.svg)

Dining took a hit over the past few years, with major challenges from COVID to rising costs weighing on the category. And perhaps no food-away-from-home segment was more impacted than Full Service Restaurants (FSR) – which stagnated as consumers traded down and sought out more affordable ways to treat themselves.

But new years present new opportunities – and there are signs that sit-down restaurants may be springing back to life. So with 2024 underway, we dove into the data to explore the current state of FSR. Is cooling inflation prompting a rise in Full Service Restaurant activity? How did FSR leaders like Dine Brands (owner of casual dining favorites Applebee’s and IHOP), Bloomin’ Brands (owner of popular grill and steak chains like Outback Steakhouse and Carrabba’s Italian Grill along with high-end Fleming’s Prime Steakhouse & Wine Bar), and Texas Roadhouse fare in Q1?

Restaurants To Dine For: Applebee’s and IHOP

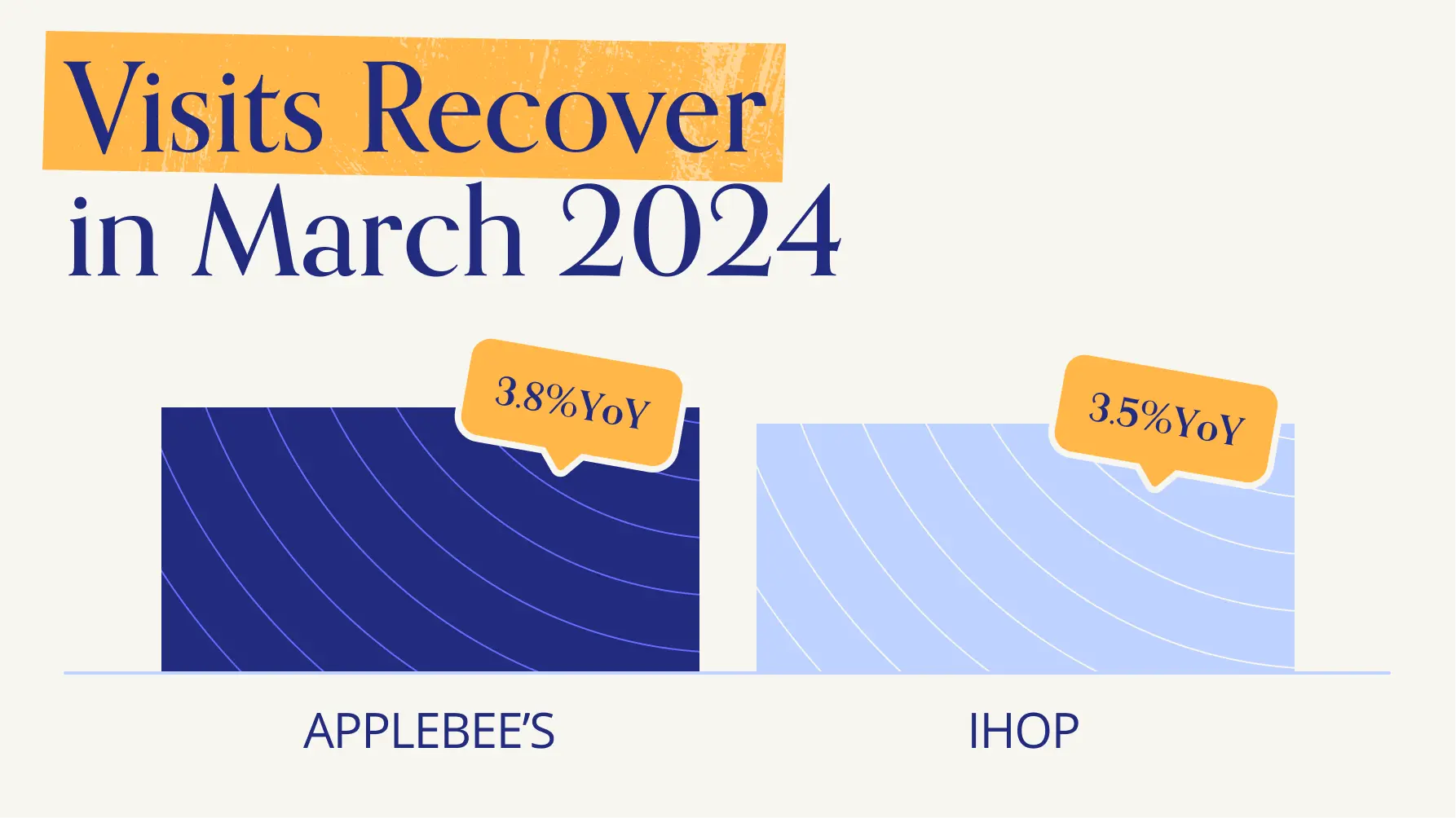

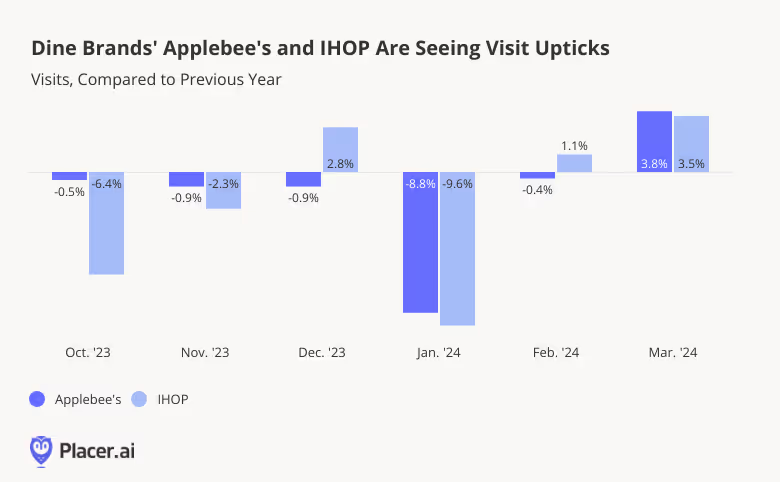

With some 1500 locations nationwide, Applebee’s has long been a mainstay of the American casual dining scene. Like other FSR chains, Applebee’s experienced a setback during the pandemic and has since faced industry-wide