.svg)

Sprouts, the natural and organic food focused grocery chain operating in 23 states nationwide, is going through a growth spurt. We dove into the visit and audience data to see where the chain stands today and what the rest of 2024 – and beyond – may have in store.

Sprouts is on a Growth Spurt

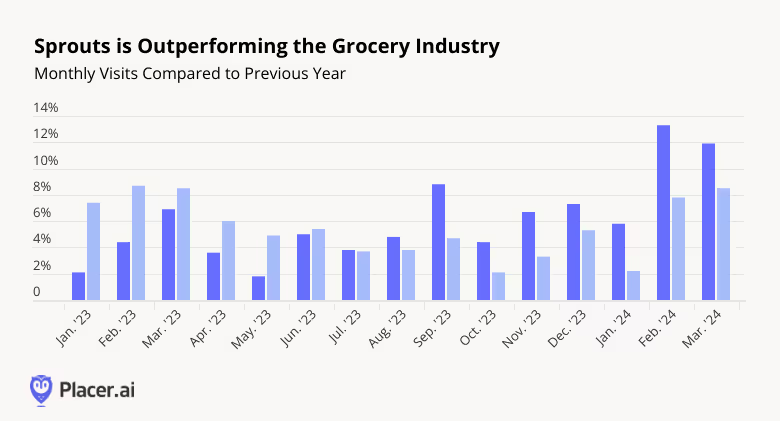

Sprouts is on the rise. Year-over-year (YoY) visits increased every month of last year and have been outperforming the nationwide Grocery average since mid-2023. And the chain continued to grow in Q1 2024, with visits up an impressive 13.3% and 11.9% in February and March 2024, respectively – an impressive feat given the comparison to an already strong Q1 2023.

Some of the growth is driven by expansion – the company opened 30 new stores in 2023 and expects to add 35 additional locations in 2024. But the increase in foot traffic is also a testament to the potential of specialty grocery stores to leverage their unique product selection to attract grocery shoppers, even in the face of growing competition in the space.

Sprouts High-Income Visitor Base Likely Contributing to the Chain’s Success

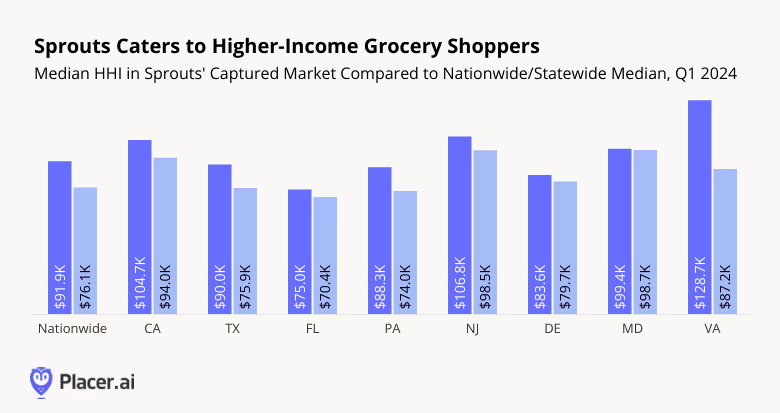

The relatively high income of Sprout’s visitor base is likely also helping the chain stay ahead of the grocery pack: Median HHI in Sprout’s trade areas nationwide is higher than the U.S. median HHI, and the data shows a similar trend in Sprout’s eight growth markets.

The relative affluence of Sprouts shoppers means that this segment may not be as impacted by high food prices as other grocery shoppers – so the retail headwinds predicted this year are not likely to slow down Sprout’s growth potential as the chain continues expanding its reach in 2024.

