.svg)

As essential sectors of retail face a slowdown in traffic momentum, the need for unique offerings and competitive advantages is more pressing than ever. Grocery retailers have benefited from increased visits, which has kept consumers engaged with chains and their offerings, even if it hasn’t always translated into larger basket sizes. In an increasingly competitive grocery market, retailers will need to consistently prove to consumers that they’re worth the extra visit.

Specialty grocers are better positioned to meet this challenge as value-focused grocery options become more constrained. Many local and regional chains have the added benefit of nimble operating models, enabling them to quickly adapt to consumer preferences. Beyond that, these specialty chains have deeply embedded themselves in the communities they serve. Looking ahead to 2025 and the growing recognition of physical stores’ importance, the strong relationships between specialty grocery retailers and consumers could help them thrive in this evolving environment.

One specialty chain that stands out in this context is Stew Leonard’s. Beloved in the Tri-State area—an area known for outstanding grocery chains—Stew Leonard’s combines product expertise with a unique in-store experience, famously described by The New York Times as “the Disneyland of Dairy Stores.” Imagine a grocery store with animatronics and birthday parties! In an era when we need more joy in retail, Stew Leonard’s sets the gold standard. With just eight locations, each with a large footprint and a strong connection to its local community, Stew Leonard’s offers a compelling package. A robust private label program, specialty departments, and high service levels make this chain stand out without relying on promotions or low prices.

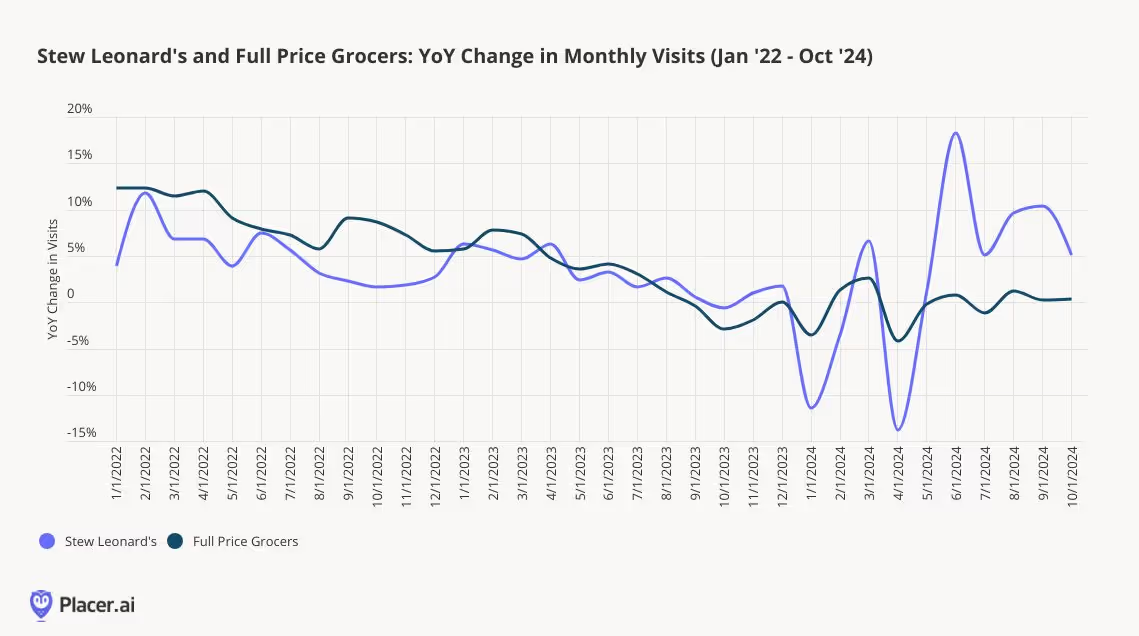

According to Placer’s foot traffic estimates, Stew Leonard’s has effectively hedged against the slowdown in growth seen by other full-price grocery chains this year. Year-to-date, the chain has experienced a 3% year-over-year increase, compared to flat growth for full-price chains. Examining trends over time, Stew Leonard’s has shown consistent, sustainable growth throughout 2022 and 2023, with an acceleration in visits in the latter half of this year, driven by the opening of its new store in Clifton, NJ.

