.svg)

Chicken restaurants have seen a huge surge in popularity over the past few years, from the epic Chicken Wars of 2021 to the impressive stateside success of international chains. And analyzing recent data indicates that fried chicken concepts are likely to continue as a top growth segment in 2025 as well.

We dove into the visit numbers to see how the segment is faring and highlighted some of the chains making the biggest splash.

Fried, Battered, and Crispy

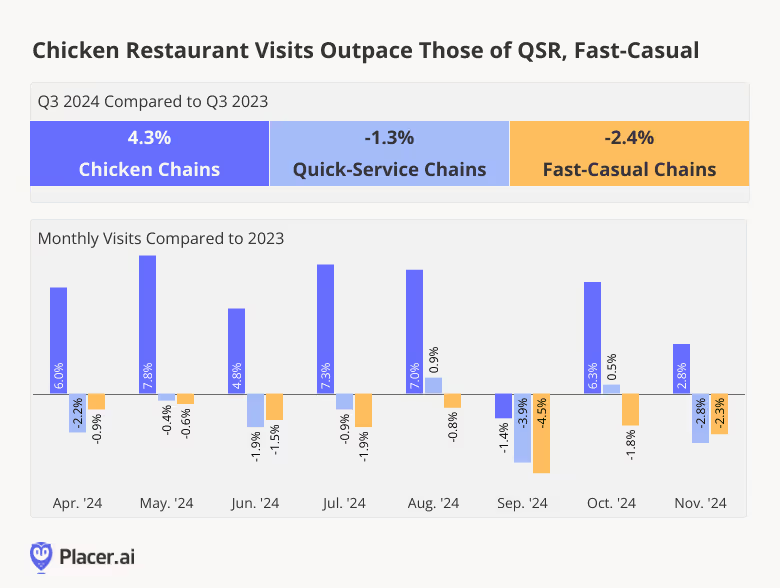

In a dining segment that’s faced its fair share of challenges of late, chicken restaurant chains are standing out. Visits to QSR and fast-casual chicken chains consistently outperformed the wider fast-casual and QSR segments in terms of YoY visits, with the chicken category seeing a 4.3% YoY traffic boost in Q3 2024.

As diners continue to prioritize convenient and affordable meals in the face of continued economic uncertainty, chicken-centric restaurants – which offer both value and speed – seem well-positioned to continue thriving.

A Clucking Success

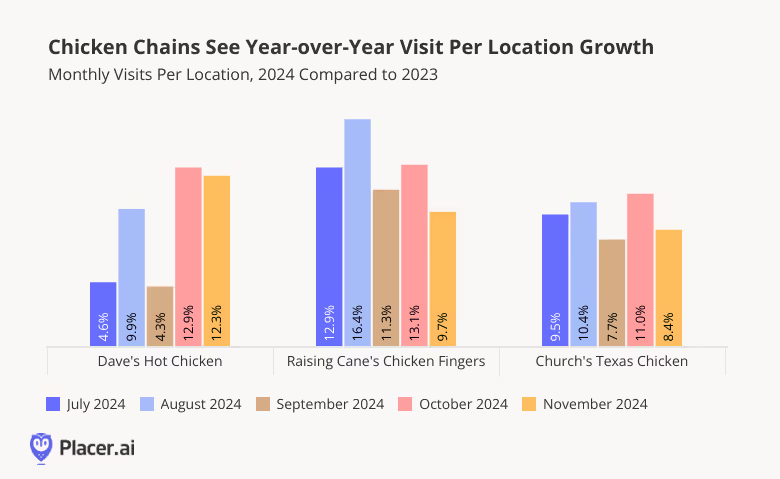

Diving into the visitation data for some of the category’s chicken leaders reveals that many of the bigger names in the game are not only growing their storefleet – they’re also continuing to drive more visits to each location.

Dave’s Hot Chicken, Raising Cane’s Chicken Fingers, and Church’s Texas Chicken each attract millions of visits to their brick-and-mortar location every month – and traffic is steadily growing thanks to the three chains' expanding footprint. And location analytics reveal that these brands are also seeing strong growth in monthly visits per location – highlighting the impressive demand for fried chicken and showcasing these companies’ ability to grow their consumer base through fleet expansions.

