.svg)

2024 represented a year of transformation in U.S. luxury retail. After years of evading the impact of inflation and changing consumer behavior, ultra luxury brands and retailers began experiencing some of the challenges plaguing the wider retail space over this past year. Consumers of all income groups pulled back on spending and shifted focus towards value, which is inherently at odds with the luxury retail experience. Despite the aspirational nature of social media, many consumers who had been testing the waters of the luxury market can’t sustain their demand. There’s also been a rebound of the “accessible” luxury market, with brands like Coach and other smaller chains capturing the attention of the consumer.

How did 2024 end in terms of luxury retail visitation? Generally, visitation to luxury retail brands was down throughout the year, with visits for 2024 as a whole down 4% year-over-year. This is in stark contrast to the growth in visits we observed in 2022 and 2023, a clear signal that there’s been a shift in consumer demand for luxury brands here in the U.S. The elasticity of luxury visits waned in 2024, which could be attributed to a few factors; changes in demand for specific brands this past year or lower general demand for the categories.

The most interesting shift this past year was in the segmentation of visitors to luxury retailers. Using PersonaLive visitor segments, we observed changes in the types of demographic consumer segments visiting luxury brands. The percentage of visits by Ultra Wealthy Families increased over the past three years, with the cohort making up 20% of luxury retailers’ captured market in 2024, the largest of any visitor segment.

At the same time, we noted decreases in the share of Near-Urban Diverse Families, Young Urban Singles, and City Hopefuls in luxury retailers’ trade areas. These groups fall more into the aspirational customer segment for luxury brands, meaning that they might not be frequent shoppers or may have saved up for a large purchase. Luxury retailers now have to rely more on their traditional consumer base and have narrowed their pool of potential visitors.

Beyond the retailers themselves, luxury shopping centers also saw visitation decelerate in 2024. Looking at three key luxury centers, Americana Manhasset in Manhasset, NY, Bal Harbour Shops in Miami, and Highland Park Village in Dallas, each center slowed down compared to prior years. These shopping centers house ultra luxury brands, such as Hermes, Dior, and Chanel, as well as new luxury entrants like LoveShackFancy and beauty chain Bluemercury as well as upscale dining options; despite this strong mix of tenants, it’s clear that changing consumer behavior has impacted these centers, even those that still saw growth early in the year.

There weren’t any observable changes in visitor behavior in terms of how long visitors stayed or what day of the week they visited. All three luxury shopping centers rely heavily on weekend visitors, and as consumers pull back on the frequency of discretionary purchases, there might be less incentive to visit overall. More than 50% of Americana Manhasset and Highland Park Village’s trade area is made up of Ultra Wealthy Families, and that high concentration that once benefited luxury retailers may now present hurdles in sustaining traffic growth.

Luxury brands, despite the changing tides, are the true retail trend setters, and have the ability to pivot as needed to meet changing consumer demands. In 2024, we saw the triumphant rise of brands such as Miu Miu, Louis Vuitton and Hermes as consumers concentrated their purchases around the hottest labels. The luxury market faces more uncertainty in 2025 as the consumer fluctuates to adapt to changes across the U.S. and the need to provide a high touch experience and inherent value is critical to garner the attention of shoppers.

The Container Store has been a prime example of a specialty retailer that successfully catered to a highly specific and niche consumer need. The home organization trend gained traction in the early 2000s with the rise of custom closet solutions and continued to grow in popularity through influential figures like Marie Kondo and The Home Edit.

The home furnishings category experienced a surge during the pandemic as consumers focused on improving their living spaces, whether by purchasing new homes or renovating existing ones. However, as discretionary spending habits have normalized and interest rates have risen, consumer spending in this category has declined.

Additionally, the sector has seen significant consolidation, most notably with the closure of Bed Bath & Beyond, a major player in home furnishings and organization. The remaining retailers in the space now largely fall into two distinct categories: niche specialists and value-driven brands..

Those retailers that play in the more niche space – including The Container Store – have had an even more challenging path to meet changing consumer needs. Despite offering a high level of customization and expertise, the chain has struggled against increasing industry-wide promotional activity and waning interest in the home organization category. Additionally, mass merchants and other home retailers have expanded their offerings in this space, providing organization solutions at price points that better align with today’s cost-conscious consumers.

Placer’s foot traffic estimates indicate a clear rise in competition for The Container Store since 2022, aligning with a broader decline in demand for its category. In 2024, visitors to The Container Store cross-shopped at Target, HomeGoods, IKEA, and World Market at higher rates than in 2022. This growing preference for competitive alternatives – many of which emphasize greater value – has likely contributed to the retailer’s challenges.

Specialty retailers play a crucial role in the industry by offering expert knowledge, superior service, and a wider assortment of products. However, as we move into 2025, the retail landscape must continue evolving to meet shifting consumer expectations, making adaptation essential for specialty retailers.

As we discussed before the 2024 holiday season began, timing was expected to play a crucial role in its success for retailers. With one less week between Thanksgiving and Christmas, retailers faced the challenge of consolidating promotions and focusing on attracting repeat visits and increasing conversion rates to match last year’s performance. But another factor influencing holiday timing is the elongation of seasonal offerings and promotions, which now extend well into October. While there’s no industry-wide standard for when the holiday season officially begins, it’s clear that many retailers recognize the value of starting their campaigns in October and early November to maximize engagement and sales.

When analyzing visitation trends throughout the holiday season, the narrative shifts depending on the time frame considered. From Black Friday through Christmas Eve, most categories experienced double-digit traffic declines compared to last year, partly due to the shorter holiday season. But focusing on the period between October and the Wednesday before Thanksgiving reveals that visitation to many categories increased by double digits compared to last year. While this time frame includes an additional week this year, it’s evident that some demand shifted into the earlier part of the holiday season.

And when looking at performance for the extended holiday season as a whole – from October 1 through Christmas Eve – year-over-year traffic performance improved across the board, with many categories actually showing growth compared to 2023.

There was particularly strong performance in discretionary categories during October and early November, including luxury department stores, beauty chains, and home furnishing retailers. These early gains provided the momentum many chains needed to help offset the impact of the shorter traditional holiday season.

The extended shopping season successfully contributed to overall traffic growth for many retail sectors and may signal that consumers are willing – and able – to start their holiday shopping earlier if the right products and promotions are available.

The holiday shopping season is in full swing, and with Black Friday weekend behind us, it's time to assess how this season is shaping up for retailers. As we noted before Thanksgiving, the shortened window between Thanksgiving and Christmas this year places added pressure on retailers to drive store traffic during key holiday events and weekends.