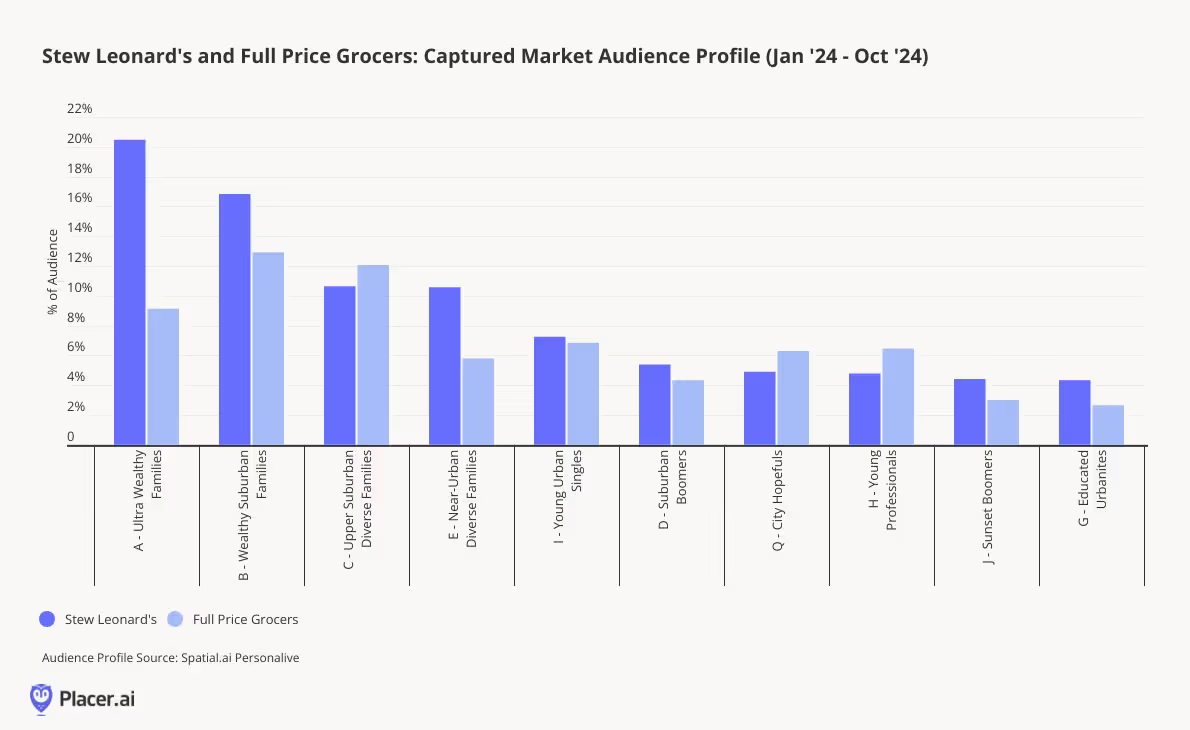

One reason for Stew Leonard’s success is the elasticity of its consumer base. Operating in the Tri-State area allows the chain to tap into wealthier consumer segments compared to national chains. According to PersonaLive audience segmentation, Stew Leonard’s has more than double the concentration of Ultra Wealthy Families compared to full-price grocery chains, along with a high percentage of Wealthy Suburban Families. The chain also attracts a notable share of Young Urban Singles, likely drawn by its strong offerings in prepared and specialty foods.

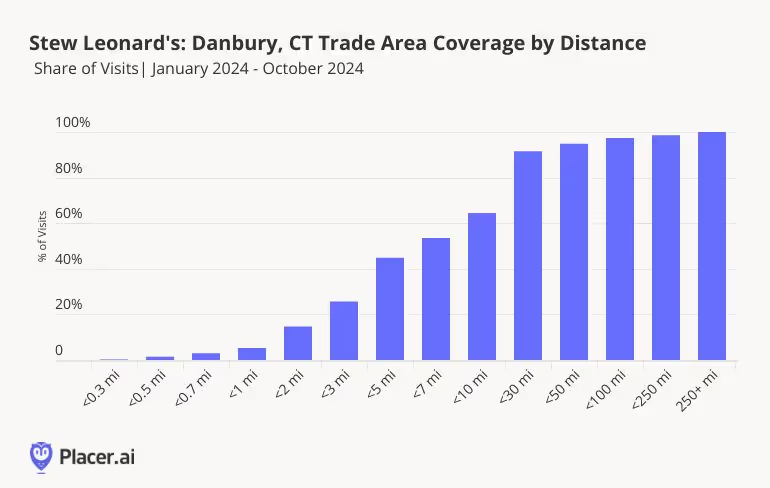

Stew Leonard’s Danbury, CT location offers insight into the brand’s appeal to shoppers. According to Placer’s trade area metrics, 35% of visitors to this store travel from more than 10 miles away, and nearly 10% come from over 30 miles, with clusters of visits from across the Northeastern corridor.

