.svg)

As we enter November, the holiday season is already in full swing across the country. We’re likely to see the consumer’s embrace of seasonal decorations soon, just as we saw in the fall season. The retail industry has already lived through one major promotional event in October, and it’s time to take the temperature on physical retail foot traffic as we head into the busiest part of the season.

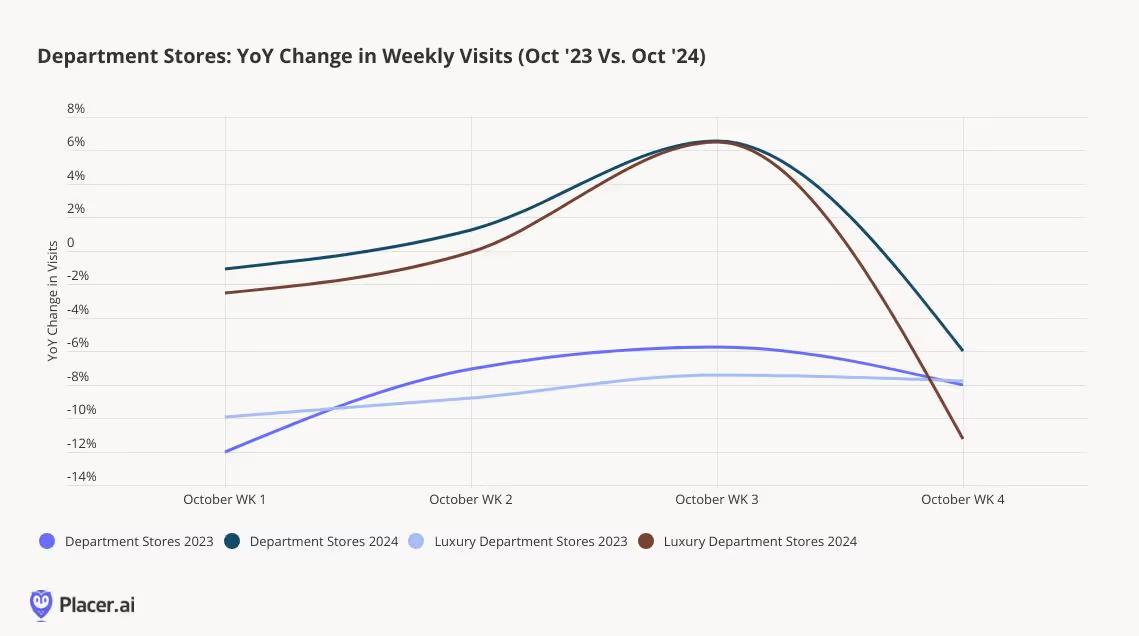

One thing that jumped out upon initial review was the foot traffic from department stores, excluding off-price retail. Looking at the four full weeks of October 2024, traffic to full line department stores was flat to last year, compared to the same period last year when traffic was down 8% to 2022 in October (store counts are about even to last year). Visits to luxury department stores show a similar story; traffic in 2023 was down 9% in October and trended down 2% this year. Coming from a sector of retail that has been challenged for years, this slight improvement is worthy of celebration.

