.svg)

With sales exceeding $148 billion in 2023, The Kroger Co. is a leading player in the grocery store space. In addition to its flagship eponymous brand, the company owns a variety of regional banners, including (among others) Fred Meyer, Harris Teeter, Ralphs, Smith’s Food and Drug, Fry’s Food Stores, King Soopers, and Food 4 Less.

We dove into the data to see how key Kroger chains are faring in 2024 – and to explore the different audiences served by the company’s varied portfolio.

Setting the Stage: A Portfolio Breakdown

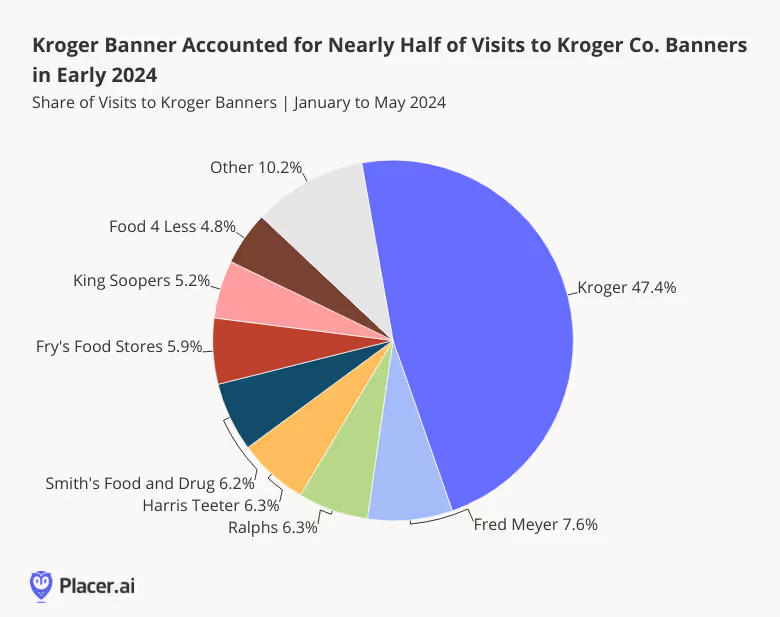

With some 1255 locations across 19 states, Kroger is The Kroger Co.’s largest grocery banner by far. And between January and May 2024, visits to the chain accounted for 47.6% of overall foot traffic to the company’s grocery portfolio. The remaining 52.4% of visits went to The Kroger Co.’s smaller banners – with Fred Meyer, Ralphs, and Harris Teeter leading the charge.