Store-level metrics also reveal strong loyalty among Stew Leonard’s visitors. Year-to-date in 2024, over a quarter of visitors to the Danbury location visited at least four times, and 35% visited three or more times. At the same time, there is a substantial share of visitors who appear to make special, less frequent trips to the store. These visitors show high cross-visitation rates with other grocers, such as Costco and ShopRite, as well as with Stew Leonard’s own operated Wine and Spirits locations.

Stew Leonard’s exemplifies a retailer that resonates with local consumers while offering an experience that attracts visitors from further away. Its combination of unique experiences, services, and products creates a shopping experience that goes well beyond traditional retail. Even as visits slow down across the sector, specialty grocers that remain hyper-focused on their unique offerings are likely to continue drawing in customers.

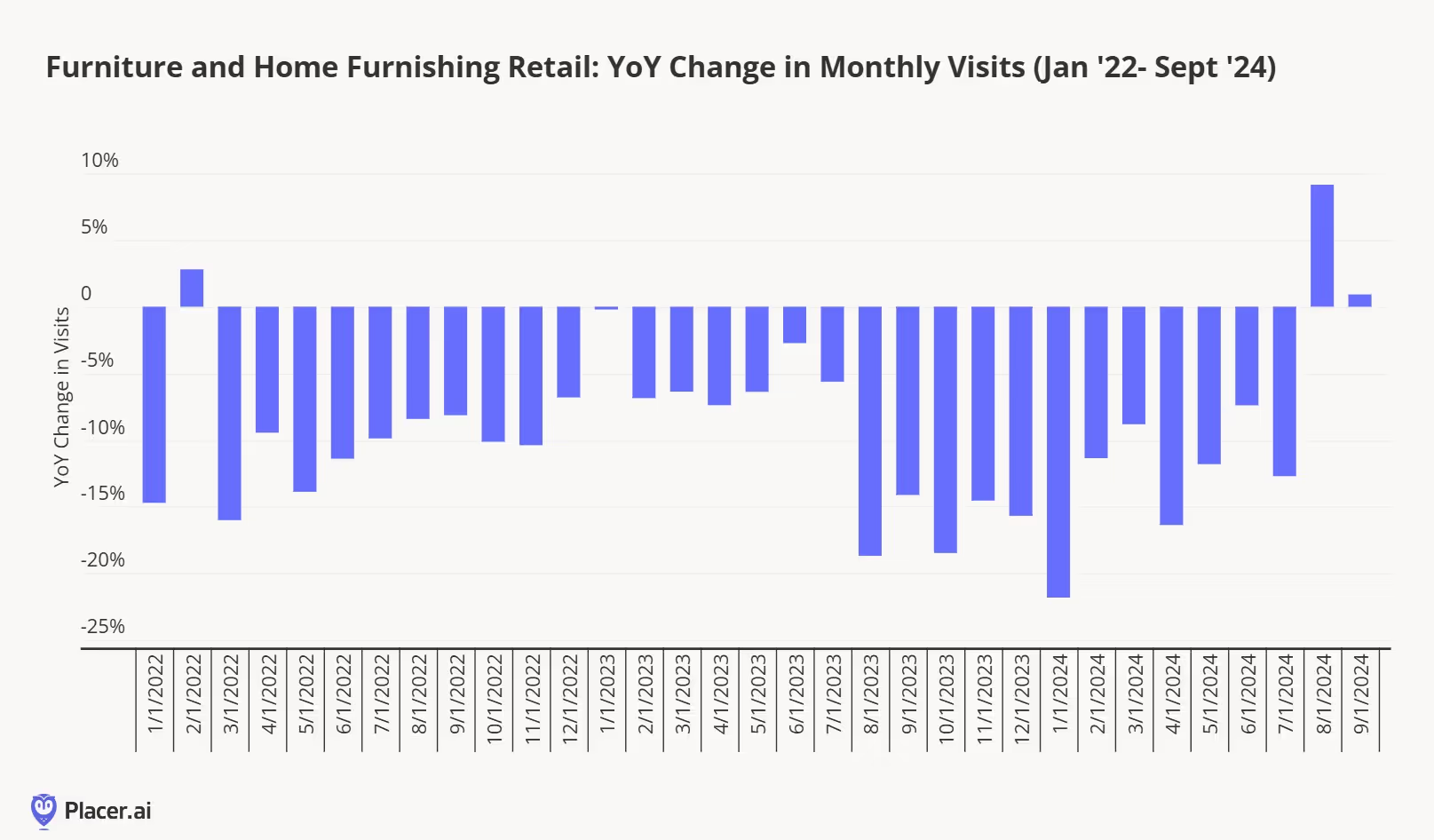

Over the past two weeks, the home industry has been abuzz with news from the remnants of Bed Bath & Beyond. A retailer that stood as the leader among specialty players continues to try and find new life in physical retail despite the closure of the original chain and its subsidiaries. After a year back in business, buybuy BABY, under new management, announced that it would be closing its 10 reopened locations.

Over at Beyond Inc., the new holding company for Overstock.com and the newly reformed Bed Bath & Beyond brand, they announced new partnerships with both Kirkland’s and The Container Store. The former partnership is going to help bring the brand back to physical retail with the creation of five Bed Bath & Beyond “neighborhood” small format stores, with locations to be announced; stores will be scouted, developed and operated by Kirkland’s. In the partnership with The Container Store, Beyond Inc. made a financial investment in the retailer and will allow The Container Store to leverage the brand’s assets, name, assortment and data; shop-in-shops also appear to be a part of this new partnership.

The home industry has been incredibly challenged in the post-pandemic period (below). However, as the category became further consolidated over the past few years, these new partnerships could help to revitalize all three brands, all of which have a strong brand identity with consumers. These partnerships also allow the brands to harness their strengths to benefit multiple banners.

How closely aligned are these brands? Kirkland’s tends to focus on furniture and furnishings, The Container Store handles all things organization, and the Bed Bath & Beyond brand name still carries weight as the undisputed leader in all things home.