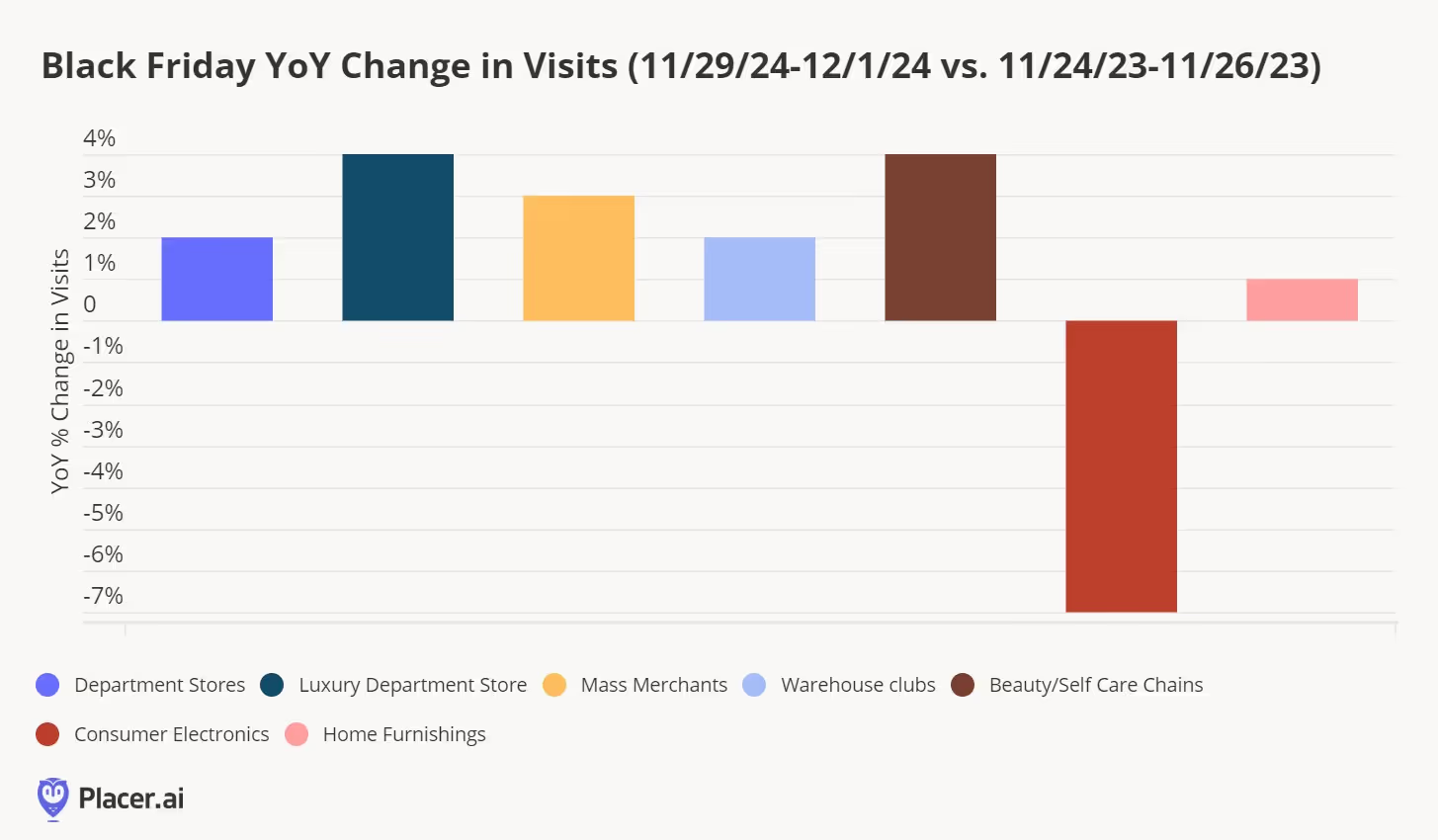

In 2023, Black Friday accounted for approximately 7% of holiday season retail visits, making it crucial for retailers this year to attract consumers early to mitigate potential slowdowns later in the season. Without burying the lede, Black Friday weekend (Friday through Sunday) delivered on this goal, with six of the seven analyzed retail sectors experiencing visitation growth. While the fervor around Black Friday may not match the excitement of the 1990s and 2000s, this year reaffirmed its enduring importance as a cornerstone of holiday shopping.

From a category perspective, luxury department stores had a strong performance this year, with traffic up 4% compared to Black Friday weekend last year. Nordstrom, in particular, stood out with a successful event. Throughout 2024, luxury department stores have worked hard to align more closely with consumer expectations in terms of assortment, in-store experience, and value, which clearly paid off during this key retail event. According to PersonaLive segmentation, Ultra Wealthy Families made up a quarter of visitors to luxury department stores during Black Friday weekend, bolstering traffic as these consumers tend to be less price-sensitive.

Full-line department stores, mass merchants, beauty, and home furnishing retailers also saw a 2-3% increase in traffic year-over-year. Overall, while discretionary retail still faces challenges, the weekend showed more positive momentum than we've seen in recent years.

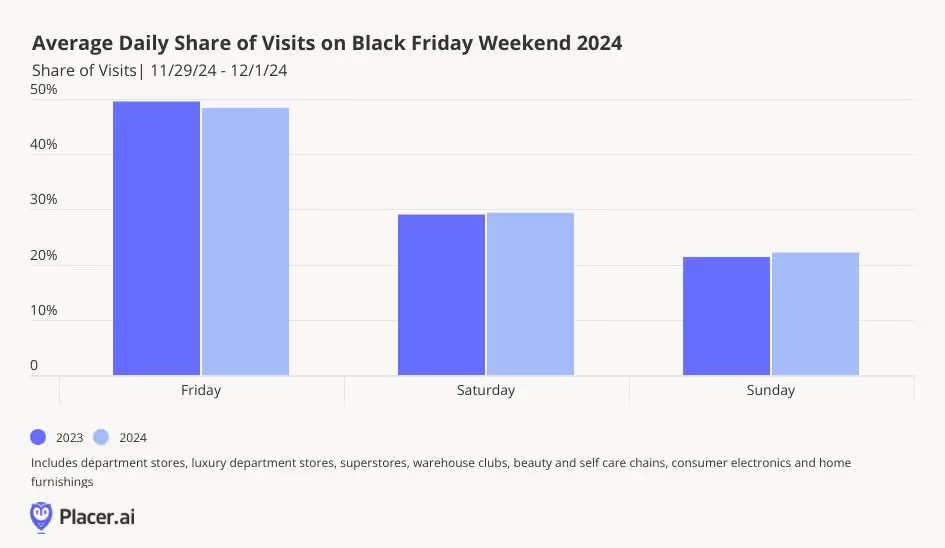

Placer’s traffic estimates revealed that while most categories experienced an increase in weekend traffic, there was a noticeable shift in the distribution of visits across the days compared to last year. This year, Friday accounted for a smaller share of event visits than in 2023, while Sunday saw a higher percentage of traffic. Despite this shift, Friday still represented nearly 50% of event visits on average across retail sectors. It’s possible that consumers delayed their shopping trips until later in the weekend, potentially after conducting online research on Friday and Saturday.