Size Isn’t Everything: Smaller Chains Seeing Fried Chicken Success

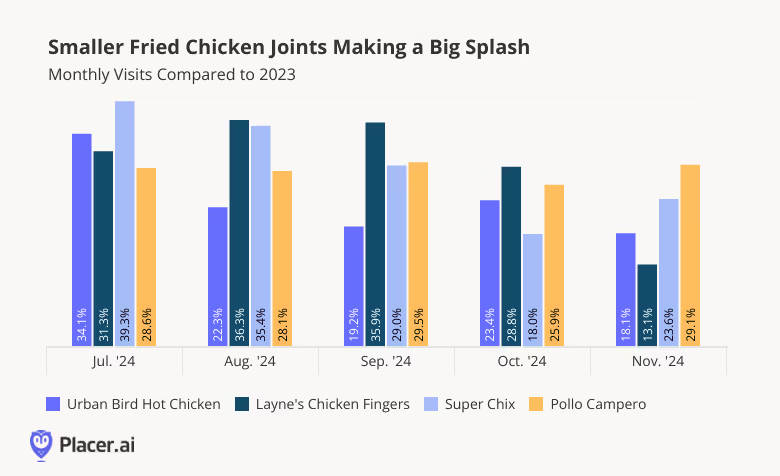

Another indication of the fried chicken market’s continued growth potential comes from the success of smaller brands flourishing alongside the category leaders. Chains like Pollo Campero, Urban Bird Hot Chicken, Layne’s Chicken Fingers, and Super Chix may not be competing with industry leaders yet – but their impressive YoY visit growth highlights consumers’ current appetite for fried chicken franchises.

The four analyzed chains enjoyed strong monthly visits in 2024 relative to 2023, with November 2024 visits elevated between 13.1% and 29.1% YoY.

Whether these smaller chains are fueling their growth by offering an innovative twist on the traditional fried bird or benefiting from homegrown loyalty, the bottom line remains clear. Despite operating in a market that's getting more crowded by the day, there's ample opportunity for new players to throw their feathered caps in the ring.

The Top Of The Pecking Order

The fried chicken segment remains a high-demand category, evidenced by the segment’s strong visit performance over the past year. With fried chicken chains continuing to expand across the country, will they maintain their visit dominance? Or will the cluck stop somewhere?

Visit Placer.ai to stay up-to-date with the latest data-driven dining insights.

Darden Restaurants Inc. is the largest full-service restaurant group in the country, operating ten dining chains that range from fine dining to casual bars.

How has the company fared in recent months? We examined the location analytics to evaluate Darden’s recent performance and took a closer look at what the holiday season might bring for its wide array of brands.

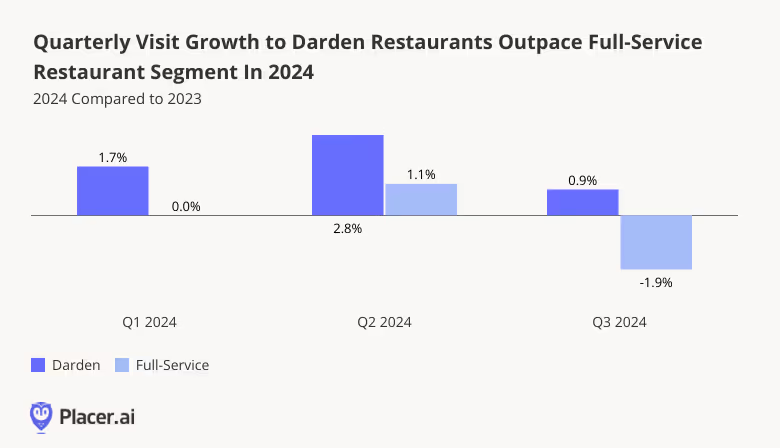

Darden Outpaces the Full-Service Restaurant Segment in Q3 2024

The full-service restaurant category has faced significant challenges in recent years as rising food prices, labor shortages, and inflation pushed costs up and some customers away. But since the beginning of 2024, Darden has managed to stay ahead and outpace the wider full-service restaurant segment in terms of year-over-year (YoY) quarterly visits. Q3 2024 visits were 0.9% higher than in Q3 2023. In contrast, the broader full-service segment experienced a 1.9% decline in the same period.

As restaurant inflation finally begins to cool and the dining segment tiptoes cautiously toward recovery, Darden’s ability to stay ahead of the competition suggests that its brands are resonating with customers even during periods of economic uncertainty.