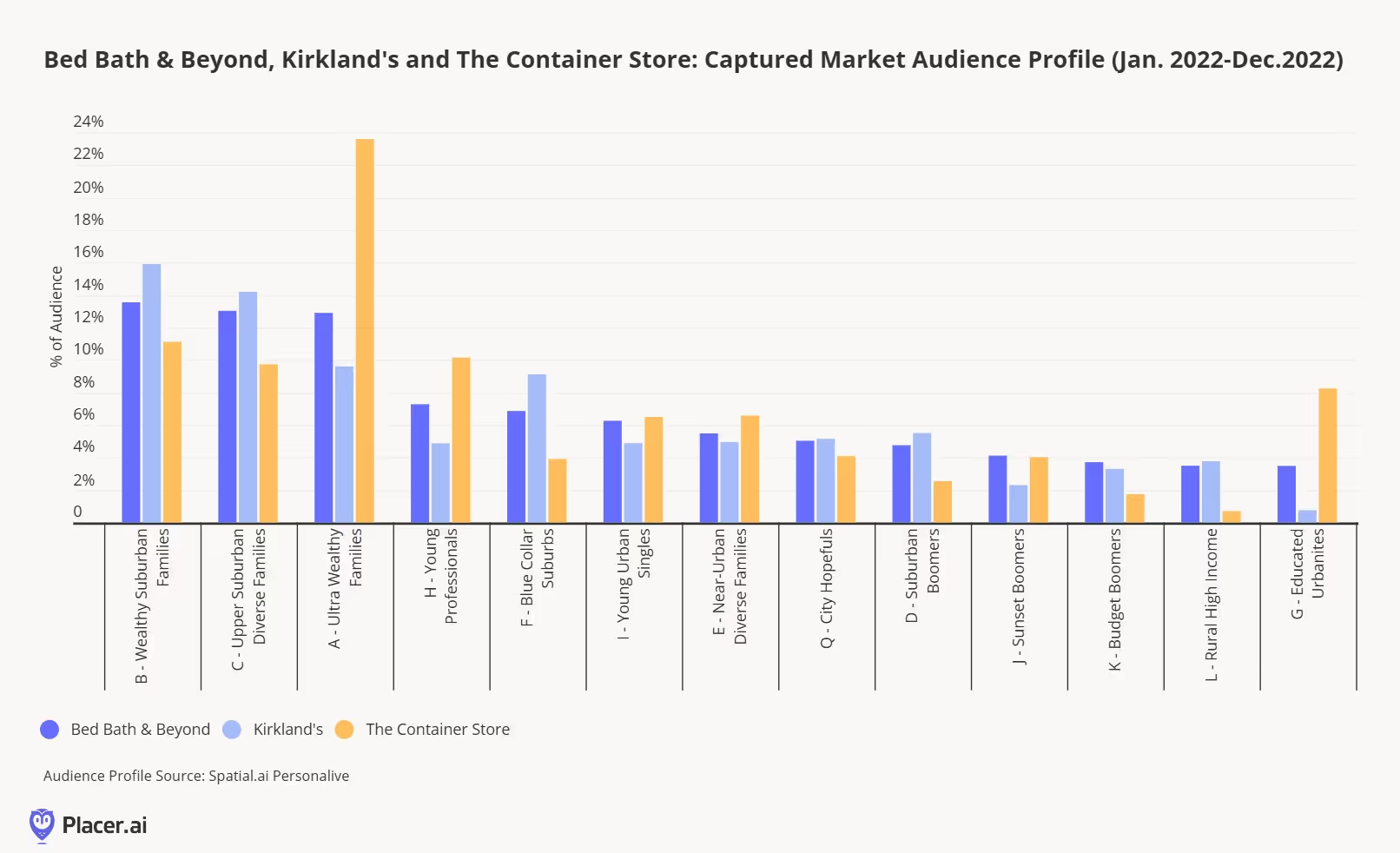

Looking at PersonaLive’s demographic and psychographic segmentation of visitors to all three brands in 2022, before Bed Bath & Beyond’s closure the next year, there are some clear alignments and also opportunities to reach new visitors through the partnerships. Kirkland outperformed Bed Bath & Beyond with suburban cohorts such as Wealthy Suburban Families, Upper Suburban Diverse Families and Blue Collar Suburbs.

Through the lens of The Container Store, it provides a lot more opportunity for Beyond Inc. to reach higher concentrations of visitors from segments such as Ultra Wealthy Families, Educated Urbanites and Young Professionals. Looking at the partnerships with both Kirkland’s and the Container Store as a collective strategy, Beyond Inc. can capitalize on the migration to suburban communities by consumers and higher income households with the new brand.

Another positive sign for the partnerships is the high levels of cross visitation between the retailers before the closing of Bed Bath & Beyond. In 2022, Bed Bath & Beyond’s final full year of operation, 20% of visitors to Kirkland’s and almost a quarter of visitors to The Container Store cross visited Bed Bath & Beyond.

In theory, both partnerships will allow Bed Bath & Beyond to return to physical retail in alignment with both consumers and the current retail landscape. Industry specific retailers and incredibly important to the health and long term success of the industry, and the idea of welcoming back a beloved brand is exciting. It should be interesting to see the new small format stores and installations as the debut and look at the impacts of the partnership on the broader home category.

The inaugural Shoptalk Fall event brought a new energy to Chicago this week. The smaller format event allowed us to dive deeper into the trends across the retail industry and hear from key retail players about their initiatives and innovations across the industry.

One thing that is clear, retailers are bullish about physical retail. Many retailers shared plans for store openings in 2025, and there is a real focus on creating the right types of store formats and finding locations that are in line with a brand’s consumers. We may truly be at a point of inflection from a channel perspective, and physical retail is likely to become a more important part of the equation.

There’s a real energy shift in the industry in regard to the importance of stores, and it’s refreshing to see. As the industry settles from the migration shifts of consumers during and after the pandemic, the opportunity for new stores to directly cater to these new groups of shoppers is immense.

And it’s not just about the rise of physical retail, but the stories that retailers are able to tell through their offline channels. Retailers are actively focused on ways to eliminate friction for shoppers, arm store employees with more insights and tools and create experiences that forge lasting bonds with shoppers. We heard from Wayfair, Build-A-Bear Workshop, Michaels and Studs, who all referenced that differentiating experiences are driving loyalty and fostering long-term connections with consumers. Stores are an essential part of building and retaining brand equity with consumers.