A Regional Deep Dive

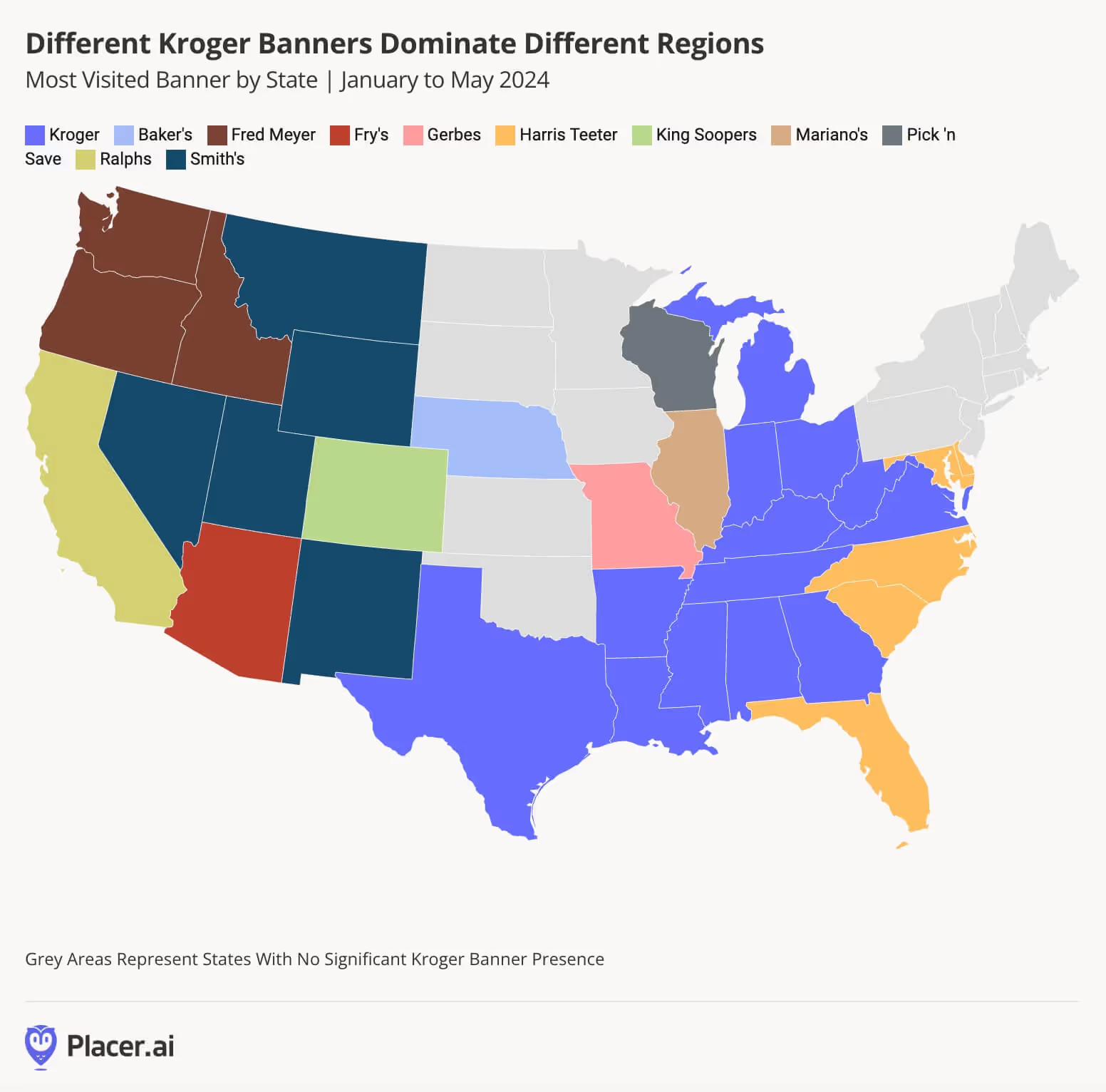

And drilling down deeper into the regional distribution of the company’s various grocery banners shows that each chain serves a different area of the country.

Kroger’s eponymous banner holds sway throughout much of the Midwest and South – while Harris Teeter serves shoppers in Maryland, Florida, and the Carolinas. Meanwhile, Fred Meyer, Smith’s, Ralphs, Fry’s, and King Soopers dominate the Western United States. And throughout some parts of the Midwest, Kroger draws consumers with a variety of smaller banners.

Like that of Albertsons, Kroger Co.’s strategy of acquiring and maintaining regional brands has allowed the company to expand its footprint across the country – while catering to the needs and preferences of local shoppers. Indeed, Kroger’s footprint now extends across three of the four U.S. regions – the West, South, and Midwest – with only the Northeast lacking a Kroger Co. presence.

