.svg)

For grocery stores, last year held plenty of challenges – from high food-at-home prices to increased competition from non-traditional grocery players like dollar stores and superstores. But 2023 also offered the segment plenty of opportunities. Discount chains made a strong showing – and customers spent more time browsing grocery aisles, loading up on essentials and making every trip to the store count.

But which grocery brands were most popular in 2023? Did large national chains dominate the scene, or did regional and local banners also have a role to play? And what can foot traffic analytics tell us about some of the broader trends that shaped brick-and-mortar grocery shopping last year?

We dove into the data to find out.

And the Winner is… Kroger!

The nation’s most-visited grocery banner in 2023 was Kroger, which captured almost 19% of annual foot traffic to the nation’s ten most-frequented grocery chains. Safeway, owned by Albertsons, also made the top ten list.

But significantly, several regional chains also garnered significant nationwide visit share – including Texas cult-favorite H-E-B, midwestern Meijer, and East Coast Food Lion and ShopRite. Aldi, the no-frills budget chain that keeps prices low by offering a limited inventory of mainly private-label products, emerged as the fourth most-visited grocery store in the country. And fan-favorite Trader Joe’s, also known for its high-quality own-label merchandise, drew 6.5% of visits to the top ten brands.

.avif)

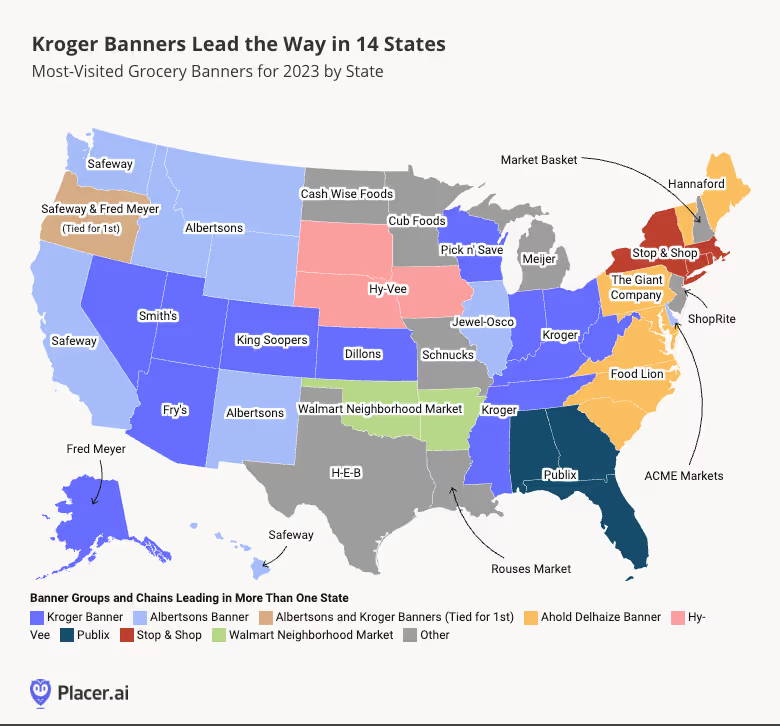

Plenty of Room for Regional and Local Players

And drilling down deeper into the data for each of the fifty states shows that each region of the country had its own local favorite. Kroger banners – including Kroger, Smith’s, King Soopers, Dillons, Fry’s Food Stores, Fred Meyer, and Pick n’ Save – topped the charts in 14 states. In one of these (Oregon), Kroger’s Fred Meyer was tied for first place with Safeway, an Albertsons banner. In addition to Oregon, Albertsons banners took the lead in nine more states, mainly in the Western region of the U.S., while Ahold Delhaize banners ranked first in seven Northeast and South Atlantic states. And a variety of more local chains held sway throughout much of the Midwest and parts of the South.

A Changing Customer Profile

Who were the shoppers driving visits to brick-and-mortar grocery stores in 2023? Location intelligence shows that overall, visitors to grocery chains last year tended to come from areas with slightly higher median household incomes (HHIs) than the nationwide average. Less affluent consumers, perhaps, were more likely to seek out lower-cost grocery alternatives like dollar stores. At the same time, there remained significant HHI gaps between chains, likely reflective in part of regional differences.

.avif)

And comparing the overall median HHI of grocery chains’ captured markets to that of previous years reveals a small but distinct decline in the relative affluence of likely grocery visitors, from $76.2K in 2019 to $73.8K in 2023. Over the same period, the share of “Flourishing Families” in the chains’ captured markets (A psychographic segment encompassing affluent middle-aged families and couples) decreased slightly, while the share of “Singles and Starters” increased.

These shifts may be partially due to the more widespread adoption of online grocery shopping among certain audience segments in the wake of COVID. While ecommerce only accounted for an estimated 7.2% of grocery spending as of May 2023 – with high delivery fees continuing to deter many Americans from going the online route – higher-HHI consumers may be particularly willing to prioritize convenience over price.

.avif)

Key Takeaways

For grocery stores, 2023 was all about value – with many customers flocking to discount chains and going out of their way to maximize savings. Still, traditional mainstays like Kroger and Albertsons continued to capture the biggest pieces of the grocery pie.

What does 2024 have in store for the grocery space? Will shoppers place less emphasis on savings as inflation continues to ease? And which chains will emerge as nationwide and regional winners?

Follow Placer.ai’s data-driven retail analyses to find out.

.avif)

.avif)