headwinds. But even though the brand’s store fleet shrunk by around 30 stores last year, overall YoY visits to Applebee’s declined just slightly between October 2023 and February 2024 (January’s weather-driven slump aside). And in March, the chain saw a promising 3.8% YoY visit uptick.

Breakfast leader IHOP also experienced negative YoY visits in October and November 2023, but in December – when the pancake chain traditionally enjoys a major holiday boost – visits jumped 2.8% YoY. Like Applebee’s, IHOP felt the effects of January’s Arctic blast, but saw its visits recover quickly in February and March 2024.

Bloomin’s Grill and Steak Chains on a Comeback

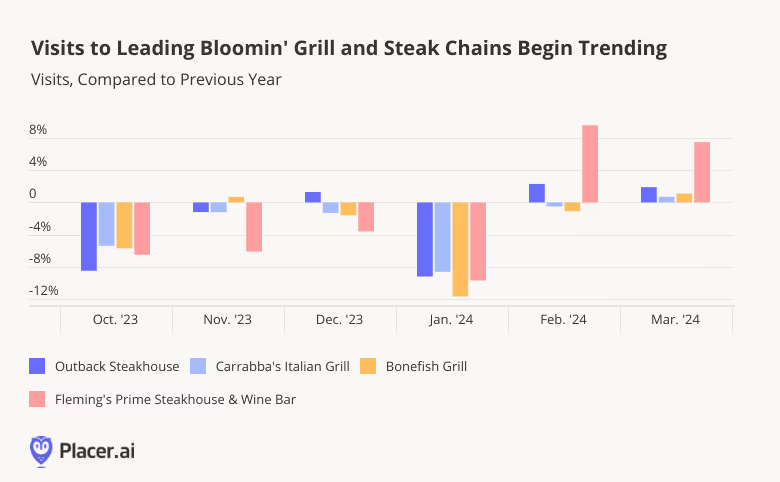

Bloomin’ Brands’ leading casual dining chains Outback Steakhouse, Carrabba’s Italian Grill, and Bonefish Grill appear to be following largely similar trajectories.

Though the brands experienced YoY visit gaps through most of Q3 2023 – and were whalloped by January’s inclement weather – all three chains experienced YoY visit increases in March 2024. Given the fact that the restaurants’ store counts didn’t change significantly last year, this visit growth appears to portend good things for Bloomin’s fast casual portfolio in the year ahead.