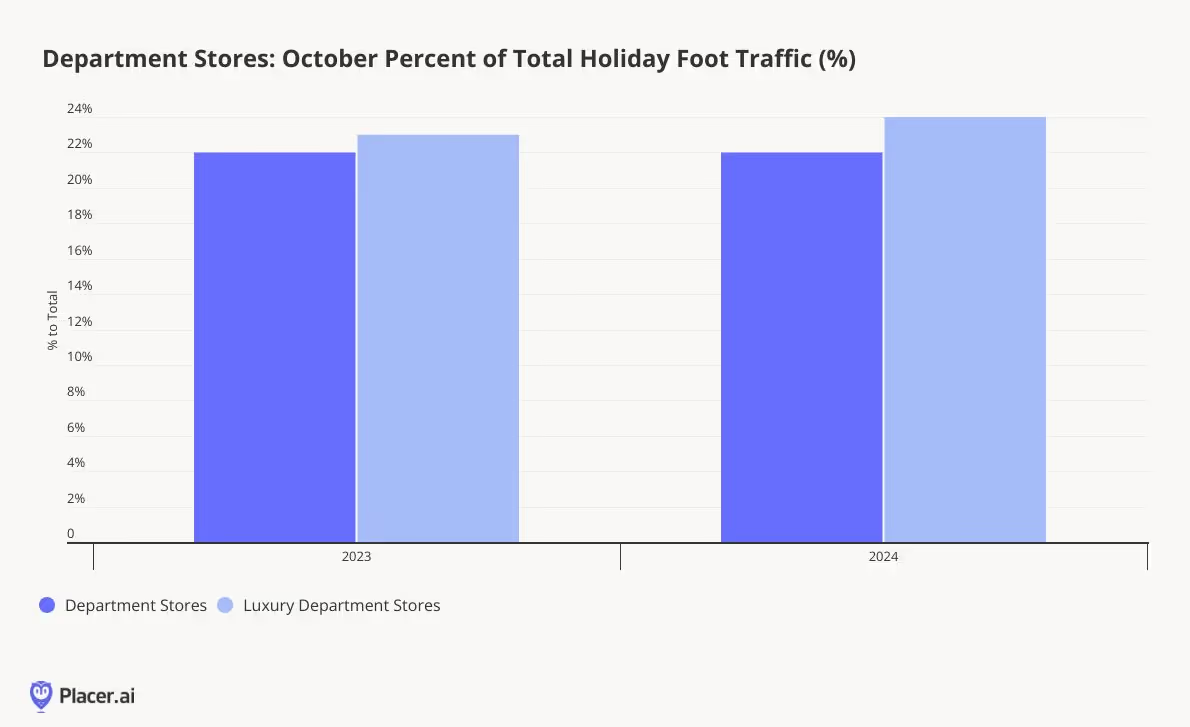

Just how important is October’s contribution to holiday shopping visits? For full line department stores, October accounted for 22% of total holiday season visits in both 2022 and 2023; October traffic for luxury department stores was 24% of total holiday traffic in 2022 and 23% in 2023. That means that there’s still almost ¾ of total visitation still left for retailers to capture over the next two months. However, with traffic trending better in 2024 than in 2023 for department stores overall, this year might actually be a proof point for pull forward holiday demand.