The other key theme centers around none other than the consumer. The retail industry feels more customer centric than ever before, especially as we get further away from the pandemic. Retailers and brands recognize that today, the shopper is in the driver’s seat, and many initiatives and innovations center around providing the consumer with more power and knowledge. This is why we are hearing more about "micro-merchandising". Retailers need and can enhance their relevancy by understanding the unique demographics/psychographic differences and preferences of their individual locations.

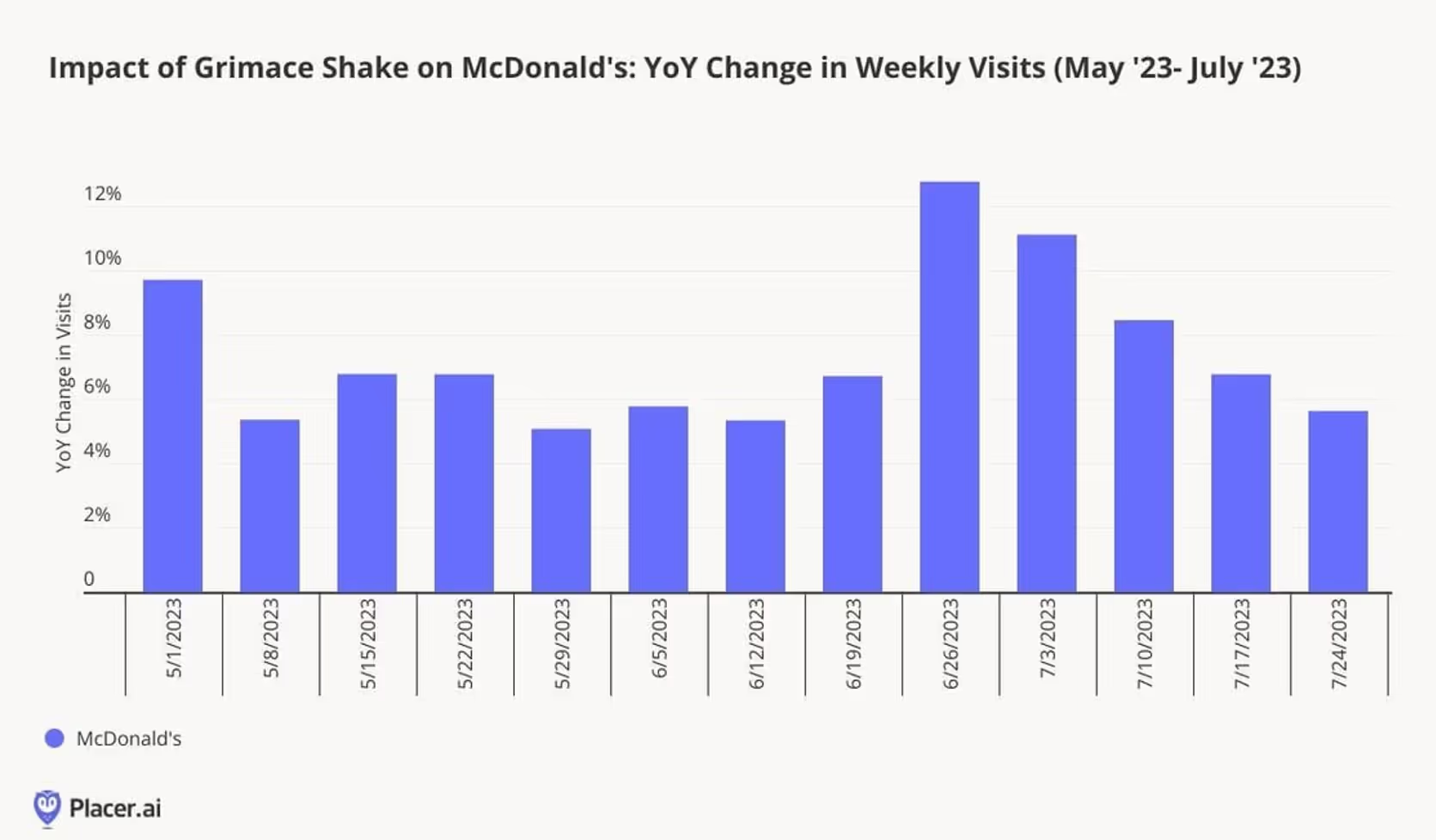

Executives at McDonald’s provided more insight into the success of June 2023's immensely popular birthday celebration for Grimace, including the Grimace Shake; they built the concept around the idea that many consumers celebrate a birthday at McDonald’s restaurants, but from there they let consumers drive the conversation around the promotion on social media.