What about the iconic lines outside retailers—did they make a comeback? Our data indicates that a few specific items drove consumers to camp out and arrive early for store openings on Black Friday. Notably, Target's exclusive release of the Taylor Swift Eras Tour book and a vinyl edition of her latest album, The Tortured Poets Department, attracted early crowds. Hourly visit data shows a higher share of visits between 4 AM and 6 AM compared to 2023. While last year saw a greater share of visits during regular store hours, this year shoppers arrived earlier, likely drawn by these exclusive products.

What does Black Friday weekend reveal about the rest of the holiday season? The industry successfully overcame its first hurdle—boosting overall holiday visitation despite fewer shopping days—thanks to the growth seen last weekend. However, challenges remain with more lull weeks ahead and an earlier Super Saturday this year. As we noted previously, a shorter season also means tighter shipping windows, which could drive increased in-store visits in the final days before Christmas. On the positive side, discretionary retail saw strong visitation, with key items and promotions effectively capturing the holiday spirit and engaging consumers during this critical period.

With Black Friday just a week away, it's the perfect time to reflect on the state of retail and what lies ahead over the next 28 days as consumers prepare for holiday gatherings, celebrations, and gift-giving. The retail industry in 2024 has been anything but consistent—some categories continue to thrive, others have struggled, and a few are clawing their way back to prominence.

This year’s holiday season is likely to follow a similar pattern, but the key differentiator is time. As we highlighted in our TL;DR newsletter on LinkedIn this week, the 2024 holiday shopping period has five fewer days compared to last year, reminiscent of the 2019 vs. 2018 holiday timeline. Holiday shopping kicked off earlier this year, with department stores seeing increased activity in October. With a condensed holiday window, it’s now up to retailers to drive more frequent visits and encourage consumers to linger longer in their stores.

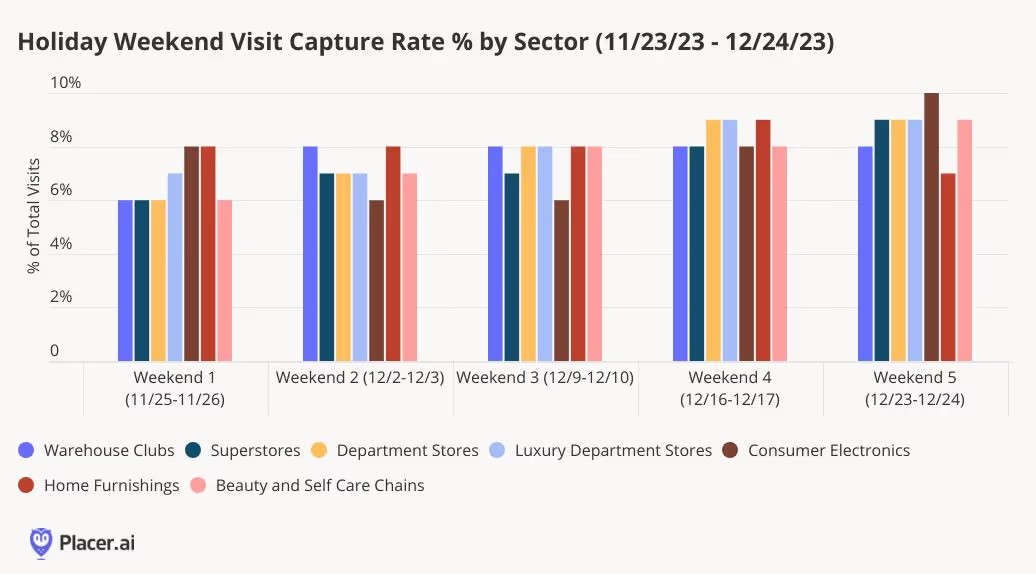

Analyzing daily visits during last year’s holiday season, there were five weekends compared to four this year. Across key holiday gifting retail categories in 2023, those five weekends (Saturday and Sunday combined) accounted for 39% of total holiday season visits, defined as Thanksgiving Day through Christmas Eve. Individually, each weekend contributed between 7% and 9% of total sector visitation, with the last two weekends each capturing 9%. In 2024, each weekend would need to account for approximately 10% of total holiday season visits to match last year’s pace.

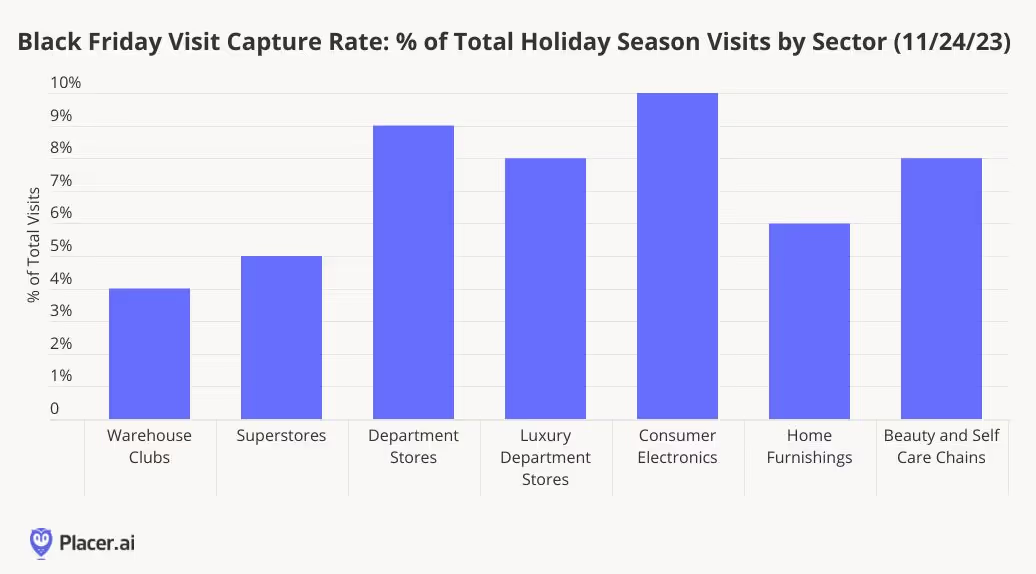

One advantage of having fewer weekends between Thanksgiving and Christmas is the reduction in lull periods, which are traditionally challenging for retailers trying to attract visitors. This year, two of the four weekends include Black Friday weekend and Super Saturday. In 2023, Black Friday alone accounted for 7% of total holiday visitation across the analyzed sectors, meaning a strong Black Friday could help offset the impact of having fewer weekends. By sector, Black Friday holds particular importance for department stores and consumer electronics retailers, as they typically see a higher share of visits on that day compared to other categories.