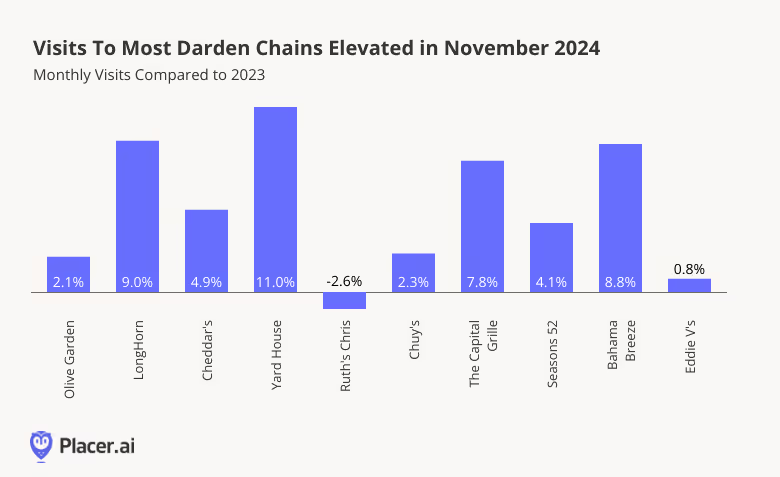

November’s Momentum Across Chains

Darden’s portfolio runs the gamut from household names like Olive Garden (with over 900 locations) and LongHorn Steakhouse (over 500 locations) to smaller chains like Yard House and Bahama Breeze. And zooming in on the recent November data reveals that most chains are still enjoying year-over-year (YoY) visit growth. Yard House led the pack with 11.0% more visits than in November 2023, followed by LongHorn Steakhouse (9.0% YoY growth), and Bahama Breeze (8.8% YoY growth).

This steady November momentum bodes well for Darden as the typically busy holiday season approaches.

Darden’s December Spike

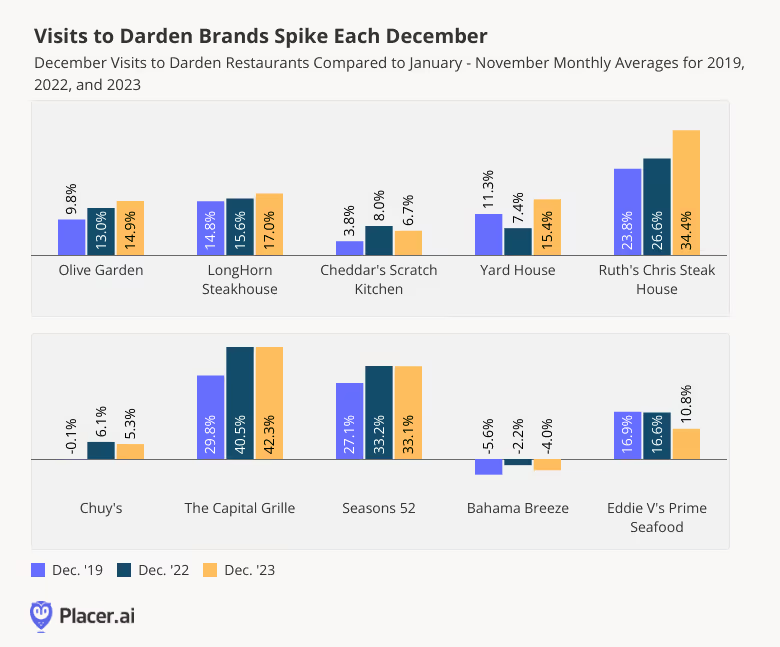

Indeed, diving into previous years’ visitation patterns reveals that Darden’s brands generally receive sizable visit bumps over the holiday season.

Analyzing December visits in 2019, 2022, and 2023 relative to each year’s January to November monthly visit average highlighted significant visit boosts across almost all Darden brands. The Capital Grille led the charge in December 2023, with visits 42.3% higher than the January to November average, followed closely by Ruth’s Chris Steak House (34.4%) and Season’s 52 (31.1%).

These consistent December traffic spikes coupled with November’s strong showing suggests that the company is well-positioned to sustain its current momentum into the holiday season and beyond.

Final Thoughts

Darden Restaurants continues to be a leader in the full-service segment, enjoying visit growth and capturing holiday foot traffic.

Will this year’s holiday season bring increased foot traffic to the company’s brands?

Visit Placer.ai to keep up with the latest data-driven dining insights.

Shoppers continue to prioritize value in 2024, offering opportunities for discount and dollar stores to thrive during the upcoming holiday season.

