.svg)

Department stores across the country have been evolving to meet changing consumer wants and needs, and Macy’s & Bloomingdale’s are no exception. Owned by the same company – Macy’s, Inc – these two brands have been recalibrating their store fleets and experimenting with new formats.

We took a closer look at visitation trends to both brands to understand how they diverge, analyze their respective strengths, and explore what might be ahead for both.

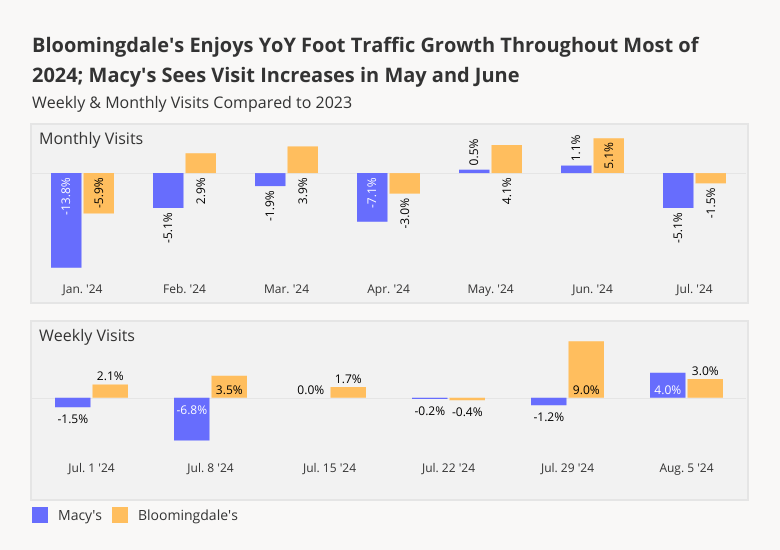

Monthly and Weekly Foot Traffic: Stabilization and Growth

In recent years, Macy’s, Inc. has focused on optimizing its store fleet, a long-running project that gained momentum with the 2023 appointment of former Bloomingdale’s executive Tony Spring as CEO. This change coincided with a turnaround strategy involving the closing of some 30% of the brand’s traditional department stores; the expansion of Macy’s small-format model; and the addition of more Bloomingdale’s locations.

And a look at foot traffic trends at Bloomingdale’s shows that the high-end brand is indeed experiencing an uptick in demand, making it ripe for expansion. For much of the period between January and July 2024, Bloomingdale’s saw YoY monthly visit increases, with only January, April, and July seeing YoY declines. January’s drop was likely due to the inclement weather that weighed on retailers nationwide, while the April 2024 YoY downturn may have been due in part to the comparison to an April 2023 that had five weekends. And though July 2024 as a whole saw visits down 1.5% YoY, a look at weekly foot traffic to Bloomingdale’s shows that throughout most of that month and into August, the chain continued to draw more visits than in 2023.

Macy’s, for its part, had a slower start to 2024 – with YoY monthly visits down through April 2024. But in May and June, Macy’s visit gap closed, with foot traffic just above 2023 levels. And though Macy’s also saw monthly YoY visits decline in July, the chain’s weekly foot traffic has remained at or above 2023 levels since the middle of the month – likely spurred by back-to-school shopping and sales.

With the upcoming holiday season expected to bring a surge in foot traffic, both Macy’s and Bloomingdale’s are well-positioned to capitalize on these opportunities and potentially drive further growth.