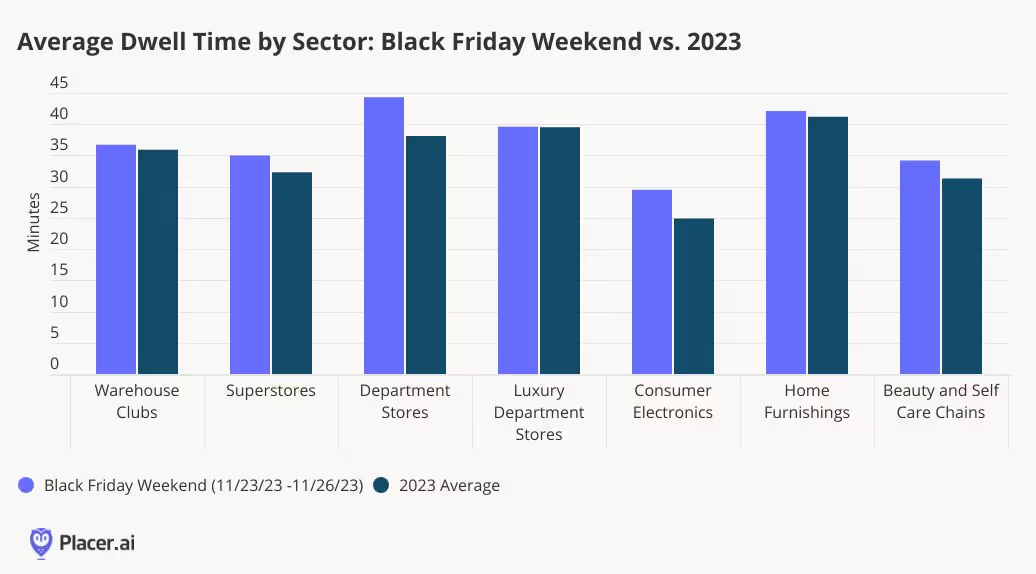

Another way to offset the five fewer shopping days? Increasing the time consumers spend in stores. In 2023, dwell times during Black Friday weekend (Thursday–Sunday) were, on average, three minutes longer than the full-year average across the analyzed sectors. Department stores had the largest gap, with visitors staying six minutes longer than average on Black Friday, followed by consumer electronics, superstores, and beauty retailers. These sectors are among the most popular for holiday shoppers during Black Friday weekend, making it encouraging that visitors stayed longer while seeking holiday deals.

A final advantage for physical retail is that fewer shopping days mean a shorter delivery window for e-commerce. With less time to shop, the holidays could sneak up on consumers, potentially driving more visitors into stores this year. While this is purely speculative, our enthusiasm for physical retail at Placer compels us to make at least one bold prediction!

The festive season is upon us, making it the perfect time to focus on a retail category that truly shines in Q4 2024: gifting, books, and paper. Despite the digital age, consumers continue to show a strong preference for shopping for these items in-store and still value tangible versions of these products. However, as discretionary retail faces challenges in meeting consumer expectations, has this category managed to capture consumer excitement and deliver delight amidst competing distractions and purchase priorities?

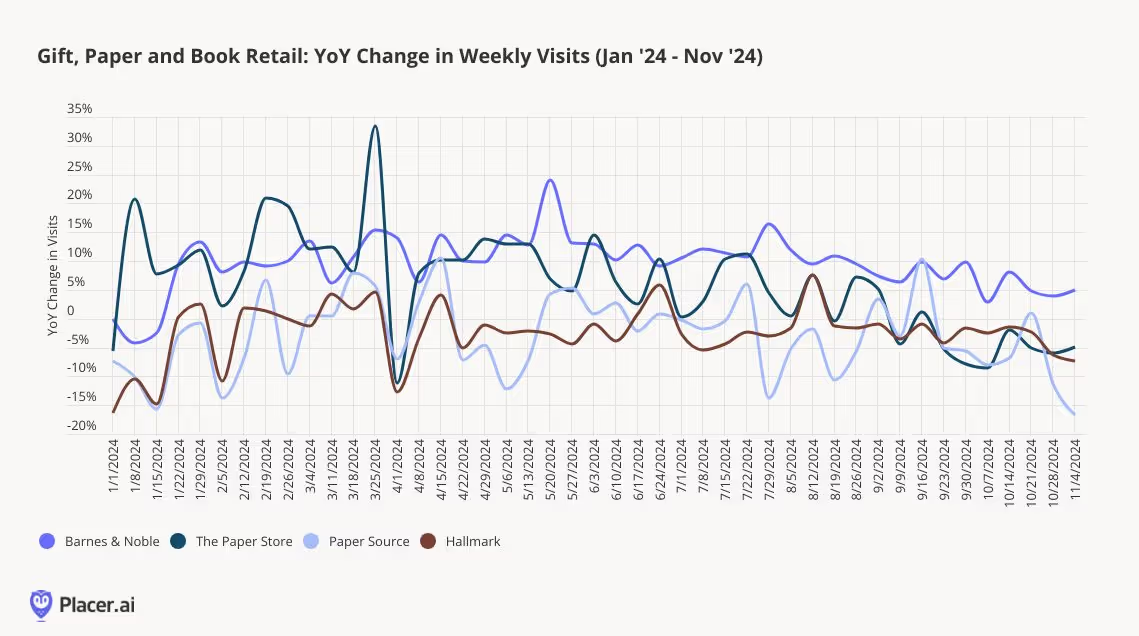

The book, paper, and gift market has experienced mixed performance among retailers this year, but even those facing year-over-year traffic declines have opportunities to improve. Barnes & Noble continues to set the standard, particularly in a category that was among the first to face e-commerce disruption; compared to 2019, visits are up 7% in 2024 despite a smaller store footprint. Paper Source is down 2% year-over-year in visits but is maintaining trends consistent with 2023. Similarly, Hallmark stores have seen a 2% decline in traffic year-to-date, though this aligns with a 5% reduction in store count. Notably, The Paper Store, a Northeastern chain of Hallmark Gold Crown stores, has outperformed the broader Hallmark brand by positioning itself more as a gift-first retailer, with cards and stationery playing a secondary role.

The book, paper, and gift market has experienced mixed performance among retailers this year, but even those facing year-over-year traffic declines have opportunities to improve. Barnes & Noble continues to set the standard, particularly in a category that was among the first to face e-commerce disruption; compared to 2019, visits are up 7% in 2024 despite a smaller store footprint. Paper Source is down 2% year-over-year in visits but is maintaining trends consistent with 2023. Similarly, Hallmark stores have seen a 2% decline in traffic year-to-date, though this aligns with a 5% reduction in store count. Notably, The Paper Store, a Northeastern chain of Hallmark Gold Crown stores, has outperformed the broader Hallmark brand by positioning itself more as a gift-first retailer, with cards and stationery playing a secondary role.

