somewhat more akin to a traditional supermarket than key competitors like Trader Joe’s. For one thing, Sprouts boasts a wider array of merchandise than Trader Joe’s – including a huge selection of fresh, organic fruits and vegetables. And while Sprouts has been leaning heavily into its growing portfolio of private-label products, they still account for a minority of the chain’s revenue (In Q2 2024, just about 20% of Sprouts’ revenue came from private-label items – while at Trader Joe’s, some 80% of products sold are own-label.)

Perhaps as a result of these differences, consumers interact with Sprouts in some ways as they would with a traditional supermarket – including during the holidays. On November 22nd, 2023, for example (last year’s Turkey Wednesday), visits to Sprouts were up 61.3% compared to the chain’s daily average for the 12-month period ending September 30th, 2024 – making it Sprouts’ busiest day of the year by far. Though this jump was smaller than the 79.2% visit spike seen by the wider grocery store category, it was significantly larger than the 41.8% boost experienced by Trader Joe’s – which draws more traffic on the day before Mother’s Day. (December 23rd was the second-busiest day of the year for all three.)

More Families With Children, Fewer Singles

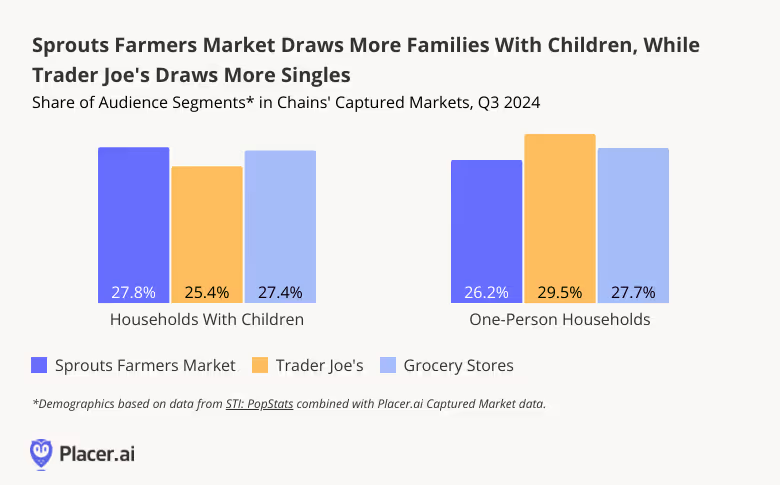

Additionally, like traditional grocery stores, Sprouts Farmers Market attracts more parental households, and fewer singles, than Trader Joe’s – another reason, perhaps, why it’s so busy on Turkey Wednesday.

Over the past twelve months, the share of families with children in Sprouts’ captured market stood at 27.8% – higher than Trader Joe’s 25.4% and in line with the industry-wide average of 27.4%. On the flip side, the share of one-person households in Sprouts’ captured market was 26.2%, lower than Trader Joe’s 29.5%, and once again more closely aligned with the somewhat-higher 27.7% observed for the grocery category as a whole. As a family-friendly chain that caters to parents on the hunt for healthy food items, Sprouts will likely be a key destination this year for households seeking to load up on ingredients for the holidays.

*Captured market analysis weights each census block group (CBG) feeding visits to the chain according to its share in the chain’s overall foot traffic – thus reflecting the profile of the chain’s actual visitor base.

Full Speed Ahead

Sprouts Farmers Market is a specialty grocer– but one that is often treated like a traditional supermarket. With stellar YoY visit and visit-per-location performance under its belt, Sprouts appears poised to be a stand-out beneficiary of both Turkey Wednesday and the day before Christmas Eve (December 23rd) this year. What else lies in store for Sprouts this year?

Follow Placer.ai’s data driven retail analyses to find out.

This blog includes data from Placer.ai Data Version 2.1, which introduces a new dynamic model that stabilizes daily fluctuations in the panel, improving accuracy and alignment with external ground truth sources.

.avif)