Sprouts’ Different Growth Markets Exhibit Different Characteristics

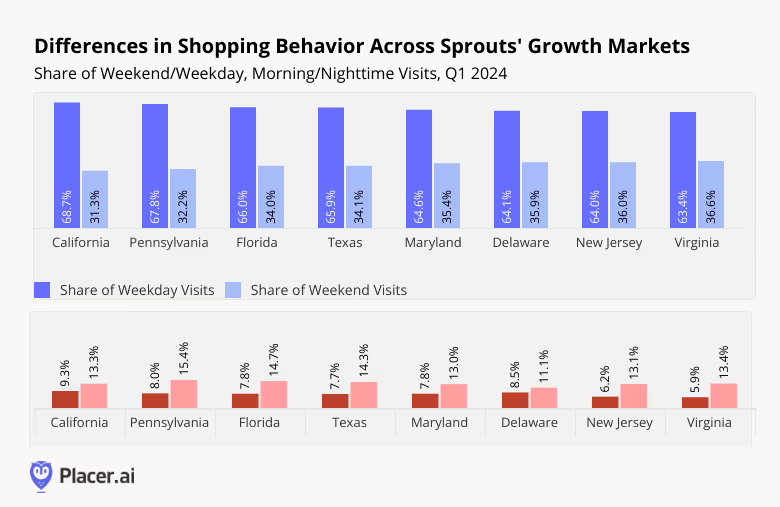

While Sprouts’ visitors across states seem to share a relatively high income level, diving deeper into the location intelligence data reveals some major differences in both in-store behavior and overall market composition.

For example, the share of weekend (as opposed to weekday) visits to Sprouts in Q1 2024 varied significantly – from 31.3% in California to 36.6% in Virginia. Shoppers in the company’s various growth markets also visited stores at different hours throughout the day: Mornings (8:00 AM to 9:59 PM) were popular with California, Delaware, and Pennsylvania residents, while evenings were favored by Pennsylvanians, Floridians, and Texans.

Understanding the in-store behavior of shoppers in each state will likely help Sprouts adapt its operations and staffing schedules as the company continues expanding in these markets.

Differences in the Composition of the Grocery Market in Each State

In addition to highlighting the variance between the shopping habits of Sprouts visitors across markets, diving deeper into the location intelligence data also reveals differences in the relationship between Sprouts shoppers and the wider grocery markets in each state.

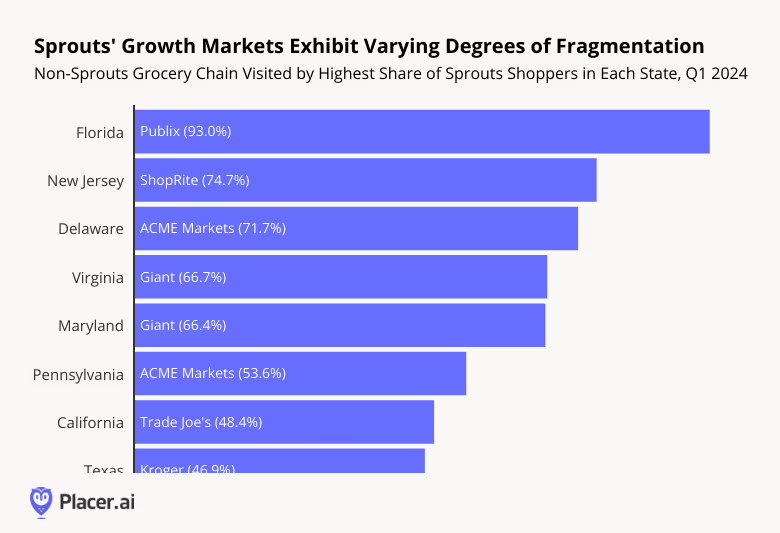

The chart below shows the most popular grocery alternative for Sprouts shoppers in each state (which other grocery chain was the most visited by Sprouts visitors) and what share of Sprouts shoppers visited that grocery chain in Q1 2024.

In Florida, over 90% of Sprouts shoppers also visited a Publix location in Q1 2024 – indicating that Sprouts in the Sunshine State is operating in a relatively consolidated grocery market and operating against an established crowd favorite. Meanwhile, only 46.9% of Texan Sprouts visitors also visited a Kroger – the other grocery chain most visited by Sprouts visitors – indicating that the Texas grocery market may be more fragmented, and so may respond to a different expansion strategy, than the Florida grocery market.

Sprouts’ Room to Grow

Sprouts strong visitation trends indicate that the grocery chain is expanding into willing markets, and the brand’s relatively affluent shopper base means that Sprouts is unlikely to be too impacted by whatever economic headwinds may lie ahead. As the chain continues making its presence felt in newer markets, location intelligence suggests that Sprouts has plenty of room to grow in 2024 and beyond.

For more data-driven retail insights, visit our blog at placer.ai.

.avif)