Visits on the Rise

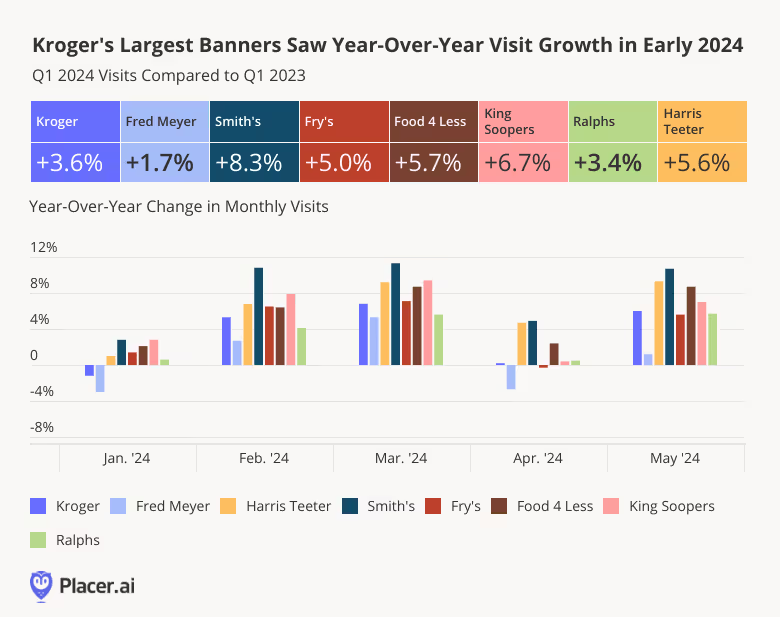

A look at recent visitation trends for Kroger Co.’s largest banners – i.e. those with at least 100 locations – shows that all experienced positive YoY visit growth in Q1 2024. The most impressive foot traffic bumps were seen by Mountain region banners Smith’s and King Soopers, followed by value-oriented Food 4 Less, and the South Atlantic-focused Harris Teeter.

On a monthly basis, too, The Kroger Co.’s major Banners saw nearly uniform YoY visit growth between January and May 2024.

Reaching Different Audiences

Analyzing demographic differences among the trade areas of Kroger’s different chains shows how the company leverages its portfolio of banners to serve distinct customer bases.

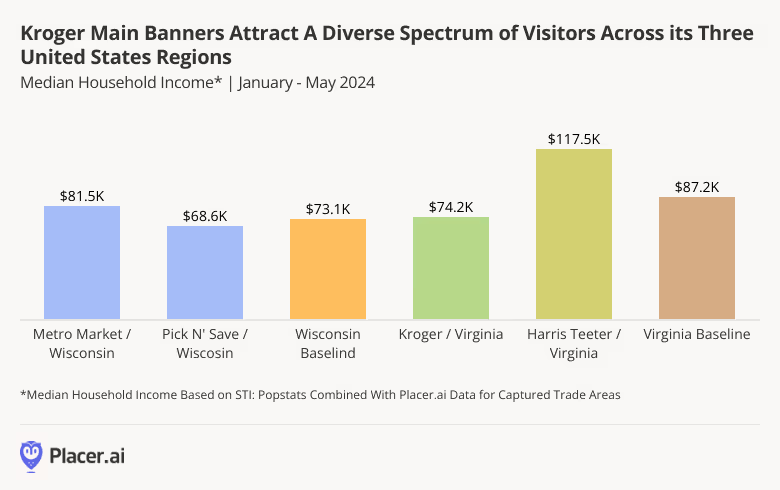

Virginia, for example, is served by two Kroger Co. banners – Kroger and Harris Teeter. And while the former draws shoppers from areas with a median HHI below the statewide baseline of $87.2K, the latter – with somewhat more upscale, pricier offerings – attracts a much more affluent audience. Similar differences can be observed in Wisconsin – where Pick ‘n Save and Metro Market serve different demographics.

By offering a diverse spectrum of shopping experiences, The Kroger Co. strategically positions itself to maximize market penetration and appeal to a broad range of consumers.

Looking Ahead

The Kroger Co. entered 2024 with a bang. With its extensive reach and adaptive approach, can the grocery leader maintain its positive momentum throughout the rest of the year?

Visit our blog at Placer.ai to find out.

As cars get more expensive, demand for repairs rises – and auto part chains are reaping the benefits. We analyzed the visit data for four leading auto part chains – AutoZone, O'Reilly Auto Parts, NAPA Auto Parts and Advance Auto Parts – and dove into O’Reilly Auto Parts’ recent growth to understand what may be driving success in this flourishing segment.