With that in mind, we took a look at visitation metrics – both from 2024 and from previous years – to see how the segment is performing and what the crucial holiday season might hold for discount retailers Dollar Tree and Dollar General.

Foot Traffic Shows No Signs of Slowing

Discount and dollar stores continue to benefit from an inflation-impacted economy, with category leaders like Dollar Tree and Dollar General continuing to expand their footprints to serve the increasing number of budget-conscious shoppers.

And in large part thanks to the increased store count, visits to Dollar Tree and Dollar General have continued to increase – Q3 2024 visits to the chains were up by 5.3% and 4.8% YoY, respectively. Monthly visits also showed impressive growth, with October 2024 visits up by 7.6% at Dollar Tree and 7.8% at Dollar General. These growth numbers may be slightly lower than the visit increases posted by the category in the past – but the ongoing positive performance by discount & dollar store leaders indicates that the category remains one of the most consistently strong players in the wider retail space.

When Do Visits Get Their Biggest Boosts?

November and December are typically the most important months for retailers as multiple shopping events – Turkey Wednesday, Black Friday, Christmas Eve Eve, and Boxing Day – drive consumers to the tills. And while many retailers open the holiday season with visit spikes driven by big Black Friday discounts, the visitation patterns look slightly different at discount chains, where prices are already low and discounts are – as their name implies – already applied. So when do these retailers get their holiday visit boosts?

Comparing weekly visit numbers in 2021, 2022, and 2023 to each year’s weekly average reveals differences between the two discount & dollar store leaders. Visits to Dollar Tree gradually increase from early November onward and peak on the last full week before Christmas, likely driven by shoppers flocking to its stores to pick up snacks, gift wrap, and stocking stuffers. Meanwhile, Dollar General’s visits exhibited more stability – although visits were higher than average between Black Friday and Christmas Eve Eve, the increase was much more muted relative to Dollar Tree’s holiday spike. Dollar General’s softer holiday traffic may be due to the expansion of its Dollar General Market concept, which turned many of its stores into destinations for fresh foods – so consumers may be treating Dollar General more like a grocery store and less like a holiday shopping spot.

Previous years’ visitation patterns indicate that the busiest time of the year is still ahead for Dollar General and Dollar Tree. How will these retailers perform during the critical pre-Christmas rush? Visit Placer.ai to find out.

The Kroger Co. has come a long way from its humble beginnings as a single grocery store in downtown Cincinnati, Ohio, in 1883. Today, the brand operates over 2,700 stores under its numerous grocery store banners.

We analyzed the visitation patterns at some of Kroger’s largest chains to see how these brands have fared over the past few months, and looked at what last year’s visit data can tell us about the upcoming Thanksgiving holiday.

Visits To Kroger Banners Show Stability in Q3

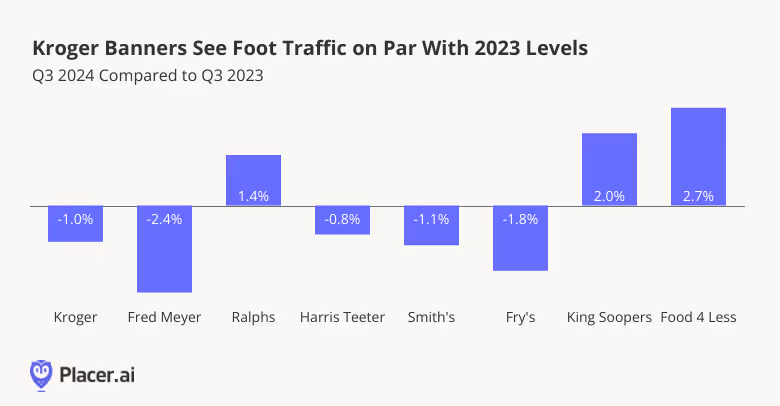

The Kroger Co.’s various grocery banners vary in size and scale, with its eponymous banner Kroger – more than 1200 stores across much of the midwest and south – attracting the largest visit share relative to the company’s full grocery portfolio. Kroger’s other major regional chains, including Harris Teeter (mid and south atlantic states); Ralphs (California), King Soopers (primarily Colorado), Food 4 Less (California, Illinois, and Indiana), Smith’s (Mountain states), Fry’s (Arizona), and Fred Meyer (Pacific northwest), lend the company considerable presence nationwide.

