Insights into the physical world anchored in location analytics

INSIDER

Report

5 Grocery Growth Drivers in 2026How Expanded Supply, Trip Frequency, and Shopping Missions Are Reshaping Food Retail and Creating Multiple Paths to Growth

Placer Research

February 19, 2026

Industry Trends

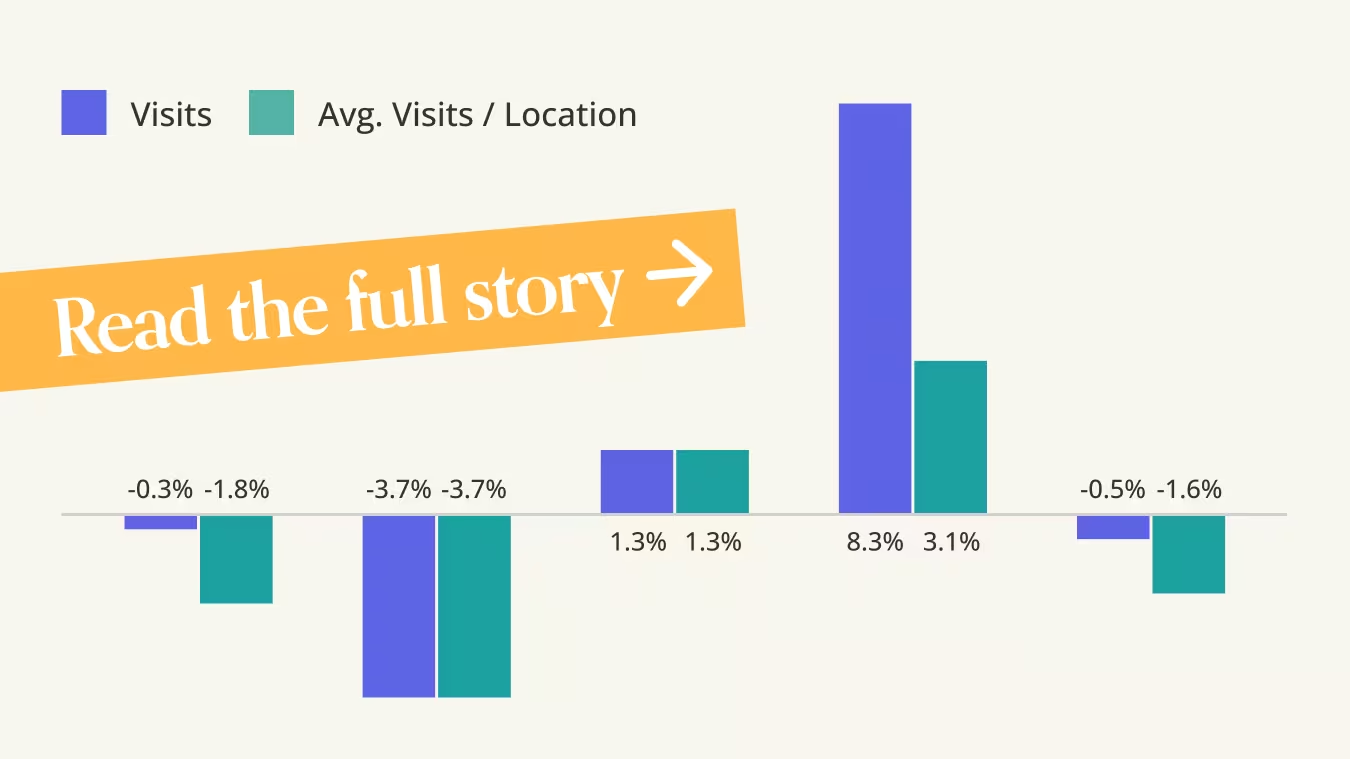

Year-Over-Year Visits to Grocery Stores by State

Article

Article

Continued Improvement in the Home Improvement SpaceThe Kroger Co, is a leading player in the grocery store space, operating its epon lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu

Ezra Carmel

Feb 20, 2026

1 minute

Article

Article

Placer.ai Overall Retail, E-Commerce Distribution, Industrial Manufacturing Index, January 2026The Kroger Co, is a leading player in the grocery store space, operating its epon lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu

Lila Margalit

Feb 19, 2026

3 minutes

Article

%20(1).avif)

Article

Clarity Wins as Off-Price Widens Its Lead Over Department StoresThe Kroger Co, is a leading player in the grocery store space, operating its epon lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu

Lila Margalit

Feb 18, 2026

3 minutes

Article

.avif)

Article

Dollar Stores, the New Face of the Holiday SeasonThe Kroger Co, is a leading player in the grocery store space, operating its epon lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu

Elizabeth Lafontaine

Feb 18, 2026

1 minute

Latest Articles

Article

Shake Shack in Q4 2025: Expansion-Led Growth With Stable Same-Store DemandLila Margalit

February 18, 2026

1 minute

.jpg)

Article

How Super Bowl Events Drove Foot Traffic and High-Value Tourism to the Bay AreaEzra Carmel

February 12, 2026

4 minutes

Article

Wingstop in Q4 2025: Speed Emerges as a Key Lever for GrowthLila Margalit

February 12, 2026

2 minutes

Article

Placer.ai January 2026 Office Index: Fern Puts RTO to the TestLila Margalit

February 11, 2026

3 Minutes

Article

How CAVA and sweetgreen are Sustaining Growth in Today’s Dining LandscapeEzra Carmel

February 10, 2026

3 minutes

Article

January 2026 Placer.ai Mall Index: Strong Start to 2026Shira Petrack

February 9, 2026

2 minutes

Latest Reports

.avif)

INSIDER

Report

Five Ways Retailers Can Leverage AI Without Losing What WorksRead the report to learn how AI is changing store roles, operations, marketing, and fleet strategy – and how to apply it without undermining what already works.

Placer Research

January 29, 2026

INSIDER

Report

10 Top Brands to Watch in 2026Meet the ten retail and dining powerhouses, including H-E-B, Walmart, and Dave’s Hot Chicken, redefining success and winning consumer loyalty in 2026.

Placer Research

January 12, 2026

INSIDER

Report

6 Coffee-Inspired Strategies That Can Reshape Dining in 2026Dive into the data to see how coffee became one of this year’s strongest dining performers – and explore strategies that can drive restaurant success across concepts in 2026.

Placer Research

December 18, 2025

INSIDER

Report

5 Markets to Watch in 2026Find out why Salt Lake City, Reno, Indianapolis, Raleigh, and Tampa are Placer.ai's markets to watch in 2026.

Placer Research

December 5, 2025

INSIDER

Report

Retail Trends to Watch in 2026Which retail trends are set to define 2026? Using location intelligence, we explore the shifting patterns that could shape the retail landscape in the year ahead.

Placer Research

November 14, 2025

INSIDER

Report

Winning Holiday Shoppers in 2025: Key Insights for Advertisers and RetailersDive into the data to uncover the retail categories, audiences, and timing strategies poised to deliver high-impact campaigns this holiday season.

Placer Research

October 30, 2025

.svg)