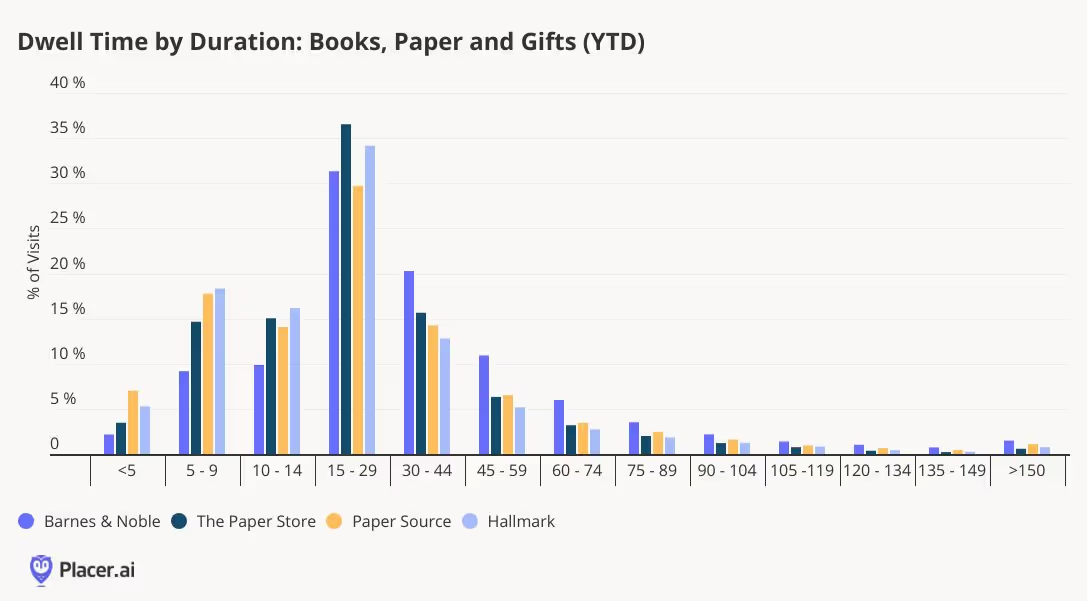

Barnes & Noble's consistent and sustainable traffic growth can be attributed to several successful initiatives. The retailer has expanded its product categories, doubled down on gifting, strengthened its position as a third space, and tapped into consumers' enduring love for books—all of which have set it apart in a challenging discretionary retail landscape. The effectiveness of these efforts is reflected in the chain's dwell time, which averages 37 minutes—nearly 10 minutes longer than any of the other chains reviewed—and excels at keeping visitors in-store for over 30 minutes.

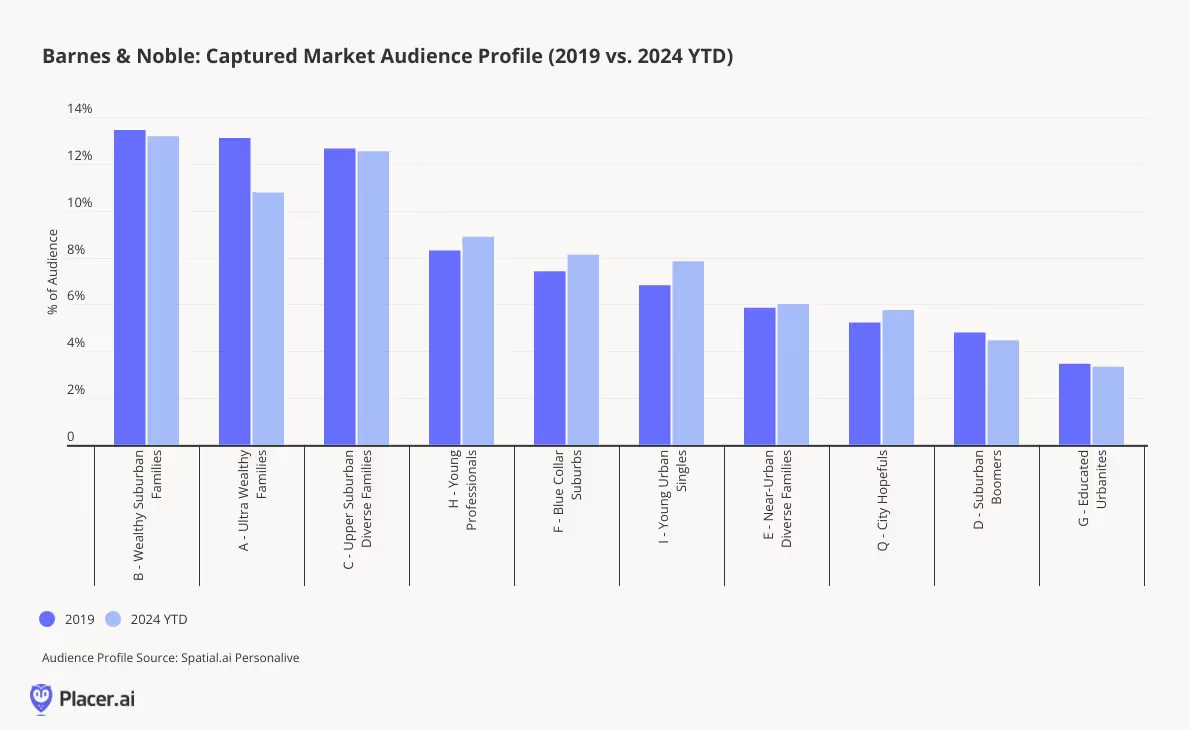

Barnes & Noble has done an impressive job of evolving its visitor demographics over time, particularly in the face of the digital revolution and the disruption of the book category. The success of specialty retailers often reflects broader cultural movements and shifts in consumer preferences, and Barnes & Noble is no exception. According to PersonaLive customer segments, the chain has significantly increased its penetration of younger consumer segments, such as Young Professionals and Young Urban Singles, when comparing 2024 year-to-date with 2019. Factors contributing to this trend could include the rise of book club culture among younger cohorts, the appeal of working from the in-store café, and an expanded assortment of gifts and paper products for special occasions.

This focus on younger consumers seems to be paying off. In 2024, 6% of Barnes & Noble visitors also shopped at a Hallmark location, although only 1% visited Paper Source, its sister brand. The integration of Paper Source shop-in-shops within Barnes & Noble locations may be cannibalizing cross-visitation between the two standalone chains.

As for Paper Source, it shares many of the elements driving Barnes & Noble's success but faces challenges in fully unlocking its potential. One key differentiator is its invitation business, but as consumers increasingly turn to digital platforms like Facebook or Paperless Post for invitations, even the booming wedding market hasn’t been enough to significantly drive growth.