Could 2024 Be the Year of Auto Parts?

Auto parts chains are having a moment. With vehicle prices significantly higher than before COVID, many consumers would rather fix their cars than purchase new ones. At the same time, inflation has begun to subside, leaving people with more room in their budgets for non-essential maintenance and repairs.

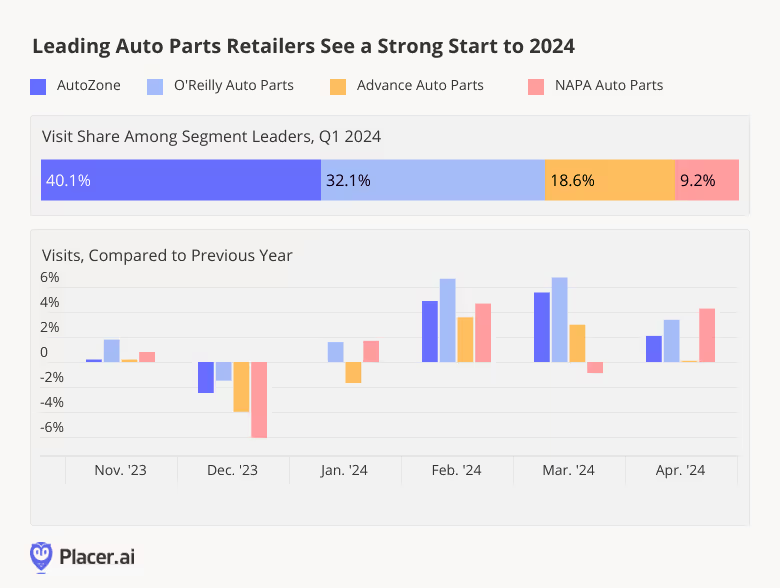

Following a drop in December 2023, YoY visits to AutoZone, O’Reilly Auto Parts, Advance Auto Parts, and NAPA Auto Parts began to pick up in January 2024 – despite unusually cold and stormy weather that left many consumers hunkered down at home. And between February and April, YoY visits to the four chains remained nearly uniformly elevated.

On a quarterly basis, O’Reilly Auto Parts saw the biggest YoY visit increase, despite lapping a strong 2023. The chain, which drew 32.1% of total visits to the four brands in Q1, saw quarterly YoY foot traffic increase by 5.1%. AutoZone, which received 40.1% of quarterly visits to the four chains, saw quarterly YoY visits increase by 3.5%. And Advance Auto Parts and NAPA Auto Parts both saw quarterly YoY visits increase by 1.7%.

O’Reilly’s Successful Loyalty Program

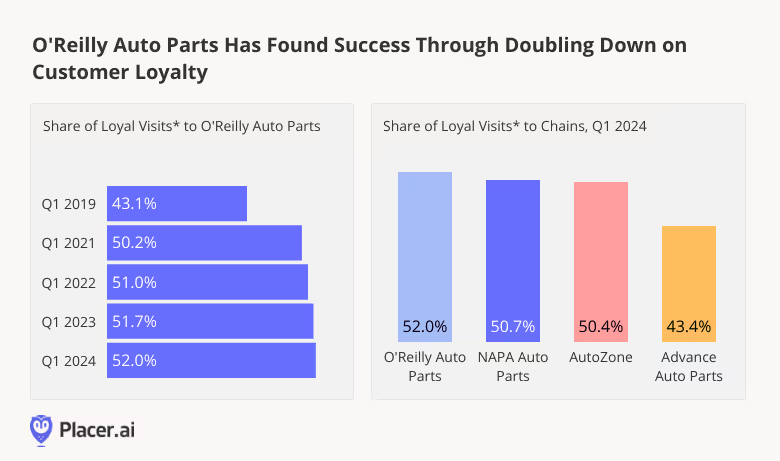

One strategy that has likely helped O’Reilly Auto Parts stay ahead of the pack is its much-touted loyalty program, recently ranked by Newsweek as one of the best in the nation.