On the whole, visits to the analyzed Kroger chains remained fairly close to 2023’s levels, with visits to Kroger, Fred Meyer, Harris Teeter, Smith’s, and Fry’s sustaining minor YoY visit gaps. No-frills value chain Food 4 Less enjoyed 2.7% YoY visit growth in Q3, likely buoyed by the same trading down behaviors that have propelled growth at other low-cost supermarkets this year. Ralphs and King Soopers also saw YoY visit growth, perhaps aided by California and Colorado’s relatively high median household incomes (HHIs) – $94.1K and $89.1K, respectively, according to data from STI: PopStats, compared to the nationwide baseline of $76.1K.

Shoppers Lingering at Discount, Hypermarket Options

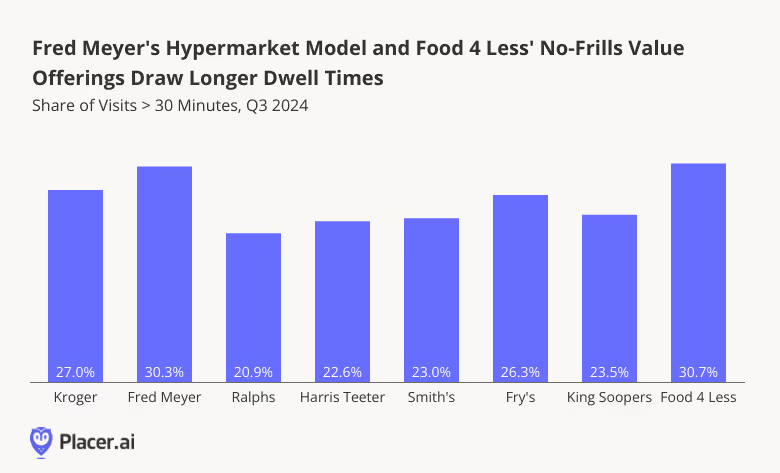

Kroger’s extensive reach allows it to appeal to a wide range of grocery shoppers. The company operates both discount grocery chains, such as Food 4 Less, more upscale ones like Harris Teeter, and everything in between.

Diving into the share of visits lasting 30 minutes or longer at individual Kroger banners reveals substantial variation, with Fred Meyer and Food 4 Less receiving the highest shares of long visits among the analyzed chains. In Q3 2024, 30.3% of Fred Meyer visits and 30.7% of Food 4 Less visits lasted over 30 minutes – a stark contrast to Ralphs (20.9%), Harris Teeter (22.6%) and King Soopers (23.5%).

This variance in dwell times may reflect the differing offerings of each chain. Hypermarket Fred Meyer provides a wide range of services beyond groceries – including pharmacies, department stores, and jewelry offerings – which could encourage shoppers to spend more time exploring. And Food 4 Less falls squarely into the discount grocery segment, one that often sees customers spending more time in-store searching for the best deals.

Turkey Wednesday Poised to Bring the Crowds

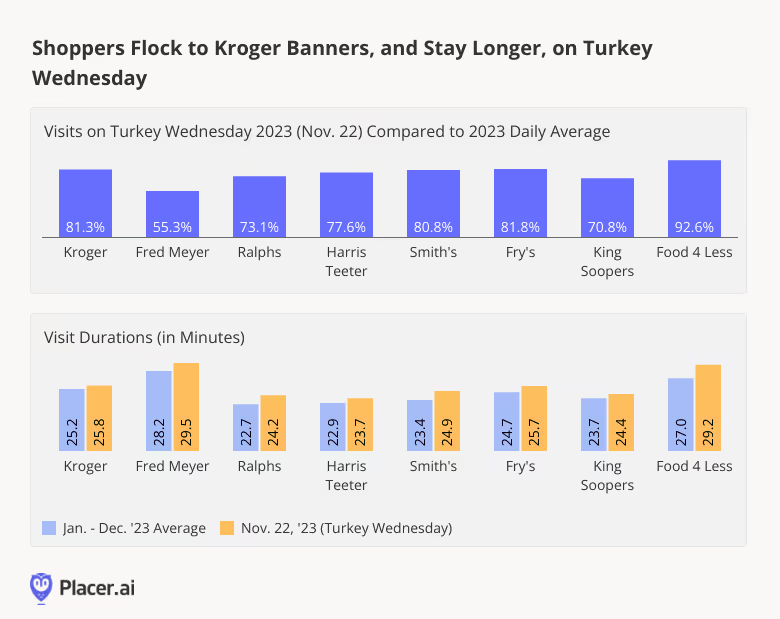

While not (yet!) an official holiday, Turkey Wednesday – the day before Thanksgiving – is one of the most important days of the year for grocers as shoppers flock to stores to pick up last-minute items for their upcoming feasts.

