Insights into the physical world anchored in location analytics

INSIDER

Report

10 Top Brands to Watch in 2026Meet the ten retail and dining powerhouses, including H-E-B, Walmart, and Dave’s Hot Chicken, redefining success and winning consumer loyalty in 2026.

Placer Research

January 12, 2026

Industry Trends

Year-Over-Year Visits to Grocery Stores by State

Article

Article

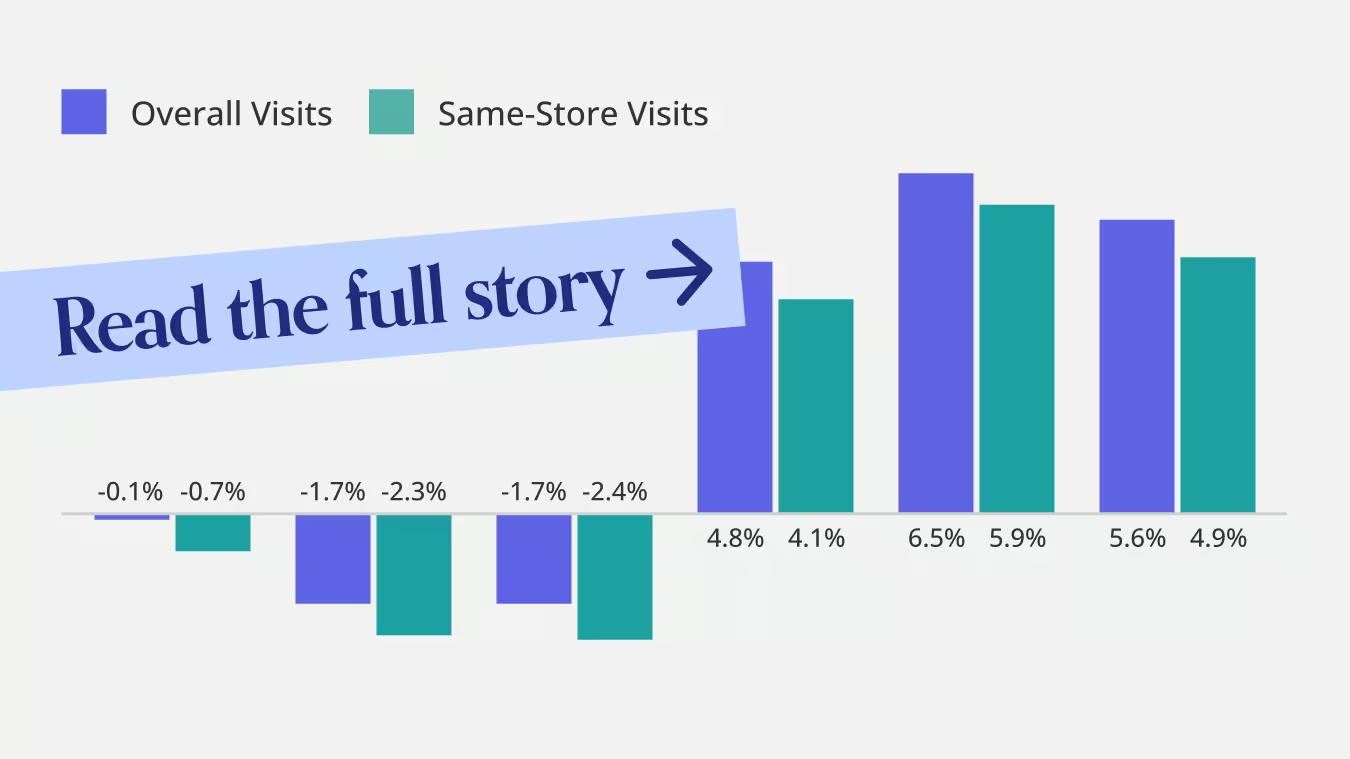

The Demand-Side Story Behind Saks Global’s BankruptcyThe Kroger Co, is a leading player in the grocery store space, operating its epon lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu

Shira Petrack

Jan 29, 2026

2 minutes

Executive Insights

Executive Insights

Visiting the Great OutdoorsThe Kroger Co, is a leading player in the grocery store space, operating its epon lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu

Caroline Wu

Jan 28, 2026

3 minutes

Article

.avif)

Article

Winter Storm Fern Sparked a Retail RushThe Kroger Co, is a leading player in the grocery store space, operating its epon lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu

Shira Petrack

Jan 27, 2026

3 minutes

Article

Article

Tractor Supply’s Demand-Driven ExpansionThe Kroger Co, is a leading player in the grocery store space, operating its epon lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu

Ezra Carmel

Jan 27, 2026

2 minutes

Latest Articles

_texasroadhouse_dine.png)

Article

Q4 2025 FSR Trends Emphasize Strategy, Value, and Footprint DisciplineShira Petrack

January 26, 2026

3 minutes

Article

Chipotle’s Growth Is No Longer Just About New RestaurantsLila Margalit

January 22, 2026

3 minutes

Article

What Other QSR Brands Can Learn From McDonald’s Loyalty StrategyShira Petrack

January 21, 2026

3 minutes

Article

Opportunity vs. Operational Reality in Dollar Tree's 99 Cents Only AcquisitionShira Petrack

January 20, 2026

3 minutes

.avif)

Article

Which Gym Is Right For You in 2026?Using AI-powered location analytics, we reveal which gyms are less crowded at peak times, skew younger or older, and attract the most singles.

Ezra Carmel

January 16, 2026

4 minutes

Article

Placer.ai December 2025 Office Index: ‘Tis the Season to WFHLila Margalit

January 12, 2026

3 minutes

Latest Reports

.png)

.png)

INSIDER

Report

5 Markets to Watch in 2026Find out why Salt Lake City, Reno, Indianapolis, Raleigh, and Tampa are Placer.ai's markets to watch in 2026.

Placer Research

December 5, 2025

INSIDER

Report

Retail Trends to Watch in 2026Which retail trends are set to define 2026? Using location intelligence, we explore the shifting patterns that could shape the retail landscape in the year ahead.

Placer Research

November 14, 2025

INSIDER

Report

Winning Holiday Shoppers in 2025: Key Insights for Advertisers and RetailersDive into the data to uncover the retail categories, audiences, and timing strategies poised to deliver high-impact campaigns this holiday season.

Placer Research

October 30, 2025

INSIDER

Report

What is Driving Discretionary Spending in 2025? See which discretionary retail categories are gaining momentum by delivering value, accessible upgrades, and immersive experiences.

Placer Research

October 2, 2025

INSIDER

Report

3 Trends Shaping the Grocery Sector Right NowDiscover the 2025 grocery sector trends driving growth across value, fresh, traditional, and ethnic formats. Learn how shifting consumer behavior, bifurcated spending, and short-trip missions are reshaping retail competition.

Placer Research

September 22, 2025

INSIDER

Report

Emerging Trends for CRE in 2025This Placer Snapshot examines the evolution of key industries impacting commercial real estate. We explore the shifting dynamics of office visits, the recovery of shopping centers, and population growth patterns across the United States in 2025.

Placer Research

August 28, 2025

.svg)