.svg)

In this blog, we dive into the latest location analytics and demographic data for luxury retailers and high-end department stores and take a closer look at consumer behavior in the upscale shopping space.

Seasonal Shopping Returns Stateside

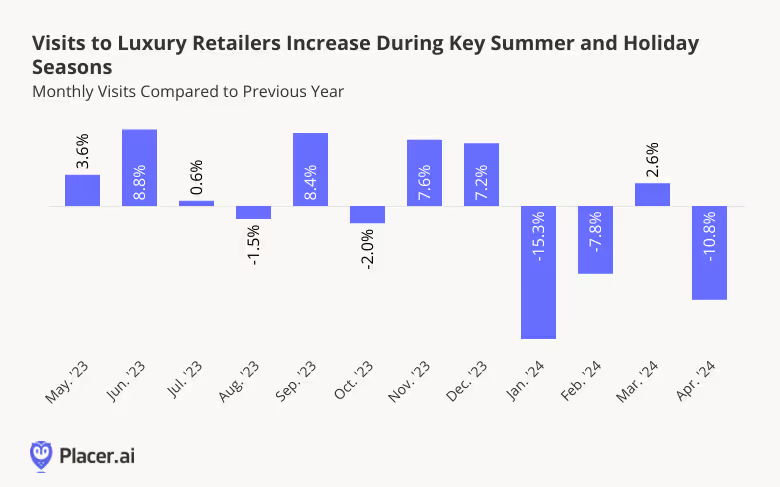

Over the past year, the Placer.ai Luxury Retail Index – including brands like Louis Vuitton, Tiffany & Co., and Chanel – saw year-over-year (YoY) foot traffic growth during crucial shopping seasons. May and June 2023 had significant increases in YoY visits, perhaps due to an influx of recreational shoppers on summer vacation, and July saw an uptick as well. YoY visits peaked again in November and December, likely reflecting the popularity of upscale retail corridors during the all-important holiday shopping season.

Some of this strength may be a result of affluent consumers refocusing their shopping on the U.S.: In 2022, many high-income shoppers chose to purchase big-ticket items abroad due to various economic benefits. But by 2023, demand for domestic luxury retail appeared to rebound, as some upscale retail clients “repatriated” their discretionary dollars.

To be sure, visit gaps re-emerged in some months of early 2024 – though these are partly attributable to factors like January’s unusually stormy weather and an April calendar shift. (April 2024 had one fewer Saturday than April 2023, providing less opportunity for visits in the highly discretionary category). But March 2024 also saw YoY visit growth. And given how well luxury retailers performed during their busiest months of year, the category may very well rally once again heading into the summer.

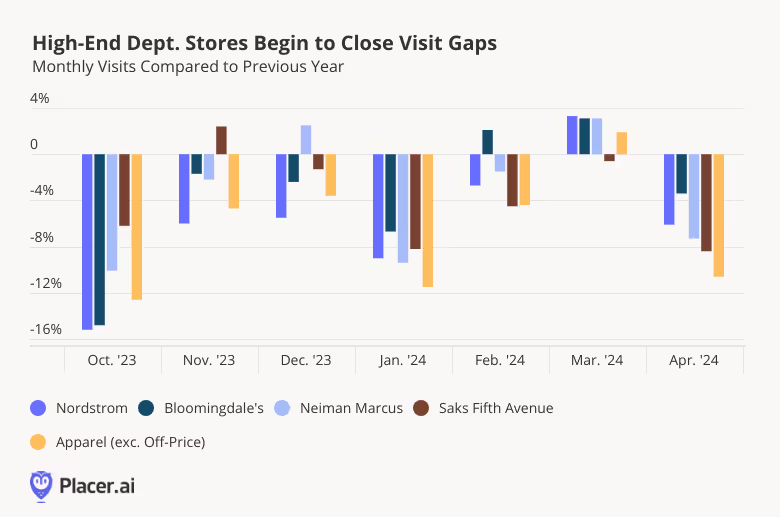

High-End Department Stores Close the Gap

Recent location intelligence also offers encouraging signs from the high-end department store space.

Like luxury retailers, high-end department stores saw narrowing visit gaps during the peak holiday shopping season – with Saks Fifth Avenue seeing a YoY uptick in November 2024, and Neiman Marcus seeing one in December.

In March 2024, YoY traffic turned positive for Nordstrom (3.3%), Bloomingdale’s (3.1%), and Neiman Marcus (3.1%), while Saks Fifth Avenue had just a -0.6% visit gap. And although April 2024 was a challenging month for the retailers, perhaps due in part to the calendar shift mentioned above, all four upscale department stores outperformed the traditional apparel category – another indication that high-end department stores may be poised for a comeback.

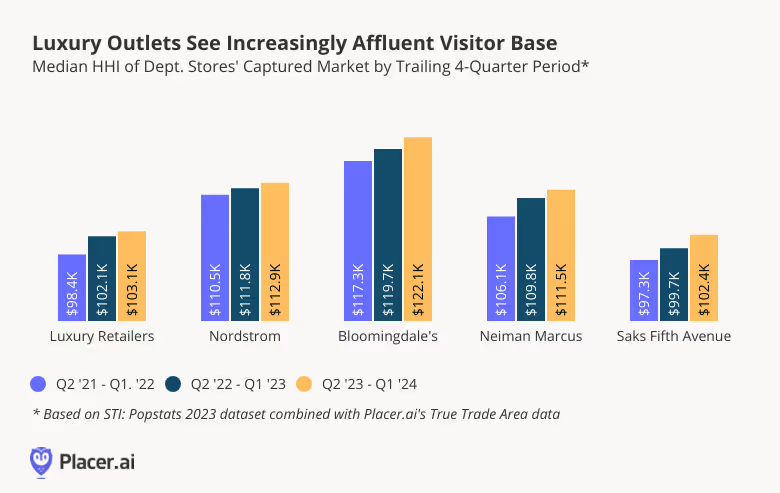

The Highest Earners Drive Traffic

Analyzing demographic changes in the captured markets of both luxury brands and high-end department stores indicates that increasingly affluent consumers are the main drivers of visits to the segment. (A chain’s captured market is obtained by weighting each Census Block Group (CBG) in its trade area according to the CBG’s share of visits to the chain – and so reflects the population that actually visits the chain in practice).

Over the last four quarters, visitors to luxury retailers and high-end department stores came from areas with higher median household incomes (HHIs) than in previous years. For example, during the period between Q2 2023 and Q1 2024, the median HHI of Bloomingdale’s captured market was $122.1K, an increase from $119.7K between April 2022 and March 2023, and $117.3K from April 2021 to March 2022.

In the face of recent inflationary pressures, aspirational luxury shoppers (who tend to be slightly less affluent) are likely quicker to adjust their behavior and trade down to more affordable brands. Meanwhile, prestige luxury shoppers – those with the highest incomes – tend to be relatively resilient, and so are able to continue shopping at their favorite luxury brands, driving up the HHI in these retailers’ trade areas.

Looking Ahead

Luxury retailers and high-end department stores have had recent foot traffic successes, while their clientele has become increasingly affluent. Will these brands continue their upward visit trajectories – and how will they leverage affluent foot traffic going forward?

Visit Placer.ai to find out.

.avif)