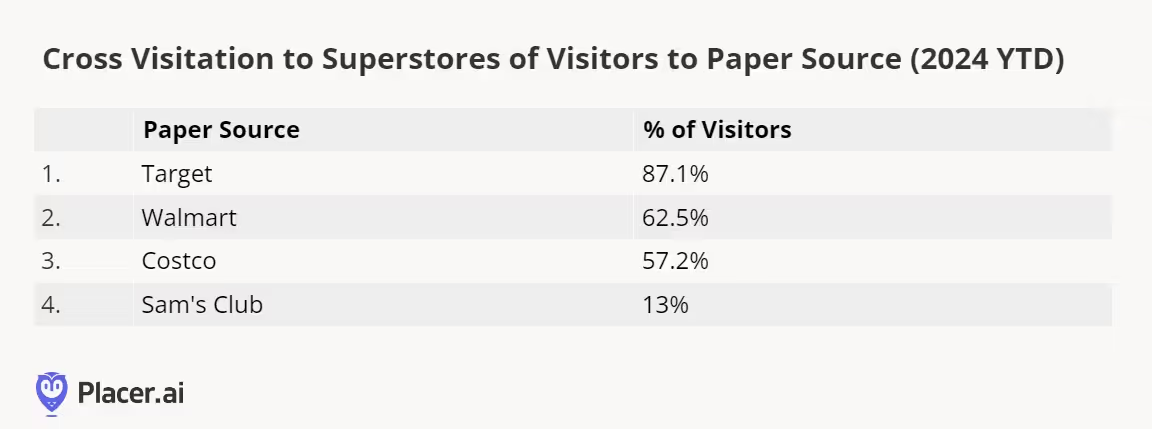

A significant challenge for Paper Source comes from competition within the superstore category. This year, 87% of Paper Source visitors also shopped at Target, and 63% visited Walmart. Both retailers have invested heavily in expanding their party supplies, cards, and gifting assortments, making it more convenient for shoppers to purchase these items during a single trip, rather than visiting a separate specialty store.

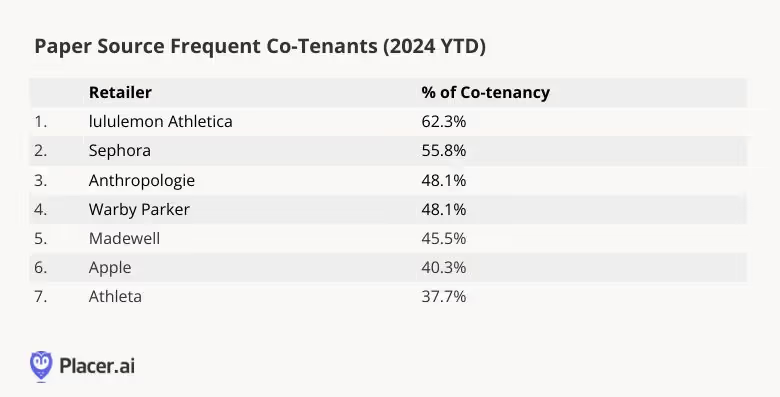

Paper Source has a strong demographic foundation to build upon as it works toward stabilization. According to PersonaLive, the chain significantly outperforms Barnes & Noble in visitation percentages among Ultra Wealthy Families, Young Professionals, and Educated Urbanites, with Ultra Wealthy Families accounting for nearly a quarter of its visitors. Its frequent co-tenants reflect similar socio-economic patterns, aligning with successful specialty chains that appeal to wealthier shoppers, such as lululemon, Sephora, Anthropologie, Warby Parker, Madewell, and Apple. With these favorable dynamics in place, Paper Source has an opportunity to thrive—success may depend on effective messaging and marketing to this affluent customer base.

The differences between Hallmark stores and The Paper Store highlight contrasting strategies: one chain has successfully expanded its product offerings to capture a more engaged audience, while the other remains closely tied to the traditional paper category and has struggled to do the same. There is little overlap in visitation between the two chains, suggesting that consumers may perceive The Paper Store as entirely separate from Hallmark, despite its status as a Gold Crown retailer.

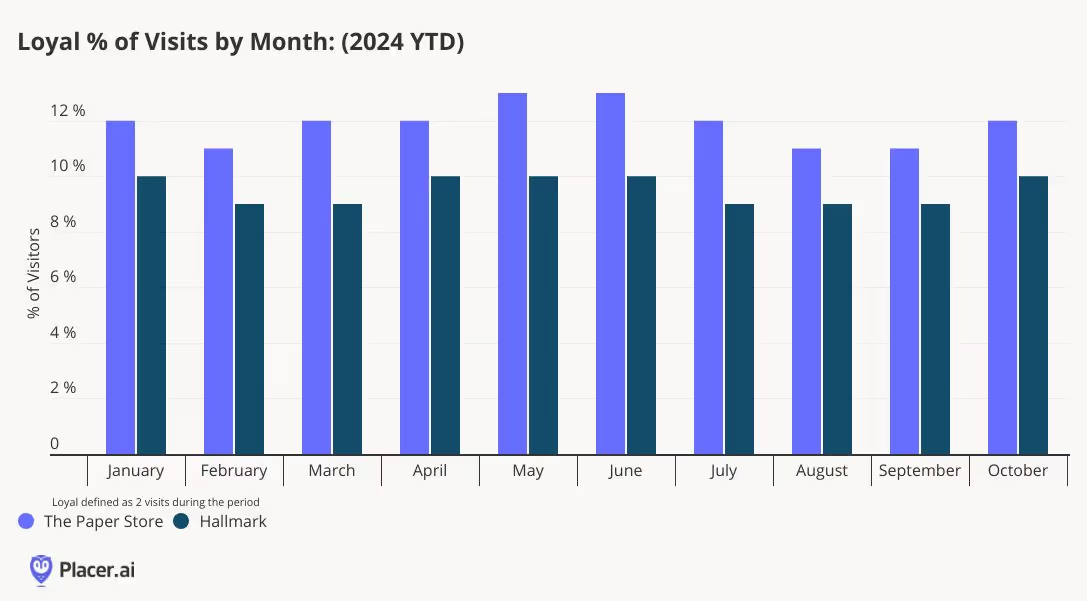

The Paper Store’s elevated and expanded assortment has fostered stronger loyalty among its visitors compared to the Hallmark chain. In 2024, loyal visitors—defined as those visiting twice per month—accounted for 12% of The Paper Store’s visitors, 2 percentage points higher than Hallmark. Additionally, The Paper Store serves more as a destination, with 37% of visitors heading home afterward, also 2 points higher than Hallmark. By expanding its product categories and curating localized selections, The Paper Store has successfully differentiated itself from the traditional Hallmark model, a strategy that could benefit the national chain as well.

The gifting, book, and paper retail category demonstrates varied consumer behavior across chains. The success of Barnes & Noble and The Paper Store underscores the importance of expanding product assortments to attract visits, as consumers increasingly seek convenience by consolidating their purchases in fewer trips. While consumers may tolerate more frequent visits for essential retail, in specialty retail, convenience and variety are critical. The category’s overall resilience suggests that consumers still have discretionary spending power for the right products at the right time, offering hope for retailers still refining their approach.

Introduction

2024 has been another challenging year for retailers. Still-high prices and an uncertain economic climate led many shoppers to trade down and cut back on unnecessary indulgences. Value took center stage, as cautious consumers sought to stretch their dollars as far as possible.

But price wasn’t the only factor driving consumer behavior in 2024. This past year saw the rise of a variety of retail and dining trends, some seemingly at odds with one another. Shoppers curbed discretionary spending, but made room in their budgets for “essential non-essentials” like gym memberships and other wellness offerings. Consumers placed a high premium on speed and convenience, while at the same time demonstrating a willingness to go out of their way for quality or value finds. And even amidst concern about the economy, shoppers were ready to pony up for specialty items, legacy brands, and fun experiences – as long as they didn’t break the bank.