And while Thanksgiving is still over a week away, analyzing trends from previous years can help grocers prepare for the coming frenzy. On November 22nd, 2023 – the day before Thanksgiving – visits across all analyzed Kroger chains shot up between 55.3% and 92.6% compared to the daily visit average for 2023. And visitors at each of the chains stayed longer in-store than they typically did during the rest of the year.

With visits to Kroger’s major banners either nearly on par with or ahead of last year’s levels, the company appears well-positioned to enjoy another year of strong Turkey Wednesday visits.

Final Thoughts

If previous years are any indication, Kroger’s grocery banners should be preparing for a surge in Thanksgiving shopping. Will visits outpace those of last year?

Visit Placer.ai to keep up with the latest data-driven grocery insights.

.avif)

Last year’s holiday shopping season was an impactful one, with many categories seeing record-breaking sales and visits. And perhaps no category benefits from Q4 peaks quite like department stores, which see major foot traffic spikes on Black Friday and in the run-up to Christmas.

So with Q4 2024 seemingly primed to be another strong season, we took a look at department store visitation patterns this year and during previous holiday seasons to see what might lie ahead for the category in the coming weeks.

Predictable Seasonal Patterns

The holiday shopping calendar often begins as early as October, as consumers start preparing for Halloween before shifting their focus to Thanksgiving, Black Friday, and Christmas. This time of year tends to be one of the busiest for many retailers, as it encompasses a variety of shopping needs, including gifts and seasonal celebrations.

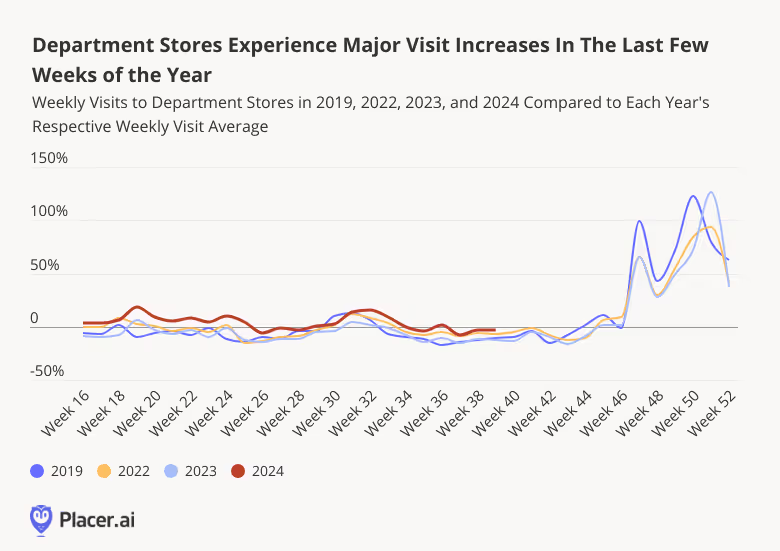

And one retail category that sees major visit increases every holiday season is department stores. Chains like Nordstrom, Macy’s, and Bloomingdale’s experience substantial spikes in visits throughout Q4 as shoppers flock to their locations to take advantage of sales and find gifts for their loved ones.

And though consumers’ holiday shopping behavior varies somewhat each year, analyzing weekly fluctuations in visits to department stores reveals some predictable patterns. Every year, visits to department stores see modest increases during major retail events like Valentine’s Day, Mother’s Day, and back-to-school shopping season – before surging during the week of Black Friday (week 47) and then again in the run-up to Christmas. During the week of last year’s Black Friday, for example, department store visits soared 65.2% above the 2023 weekly average – only to go even higher (122.8%) during the week before Christmas (week 51).