Location intelligence shows that since COVID, O’Reilly Auto Parts has seen a steady increase in the loyalty of its customer base. And in April 2024, O’Reilly Auto Parts boasted the most loyal customer base of the four analyzed chains – with 52.0% of visits made by individuals that frequented the chain at least twice during the month. But other auto chains, including AutoZone, also enjoyed significant shares of visits by repeat customers – showing that there’s plenty of room at the top in the auto parts space.

Auto Parts Promising Year

The auto parts industry is poised for success in 2024, with leading chains like O'Reilly Auto Parts, AutoZone, Advance Auto Parts, and NAPA Auto Parts demonstrating resilience and growth. How will these chains continue to perform as the year wears on?

Visit placer.ai to find out.

Sweetgreen and First Watch both went public in 2021 and have since steadily increased in popularity – and in store count. So with 2024 well underway, we checked in with the two brands to see how they fared in Q1 and to explore some of the factors underlying their success.

Sweetgreen’s Successful Expansion

Despite the dining challenges of much of 2023 and early 2024, sweetgreen posted impressive visits between April 2023 and March 2024, with the chain’s YoY traffic increases ranging from 21.4% to 51.6%.

The remarkable visit surge was partially driven by the sweetgreen’s significant expansion, which could explain the slight dips in average visits per location for much of 2023 while consumers around sweetgreen’s newer restaurantes familiarized themselves with the brand’s offerings. But since December 2023, YoY visits per location have been positive – with the exception of a weather-induced slump in January – indicating that the chain’s newer venues have established themselves within their community.

This narrowing of the gap between visits and visits per location may also signal the success of sweetgreen’s strategic shift towards prioritizing "quality over quantity” – slowing down expansion and investing in an enhanced customer experience.

Healthy Salads for Everyone

As a salad and grain-bowl chain, sweetgreen holds special appeal for wellness-focused younger consumers, including singles and members of the coveted Gen Z demographic. But as the chain has expanded, it has also succeeded in reaching new audiences.

Sweetgreen has been explicit about its goal of reaching Gen Z consumers. And analyzing the demographic makeup of the chain’s captured market reveals that sweetgreen’s trade area includes a relatively large share of one-person households (that tend to be on the younger side) But analyzing shifts in the chain’s captured market composition over the past five years also reveals that the share of one-person households has been decreasing – while remaining above the nationwide average of 28.0% – and the share of households with children has increased. So even as sweetgreen continues serving its core consumers, the chain’s expansion has also allowed sweetgreen to reach new audiences.

First Watch’s Never-Ending Expansion

First Watch is also in expansion mode, and with plans to open some 50 more restaurants this year the chain shows no signs of slowing down. And, like sweetgreen, First Watch’s expansion has driven significant growth to the chain’s overall visits – and the chain’s average visits per location numbers are up as well, indicating that the new venues are finding a receptive audience.

By staying nimble on its feet and continually changing up its menu offerings, First Watch has succeeded in differentiating itself from other breakfast chain giants – and appears poised to enjoy continued success throughout the year.

Expanding Its Reach

First Watch’s expansion has also helped the company reach new types of diners even as the chain continues catering to its core audience. The share of the Spatial.ai: PersonaLive’s “Upper Suburban Diverse Families” segment in First Watch’s captured market has held steady over the past five years, even as the share of the “Blue Collar Suburbs” and “Urban Low Income” segments increased. It seems, then, that First Watch has also succeeded in leveraging its store fleet expansion to reach new audience segments – without sacrificing its core patrons.

.avif)

Sweetgreen and First Watch Head into 2024 on an Upswing

Sweetgreen and First Watch’s expansions have helped the companies increase visits and reach new segments – without sacrificing their core audiences. What does the rest of 2024 have in store for the chains?

Visit our blog at placer.ai to find out.