How did these currents – likely to continue shaping the retail landscape into 2025 – impact leading brands and categories? We dove into the data to find out.

Conventional Value Reaching Its Ceiling

Bifurcation has emerged as a foundational principle in retail over the past few years: Consumers are increasingly gravitating toward either luxury or value offerings and away from the ‘middle.’ Add extended economic uncertainty along with rapid expansions and product diversification from top value-oriented retailers, and you have an explosion of visits in the value lane.

But we are seeing a ceiling to that growth – especially in the discount & dollar store space. Throughout 2023 and the first part of 2024, visits to discount & dollar stores increased steadily. But no category can sustain uninterrupted visit growth forever. Since April 2024, year–over-year (YoY) foot traffic to the segment has begun to slow, with September 2024 showing just a modest 0.8% YoY visit increase.

Discount & dollar stores, which attract lower-income shoppers compared to both grocery stores and superstores, have also begun lagging behind these segments in visit-per-location growth. In Q3, the average number of visits to each discount and dollar store location remained essentially flat compared to 2023 (+0.2%), while visits per location to superstores and grocery stores grew by 2.8% and 1.0%, respectively. As 2024 draws to a close, it is the latter segments, which appeal to shoppers with incomes closer to the nationwide median of $76.1K, which are seeing better YoY performance.

The deceleration doesn’t mean that discount retailers are facing existential risk – discount & dollar stores are still extremely strong and well-positioned with focused offerings that resonate with consumers. The visitation data does suggest, however, that future growth may need to focus on initiatives other large-scale fleet expansions. Some of these efforts will involve moving upmarket (see pOpShelf), some will focus on fleet optimization, and others may include new offerings and channels.

Return of the middle anyone?

Innovative and Disruptive Value Shake Up Retail and Dining

Still, in an environment where consumers have been facing the compounded effects of rising prices, value remains paramount for many shoppers. And brands that have found ways to let customers have their cake and eat it too – enjoy specialty offerings and elevated experiences without breaking the bank – have emerged as major visit winners this year.

Trader Joe’s Drives Visits With Private Label Innovation

Trader Joe’s, in particular, has stood out as one of the leading retail brands for innovative value in 2024, a trend that is expected to continue into 2025.

Trader Joe’s dedicated fan base is positively addicted to the chain’s broad range of high-quality specialty items. But by maintaining a much higher private label mix than most grocers – approximately 80%, compared to an industry average of 25% to 30% – the retailer is also able to keep its pricing competitive. Trader Joe’s cultivates consumer excitement by constantly innovating its product line – there are even websites dedicated to showcasing the chain’s new offerings each season. In turn, Trader Joe’s enjoys much higher visits per square foot than the rest of the grocery category: Over the past twelve months, Trader Joe’s drew a median 56 visits per square foot – compared to 23 for H-E-B, the second-strongest performer.

Chili’s Beats QSR at its Own Game

Casual dining chain Chili’s has also been a standout on the disruptive value front this past year – offering consumers a full-service dining experience at a quick-service price point.

Chili’s launched its Big Smasher Burger on April 29th, 2024, adding the item to its popular ‘3 for Me’ offering, which includes an appetizer, entrée, and drink for just $10.99 – lower than than the average ticket at many quick-service restaurant chains. The innovative promotion, which has been further expanded since, continues to drive impressive visitation trends. With food-away-from-home inflation continuing to decelerate, this strategy of offering deep discounts is likely to continue to be a key story in 2025.

The Convenience Myth

Convenience is king, right?

Well, probably not. If convenience truly were king, visitors would orient themselves to making fewer, longer visits to retailers – to minimize the inconvenience of frequent grocery trips and spend less time on the road. But analyzing the data suggests that, while consumers may want to save time, it is not always their chief concern.

Looking at the superstore and grocery segments (among others) reveals that the proportion of visitors spending under 30 minutes at the grocery store is actually increasing – from 73.3% in Q3 2019 to 76.6% in Q3 2024. This indicates that shoppers are increasingly willing to make shorter trips to the store to pick up just a few items.

At the same time, more consumers than ever are willing to travel farther to visit specialty grocery chains in the search of specific products that make the visit worthwhile.

Cross visitation between chains is also increasing – suggesting that shoppers are willing to make multiple trips to find the products they want – at the right price point. Between Q3 2023 and Q3 2024, the share of traditional grocery store visitors who also visited a Costco at least three times during the quarter grew across chains.

Does this mean convenience doesn’t matter? Of course not. Does it indicate that value, quality and a love of specific products are becoming just as, if not more, important to shoppers? Yes.

The implications here are very significant. If consumers are willing to go out of their way for the right products at the right price points – even at the expense of convenience – then the retailers able to leverage these ‘visit drivers’ will be best positioned to grow their reach considerably. The willingness of consumers to forego convenience considerations when the incentives are right also reinforces the ever-growing importance of the in-store experience.

So while convenience may still be within the royal family, the role of king is up for grabs.

Serving Diners Quicker With Automatization

Chipotle Draws Crowds With Autocado

Convenience may not be everything, but the drive for quicker service has emerged as more important than ever in the restaurant space. Diners want their fast food… well, as fast as possible. And to meet this demand, quick-service restaurants (QSRs) and fast-casual chains have been integrating more technology into their operations. Chipotle has been a leader in this regard, unveiling the “Autocado” robot at a Huntington Beach, California location last month. The robot can peel, pit, and chop avocados in record time, a major benefit for the Tex-Mex chain.

And the Autocado seems to be paying off. The Huntington Beach location drew 10.0% more visits compared to the average Chipotle location in the Los Angeles-Long Beach-Anaheim metro area in Q3 2024. Visitors are visiting more frequently and getting their food more quickly – 43.9% of visits at this location lasted 10 minutes or less, compared to 37.5% at other stores in the CBSA.

Are diners flocking to this Chipotle location to watch the future of avocado chopping in action, or are they enticed by shorter wait times? Time will tell. But with workers able to focus on other aspects of food preparation and customer service, the innovation appears to be resonating with diners.

McDonald’s Leans into Automation in Texas

McDonald’s, too, has leaned into new technologies to streamline its service. The chain debuted its first (almost) fully automated, takeaway-only restaurant in White Settlement, TX in 2022 – where orders are placed at kiosks or on app, and then delivered to customers by robots. (The food is still prepared by humans.) Unsurprisingly, the restaurant drives faster visits than other local McDonald’s locations – in Q3 2023, 79.7% of visits to the chain lasted less than 10 minutes, compared to 68.5% for other McDonald’s in the Dallas-Fort Worth-Arlington, TX CBSA. But crucially, the automated location is also busier than other area McDonald’s, garnering 16.8% more visits in Q3 than the chain’s CBSA-wide average. And the location draws a higher share of late-night visits than other area McDonald’s – customers on the hunt for a late-night snack might be drawn to a restaurant that offers quick, interaction-free service.