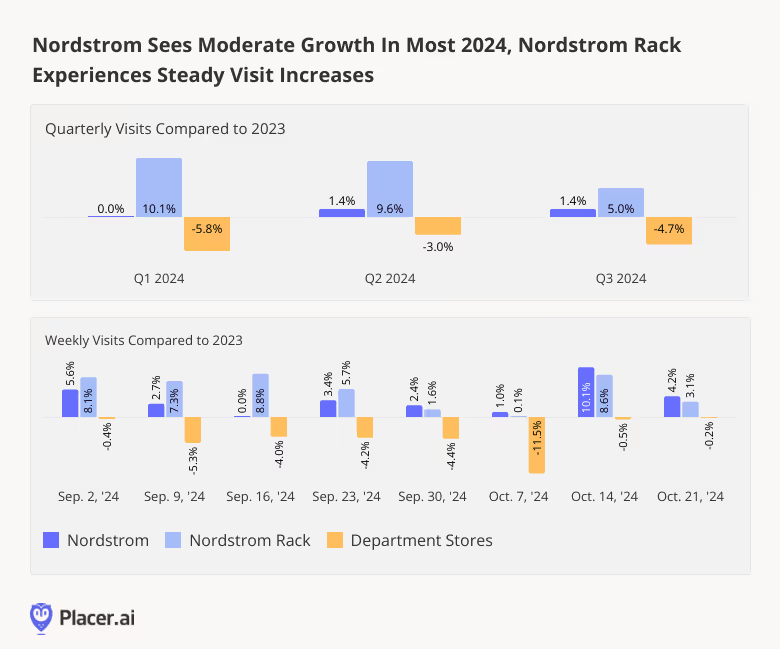

Nordstrom Picks Up The Pace

Nordstrom is one department store that seems poised to enjoy a particularly robust holiday shopping season this year. The chain, which operates more than 90 of its namesake stores, also has an off-price banner – Nordstrom Rack – with over 250 locations. And both brands have enjoyed stable visit growth since April 2024 – with quarterly YoY visits to Nordstrom and Nordstrom Rack elevated by 1.4% and 9.6%, respectively, in Q2 2024, and by 1.4% and 5.0%, respectively, in Q3 2024. By contrast, the wider department store category sustained consistent YoY visit gaps.

Drilling down deeper into weekly visit data shows that this positive trend continued into October. And while Nordstrom Rack – which is firmly in expansion mode – outperformed Nordstrom’s traditional stores through September, this trend reversed slightly in October, as the holiday season grew closer. With Black Friday just around the corner, both chains seem well positioned to continue driving visits to their respective stores.

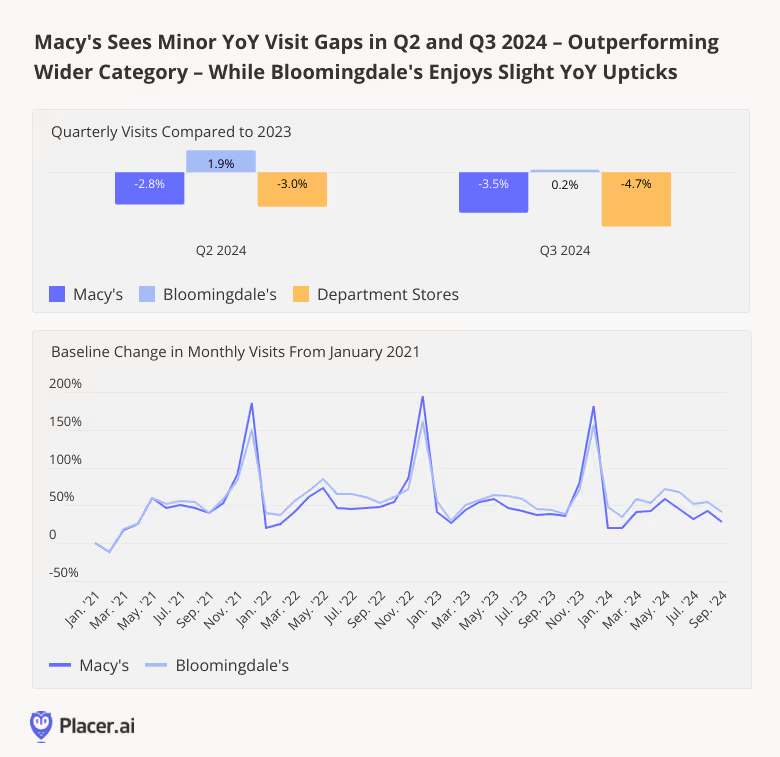

Macy’s “Bold New Chapter” in Play?