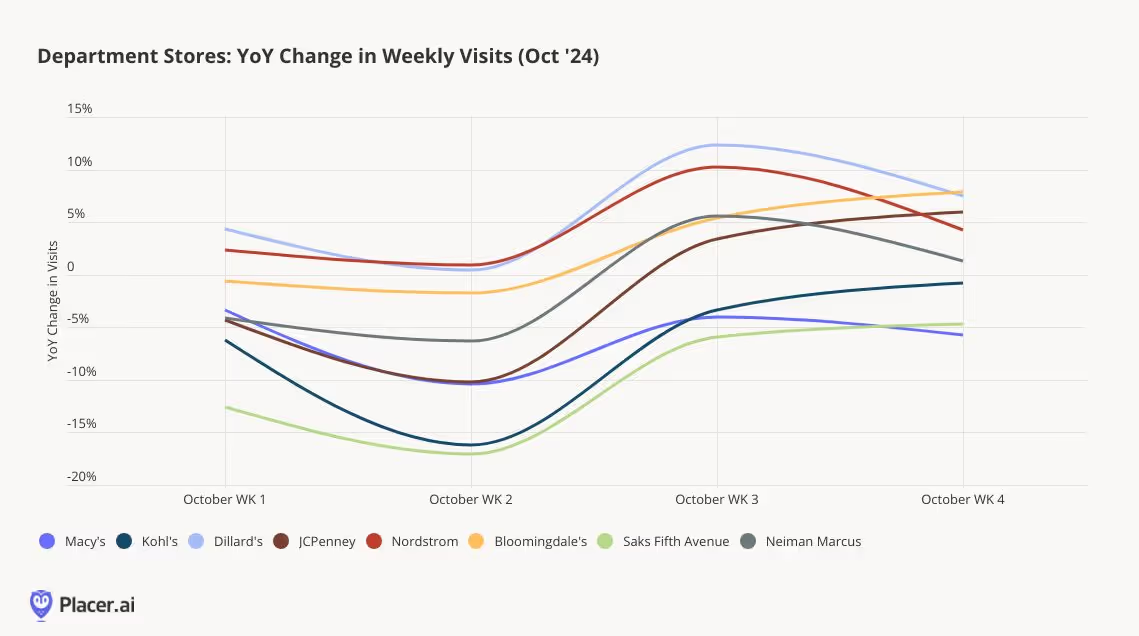

Looking at visitation by retailers within the two sectors, Dillard’s, unsurprisingly led the charge for full line department stores in visitation growth. JCPenney also saw a lot of trend improvement compared to last year, as did Macy’s in the back half of the month. The only major retailer that has underperformed 2023 in October was Kohl’s. Through the lens of luxury department stores, Bloomingdale’s and Nordstrom grew traffic in the low to mid-single digits in October, with Neiman Marcus only down slightly to 2023 levels.

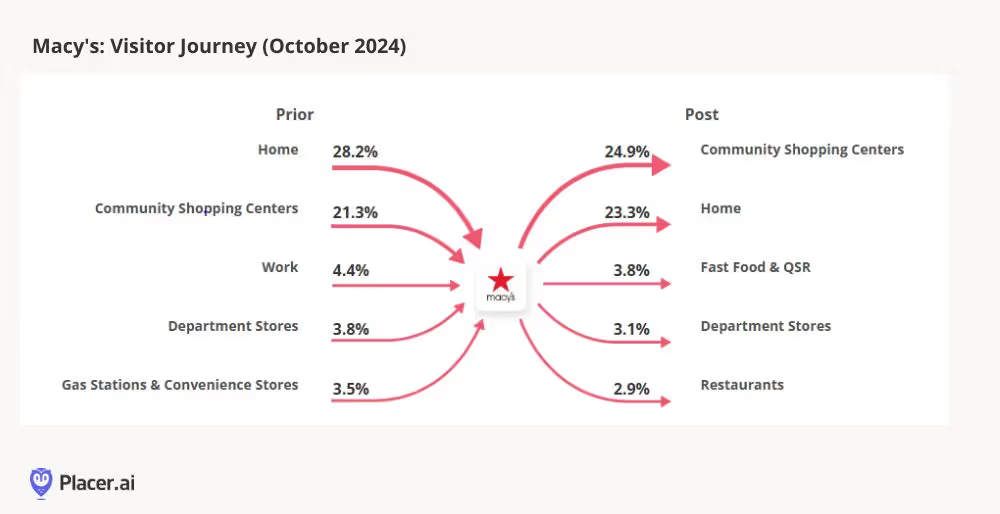

Another interesting insight Placer’s data uncovered; department stores are more of a destination for consumers this year. Looking at Macy’s cross-visitation specifically in October, the percent of visitors to Macy’s that traveled home after visiting was almost 50 basis points higher than in 2023. Our data also showed a lower percentage of cross visitation between Macy’s and other department stores this year compared to last October. Department stores may be doing a better job of capturing consumers' attention and better aligning themselves with the needs of their shoppers. This is in contrast of what we're seeing in essential retail categories such as grocery stores and superstores, where consumers are willing to cross shop multiple retailers; this underscores just how different consumer behavior is by category.

What does this signal about the remainder of the “true” holiday season? It’s hard to tell as we stand today, but the trend improvement across department stores this year gives us some optimism about consumers flocking to physical stores this year. But, it’s important to give consumers a reason to visit as many times as possible, especially as retail fatigue sets in from shopping earlier in the season. Value is still going to be the top driver of visitation this year, but unique products, services and experiences are still important to capturing the joy of the season.

%20(1).avif)