.svg)

In a market ruled by value and convenience, traditional full-service restaurants (FSRs) have faced an uphill slog. But even in 2024, some FSRs are flourishing. We dove into the data to explore factors driving success at three very different full-service chains: First Watch, Chili’s Grill & Bar, and Outback Steakhouse.

First Watch: Expansion, Unabated

First Watch first burst onto the scene in 1983 with a single restaurant in California – and now boasts some 544 locations across 29 states. With offerings ranging from Superfood Kale Salads to more traditional pancakes and bacon and eggs, First Watch has emerged as a prime destination for diners seeking to enjoy a leisurely breakfast with family and friends.

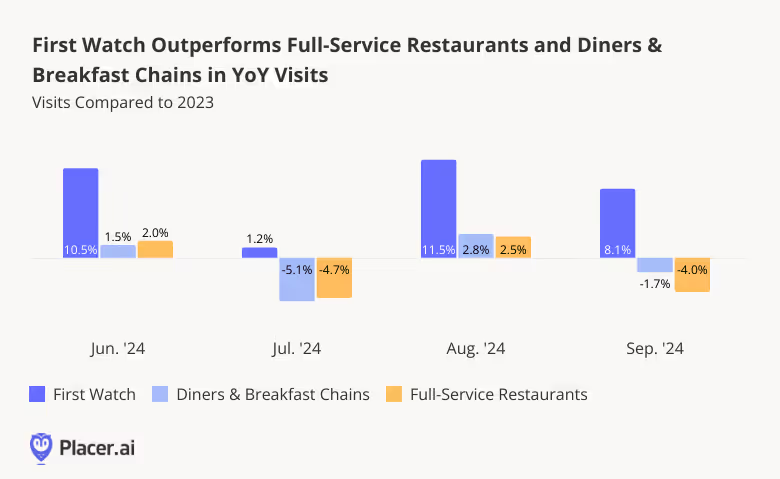

And foot traffic data shows that First Watch, still firmly in expansion mode, is continuing to grow its audience. Between June and September 2024, First Watch saw consistent year-over-year (YoY) visit growth, outperforming both the full-service restaurant category and other diners & breakfast spots.

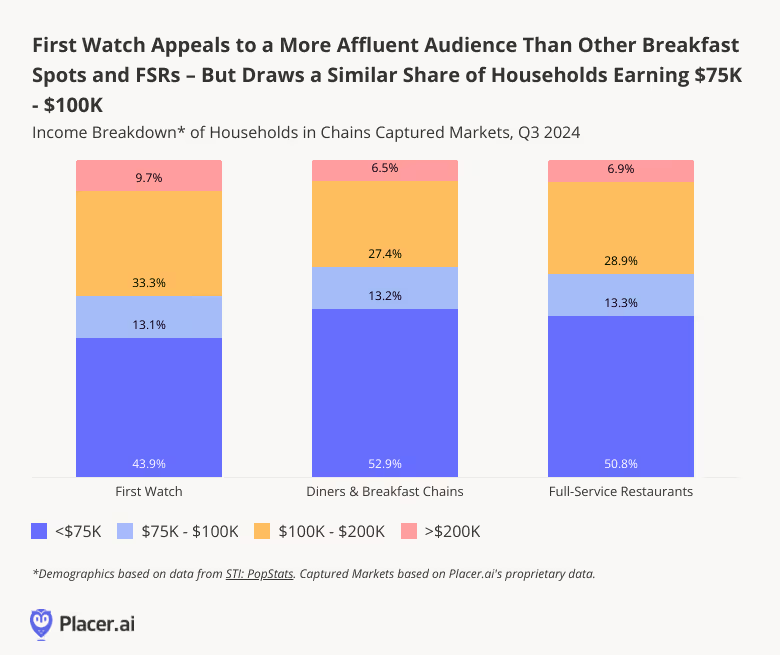

One factor that may be helping to propel First Watch’s success is the relative affluence of its customer base. Analyzing the income breakdown of First Watch’s trade area shows that in Q3 2024, nearly ten percent (9.7%) of households in the chain’s captured market earned $200K+ per year, compared with 6.5% for diners & breakfast chains and 6.9% for the wider FSR space. On the flip side, only 43.9% of households in First Watch’s captured market had annual incomes below $75K, compared to just over 50.0% for both analyzed segments.

Amidst concerns surrounding food inflation, rising labor costs, and discretionary spending cutbacks, First Watch’s wealthier customer base may be helping to shield it from some of the value pressures that have weighed on other restaurants – contributing to its resilience.