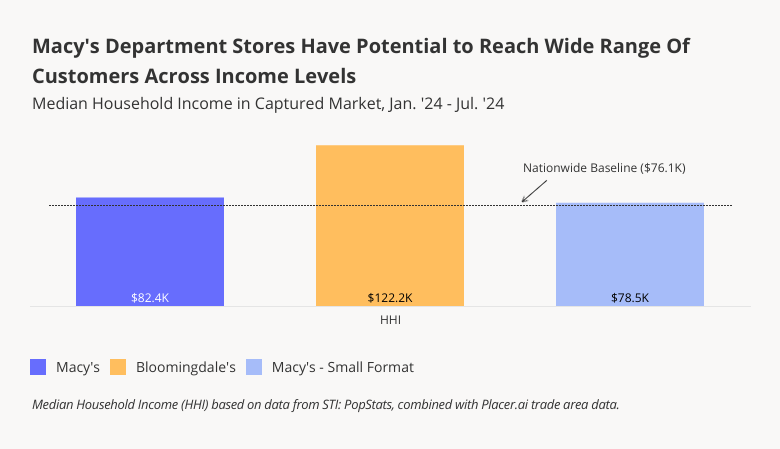

A Wide Range Of Incomes

Analyzing the median household incomes (HHI) of Macy’s and Bloomingdale’s captured markets shows how Macy’s, Inc.’s revitalization strategy is helping the company further diversify the range of options available for shoppers of all kinds underneath its umbrella.

Between January and July 2024, for example, luxury-focused Bloomingdale’s attracted visitors from areas with the highest median HHI of the three brands – $122.2K, well above the nationwide average of $76.1K. Bloomingdale’s affluent audience may be less prone to inflation-driven cutbacks than the average American, contributing to the chain’s stronger positioning this year.

By contrast, Macy’s shoppers came from areas with a median HHI of $82.4K, while visitors to Macy’s small-format stores (some 13 locations nationwide) came from areas with a median HHI of $78.5K – just above the nationwide baseline. By expanding its small-format footprint, Macy’s may succeed at increasing its draw among more average-income shoppers.

This income variation underscores the broad retail potential of each chain, ensuring that consumers can find options that cater to their specific needs across Macy’s diverse offerings.

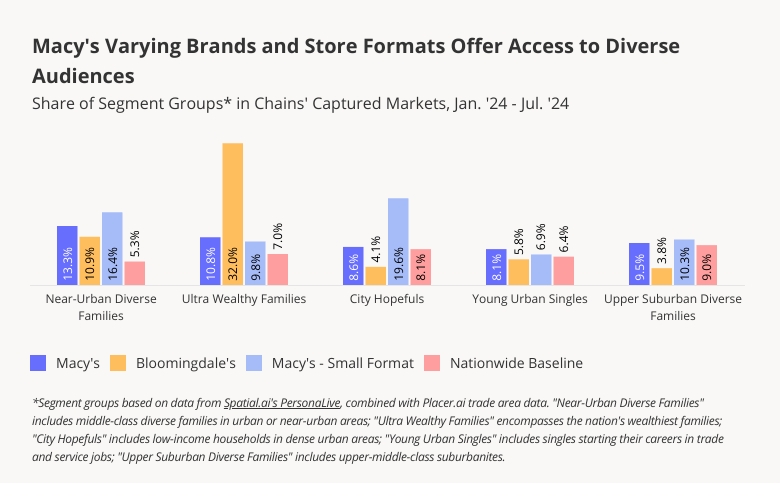

Blooming & Growing: The Bloomingdale’s Shopper

Analyzing the psychographic characteristics of Macy’s and Bloomingdale’s captured markets can shed additional light on how the chain’s turnaround strategy may help it reach new audiences. Macy’s traditional department stores already draw a diverse mix of consumers. But the addition of new Bloomingdale’s locations will help the company make further inroads into affluent segment groups like “Ultra Wealthy Families” – which makes up a whopping 32.0% of Bloomingdale’s captured market. At the same time, Macy’s smaller-format stores will offer the company greater access to the more modest-income “City Hopefuls” and “Near-Urban Diverse Families”, as well as the upper-middle-class “Upper Suburban Diverse Families”.

A Strategic Path Forward

Macy’s and Bloomingdale’s continue to adapt to shifting consumer preferences by focusing on their strengths in specific markets and among their demographic segments, and by expanding its small-format stores. With the holiday season approaching, can both chains continue to drive visits?

Visit Placer.ai to keep on top of the latest data-driven retail news.

.avif)