Evolving Retail Formats - Finding the Right Fit

Changing store formats is another key trend shaping retail in 2024. Whether by reducing box sizes to cut costs, make stores more accessible, or serve smaller growth markets – or by going big with one-stop shops, retailers are reimagining store design. And the moves are resonating with consumers, driving visits while at the same improving efficiency.

Macy’s Draws Local Weekday Visitors With Small-Format Stores

Macy’s, Inc. is one retailer that is leading the small-format charge this year. In February 2024, Macy’s announced its “Bold New Chapter” – a turnaround plan including the downsizing of its traditional eponymous department store fleet and a pivot towards smaller-format Macy’s locations. Macy’s has also continued to expand its highly-curated, small-format Bloomie’s concept, which features a mix of established and trendy pop-up brands tailored to local preferences.

And the data shows that this shift towards small format may be helping Macy’s drive visits with more accessible and targeted offerings that consumers can enjoy as they go about their daily routines: In Q3 2024, Macy’s small-format stores drew a higher share of weekday visitors and of local customers (i.e. those coming from less than seven miles away) than Macy’s traditional stores.

Harbor Freight Tools and Ace Hardware Serve Smaller Growth Markets With Less Square Footage

Small-format stores are also making inroads in the home improvement category. The past few years have seen consumers across the U.S. migrating to smaller suburban and rural markets – and retailers like Harbor Freight Tools and Ace Hardware are harnessing their small-format advantage to accommodate these customers while keeping costs low.

Harbor Freight tools and Ace Hardware’s trade areas have a high degree of overlap with some of the highest growth markets in the U.S., many of which have populations under 200K. And while it can be difficult to justify opening a Home Depot or Lowe’s in these hubs – both chains average more than 100,000 square feet per store – Harbor Freight Tools and Ace Hardware’s smaller boxes, generally under 20,000 square feet, are a perfect fit.

This has allowed both chains to tap into the smaller markets which are attracting growing shares of the population. And so while Home Depot and Lowe’s have seen moderate visits declines on a YoY basis, Harbor Freight and Ace Hardware have seen consistent YoY visit boosts since Q1 2024 – outperforming the wider category since early 2023.

Hy-Vee Bucks the Trend by Going Big

Are smaller stores a better bet across the board? At the end of the day, the success of smaller-format stores depends largely on the category. For retail segments that have seen visit trends slow since the pandemic – home furnishings and consumer electronics, for example – smaller-format stores offer brands a more economical way to serve their customers. Retailers have also used smaller-format stores to better curate their merchandise assortments for their most loyal customers, helping to drive improved visit frequency.

That said, a handful of retailers, such as Hy-Vee, have recently bucked the trend of smaller-format stores. These large-format stores are often designed as destination locations – Hy-Vee’s larger-format locations usually offer a full suite of amenities beyond groceries, such as a food hall, eyewear kiosk, beauty department, and candy shop. Rather than focusing on smaller markets, these stores aim to attract visitors from surrounding areas.

Visit data for Hy-Vee’s large-format store in Gretna, Nebraska indicates that this location sees a higher percentage of weekend visits than other area locations – 37.7% compared to 33.1% for the chain’s Omaha CBSA average – as well as more visits lasting over 30 minutes (32.9% compared to 21.9% for the metro area as a whole). For these shoppers, large-format, one-stop shops offer a convenient – and perhaps more exciting – alternative to traditionally sized grocery stores. The success of the large-format stores is another sign that though convenience isn’t everything in 2024, it certainly resonates – especially when paired with added-value offerings.

A Resurgence of Legacy Brands

Many retail brands have entrenched themselves in American culture and become an extension of consumers' identities. And while some of these previously ubiquitous brands have disappeared over the years as the retail industry evolved, others have transformed to keep pace with changing consumer needs – and some have even come back from the brink of extinction. And the quest for value notwithstanding, 2024 has also seen the resurgence of many of these (decidedly non-off-price) legacy brands.

In apparel specifically, Gap and Abercrombie & Fitch – two brands that dominated the cultural zeitgeist of the 1990s and early 2000s before seeing their popularity decline somewhat in the late aughts and 2010s – may be staging a comeback. Bed Bath & Beyond, a leader in the home goods category, is also making a play at returning to physical retail through partnerships.

Anthropologie, another legacy player in women’s fashion and home goods, is also on the rise. Anthropologie’s distinctive aesthetic resonates deeply with consumers – especially women millennials aged 30 to 45. And by capturing the hearts of its customers, the retailer stands as a beacon for retailers that can hedge against promotional activity and still drive foot traffic growth.

And visits to the chain have been rising steadily. In Q4 2023, the chain experienced a bigger holiday season foot traffic spike than pre-pandemic, drawing more overall visits than in Q4 2019. And in Q3 2024, visits were higher than in Q3 2023.

Meeting the Evolving Needs of Millennials

And speaking of the 35 to 40 set – the generation that all retailers are courting? Millennials. Does that sound familiar? Yes, because this is the same generational cohort that retailers tried to target a decade ago. As millennials have aged into the family-formation stage of life, their retail needs have evolved, and the industry is now primed to meet them.

Sam’s Club Draws Value-Conscious Singles and Starters

From the revival of nostalgic brands like the Limited Too launch at Kohl’s to warehouse clubs expanding memberships to younger consumers as they move to suburban and rural communities, there are myriad examples of retailers reaching out to this cohort. And Sam’s Club offers a prime example of this trend.

Over the past few years, millennials and Gen-Zers have emerged as major drivers of membership growth at Sam’s Club, drawn to the retailer’s value offerings and digital upgrades – like the club’s Scan & Go technology. Over the same period, Sam’s Club has grown the share of “Singles and Starters” households in its captured market from 6% above the national benchmark in Q3 2019 to 15% in Q3 2024. And with plans to involve customers in co-creating products for its private-label brand, Sam’s Club may continue to grow its market share among this value-conscious – but also discerning and optimistic – demographic.

Taco Bell Brings in Crowds With Value Nostalgia Menu

Millennials are also now old enough to wax nostalgic about their youth – and brands are paying attention. This summer, Taco Bell leaned into nostalgia with a promotion bringing back iconic menu items from the 60s, 70s, 80s, and 90s – all priced under $3. The promotion, which soft-launched at three Southern California locations in August, was so successful that the company is now offering the specials nationwide. The three locations that trialed the “Decades Menu” saw significant boosts in visits during the promotional period compared to their daily averages for August. And people came from far and wide to sample the offerings – with a higher proportion of visitors traveling over seven miles to reach the stores while the items were available.

What Lies Ahead?

Hot on the heels of a tumultuous 2023, 2024’s retail environment has certainly kept retailers on their toes. While embracing innovative value has helped some chains thrive, other previously ascendant value segments, including discount & dollar stores, may have reached their growth ceilings. Consumers clearly care about convenience – but are willing to make multiple grocery stops to find what they need. At the same time, legacy brands are plotting their comeback, while others are harnessing the power of nostalgia to drive millennials – and other consumers – through their doors.