Macy’s Inc., for its part, is doubling down on its “Bold New Chapter” – a turnaround strategy involving a significant trimming of the company’s traditional Macy’s portfolio and the addition of several Bloomingdale’s and small-format stores. In August, Macy’s announced its intention to increase to 55 the number of Macy’s locations slated for closure by the end of 2024. And though the plan’s implementation is still in early stages, foot traffic data suggests that both Macy’s and Bloomingdale’s are holding their own.

In Q2 and Q3 2024, Macy’s sustained minor YoY visit gaps – 2.8% and 3.5%, respectively – slightly outperforming the broader category. Meanwhile, Macy’s high-end Bloomingdale’s brand saw a YoY visit uptick of 1.9% in Q2, while Q3 visits remained flat compared to 2023. And given the huge monthly visit spikes both chains experience each year in November and December, Macy’s and Bloomingdale’s appear well positioned to once again experience a surge in foot traffic as the holiday season begins.

Final Thoughts

If previous years are any indication, department stores should be getting ready for significant foot traffic increases as the holidays quickly approach. Will improving consumer sentiment and cooling inflation lead to visit increases at department stores, or will consumers decide to take it easy this year?

Visit Placer.ai to keep up with the latest data-driven retail insights.

The holiday season is right around the corner, bringing with it some of the most impactful shopping periods of the year. We took a closer look at visit performance across major wholesale clubs and superstores – Target, Walmart, Sam’s Club, BJ’s Wholesale, and Costco – to see what their 2024 performance and past holiday season visit patterns can tell us about what to expect this Q4.

Wholesalers Outperform Superstores in Q3 2024

Warehouse clubs have been thriving in 2024, buoyed by price-conscious consumers eager to load up on inexpensive essentials. In Q3, quarterly visits to retail giants Sam’s Club and BJ’s Wholesale rose 5.2% and 5.9%, respectively. And Costco, holding its place ahead of the pack, saw a foot traffic increase of 7.2%. For all three chains, the robust visit growth continued into October, with visits up 3.6% to 5.9% YoY.

Meanwhile, Target and Walmart saw respective quarterly YoY foot traffic upticks of 1.0% and 0.9% in Q3 2024. In August – the height of the back-to-school shopping season – visits to both chains increased just over 3.0% YoY. And though foot traffic to the superstore behemoths slowed in September as the summer rush abated, Target saw its visit gap narrow once again in October, while Walmart experienced a slight 0.2% increase.

Historic Holiday Season Visit Spikes

Warehouse retailers have been the clear foot traffic winners this year – but digging deeper into historical data suggests that it is Target that is primed to experience the busiest holiday season of the analyzed chains.

During the week of November 20th, 2023 – the week of Turkey Wednesday and Black Friday – visits to Target soared 18.9% compared to the chain’s 2023 weekly visit average, marking the biggest pre-Thanksgiving visit spike of any of the analyzed chains.

But Target’s real visit surge came during the week of December 18th – the week before Christmas, including the all-important Super Saturday – when visits to Target surged 87.3% above the chain’s 2023 weekly visit average. This was more than double the relative increase experienced by Walmart (39.6%), Sam’s Club (32.8%), BJ’s Wholesale (32.3%), or Costco (34.1%). And with recent visits to Target on par with – or slightly above – last year’s levels, the retail giant is likely poised to win the holidays once again.

Regional Holiday Shopping Patterns

Overall, Super Saturday was a bigger milestone for Target last year than Black Friday. (On the former, visits surged 166.1% compared to a 2023 daily average, while on the latter they rose 135.3%.) But digging deeper into the data reveals significant regional differences in Target’s performance on the two major shopping days.

In some parts of the country – including several midwestern, south central, and nearby states where Black Friday has special resonance – the day after Thanksgiving drew bigger visit spikes than Super Saturday. Some markets in particular saw outsized Black Friday visit surges, including West Virginia (348.6%), Kentucky (232.3%), and Indiana (227.4%). Other markets, such as California (74.6%) and Colorado (89.5%), experienced more moderate – though still substantial – Black Friday jumps.

In contrast, visits to Target on Super Saturday were more evenly distributed across the country, with several western and sunbelt states recording substantial visit increases – including New Mexico, which saw a 200.6% jump in visits to Target on December 23, 2023 compared to the 2023 daily visit average.

Ready, Set, Shop!

With solid Q3s under their belts, Target, Walmart, Costco, Sam’s Club, and BJ’s Wholesale Club are all well-positioned to enjoy a robust holiday season this year. Will the retail giants deliver?

Follow Placer.ai’s data-driven retail analyses to find out.