But it is Bloomin’ Brands’ fine dining concept, Fleming’s Prime Steakhouse & Wine Bar, that really seems to be hitting it out of the park. While Fleming’s also saw visit gaps between October 2023 and January 2024, the chain experienced 9.6% and 7.5% visit growth, respectively, in February and March 2024 – closing out Q1 with a bang.

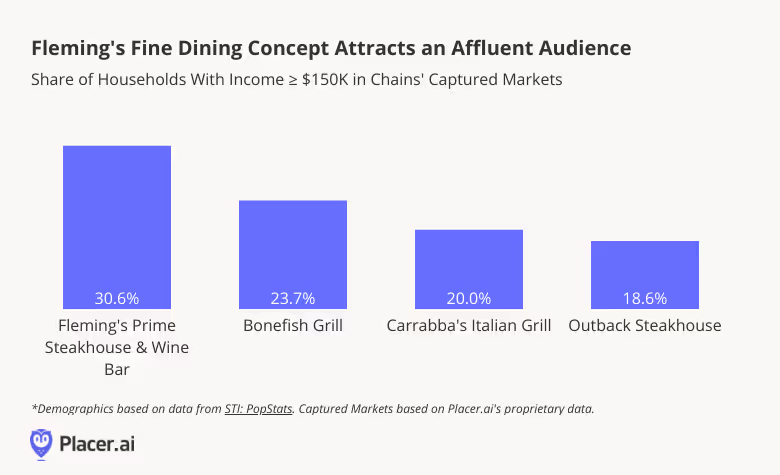

Fleming’s particularly robust recent performance may be due in part to its relatively affluent customer base. Nearly one-third of households in Fleming’s captured market have an annual income of $150K or more – compared to just 18.6% to 23.7% for Bloomin’s casual dining concepts. Though a night out at the fine-dining steakhouse can be expensive, Fleming’s well-heeled visitor base is better positioned to absorb price increases than other consumers.

Texas Roadhouse’s Sizzling Success

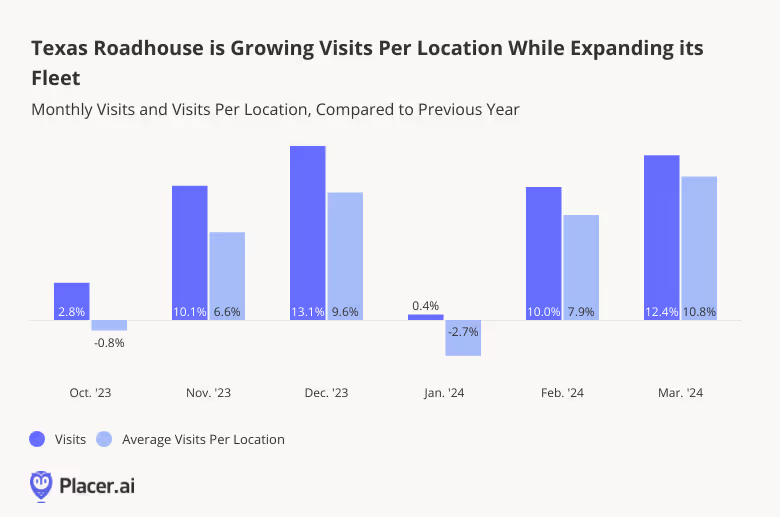

Appealing to affluent consumers, however, isn’t the only way to go. Texas Roadhouse is firmly in the casual dining space and tends to cater to average-income diners. (In Q1 2024, just 15.2% of its captured market had a household income ≥$150K.) But the steakhouse’s strategy of satisfying steak lovers with high-quality, affordable offerings is working: Throughout Q1, Texas Roadhouse experienced strongly positive YoY visit growth. And while some of this growth is attributable to the brand’s increasing unit count, the average number of visits per location is generally keeping pace – showing that Texas Roadhouse’s expansion continues to meet strong demand.

Poised for Further Growth

Though more affordable Dining segments like QSR and Fast Casual began to spring back to life last year, FSR has yet to fully recover from the double whammy of COVID and inflation. But if March 2024’s promising numbers are any indication, the category may be in for a turnaround. How will FSR continue to perform as 2024 progresses?

Follow Placer.ai’s Dining deep dives to find out.

.avif)

.avif)