Chili’s Grill & Bar Rides the Big Smasher Wave

Another FSR that has been experiencing outsized visit growth this year – at least since April – is Chili’s Grill & Bar. Following a tepid start to the year, Chili’s launched its much-vaunted Big Smasher Burger on April 29th, 2024, and hasn’t looked back since.

The new offering, added to Chili’s 3 For Me value menu, presented a full-service value challenge to QSR favorites like the Big Mac. And in Q2 2023, the item helped drive a 14.8% increase in same-store sales.

Since the big launch, weekly YoY visits to Chili’s have been consistently elevated – kept aloft with the help of viral hype around Chili’s long standing Triple Dipper offering, as well as the new secret Nashville Hot Mozz offering that became so popular it spawned a halloween costume.

Unlike First Watch, Chili’s has found success by embracing its role as a value chain. The median household income (HHI) of Chili’s captured market in Q3 2024 was $73.1K – below the nationwide median of $76.1K, and on par with that of the wider FSR space ($73.7K – By way of comparison, the median HHI of First Watch’s captured market was $85.6K in Q3).

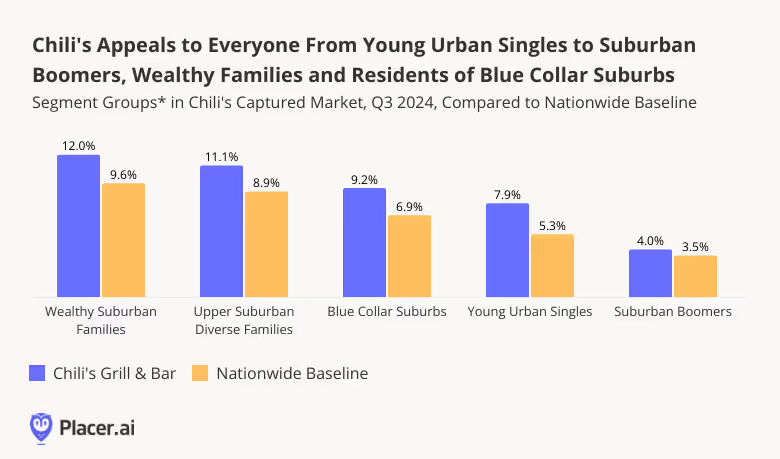

And a closer look at the demographic make-up of Chili’s captured market shows just how broad the appeal of the chain is. In Q3 2024, Chili’s visitor base was over-represented for a wide range of segments across age and income groups – from “Wealthy Suburban Families” to “Young Urban Singles”, “Suburban Boomers’, and residents of “Blue Collar Suburbs”. By delivering high-quality meals at affordable prices, Chili’s has solidified its place as an everyman’s chain, offering value comparable to that of quick-service restaurants.

Bloomin Brands’ Outback Steakhouse Rocks the Pacific West

Aussie-themed Outback Steakhouse – Bloomin’ Brands’ biggest chain – is another full-service restaurant that is successfully weathering the storm. Like other FSRs, Outback has faced its fair share of challenges over the past few years, with rising costs and spending cutbacks taking a toll on the chain’s performance. But in Q3 2024, the average number of visits to each Outback Steakhouse location increased 0.5% YoY, even as overall traffic to the chain fell 1.7% in the wake of strategic rightsizing moves that included the shuttering of a number of underperforming locations. By contrast, the average number of visits per location in the wider FSR space dropped 1.2%, while overall foot traffic to the segment fell 2.1%. Outback Steakhouse’s ability to sustain a YoY visit-per-location uptick in Q3, even if a minor one, shows that its rightsizing efforts are paying off.

And drilling down deeper into regional data for the chain shows that in some areas of the country, Outback Steakhouse is positively thriving. In California, Outback’s third-largest market in terms of store count, the chain saw a YoY visit increase of 5.3% – significantly higher than the statewide FSR average of 1.1%. In Washington and Oregon, Outback Steakhouse experienced even more substantial visit increases – 9.0% and 9.6%, respectively – even as full-service restaurants generally languished. And in all three states, the number of Outback Steakhouse locations has remained basically unchanged over the past year, meaning that these increases reflect the growing draw of the chain’s existing venues.

FSR Chains Ahead of the Pack

First Watch, Chili’s Grill & Bar, and Outback Steakhouse are very different full-service chains – but each of them is thriving in its own way. How will the three brands fare as the holiday season picks up steam?

Follow Placer.ai’s data-driven dining analyses to find out.

This blog includes data from Placer.ai Data Version 2.1, which introduces a new dynamic model that stabilizes daily fluctuations in the panel, improving accuracy and alignment with external ground truth sources.

.avif)

.avif)