We heard from many that word of mouth marketing is truly the key to success in retail today, and empowering consumers to share their thoughts and affinities with others in person or through social media platforms is driving engagement and adoption. Through the lens of foot traffic, we may see more consumers head to stores after hearing about them from others in their network. Marketing departments no longer consist of teams within an organization, but incorporate consumers as well.

Overall, we felt a lot of positivity from the industry about where we’re headed in the near term. As we see the slow rebound of the discretionary side of retail, new stores and innovations in the coming year and a consumer that still remains resilient despite many economic headwinds, the best might be ahead for the industry.

We’re in the midst of not only the beginning of the holiday season in retail, but also at the peak of wedding season. September and October are now the most popular months to get married, and fall weddings have become extremely popular with younger generations. Wedding planning encompasses so many different occasions, events and appointments, but none more important than wedding dress shopping.

The bridal retail space across the U.S. is incredibly fragmented, with much of the business being done by local boutiques and small chains with a handful of stores. However, there are still major retailers in the market and more entering each year. Brands in apparel have especially taken note with Abercrombie & Fitch, Reformation and e-commerce brands like Lulus all making a play at capturing a bride’s attention.

Two larger, more established forces in bridal retail include David’s Bridal and Anthropologie Weddings (formerly known as BHLDN). Both concepts have distinct value propositions for their consumers, but both aim at providing an elevated assortment and experience that is also value oriented. As value continues to be a motivating factor across all consumer decision making, both of these retailers have seen positive momentum in 2024.

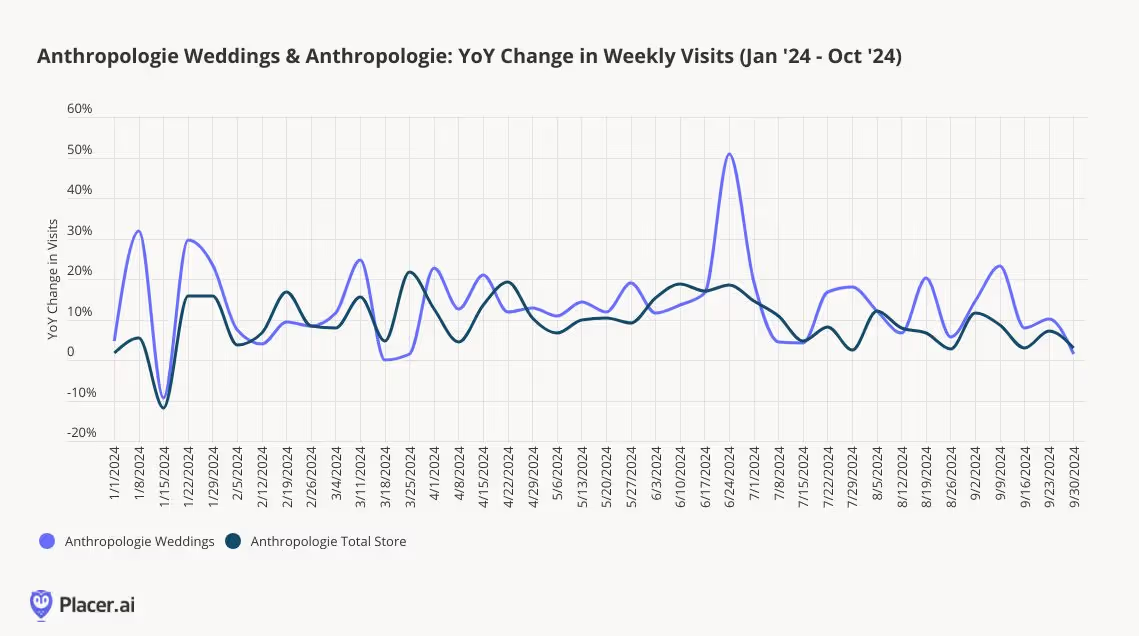

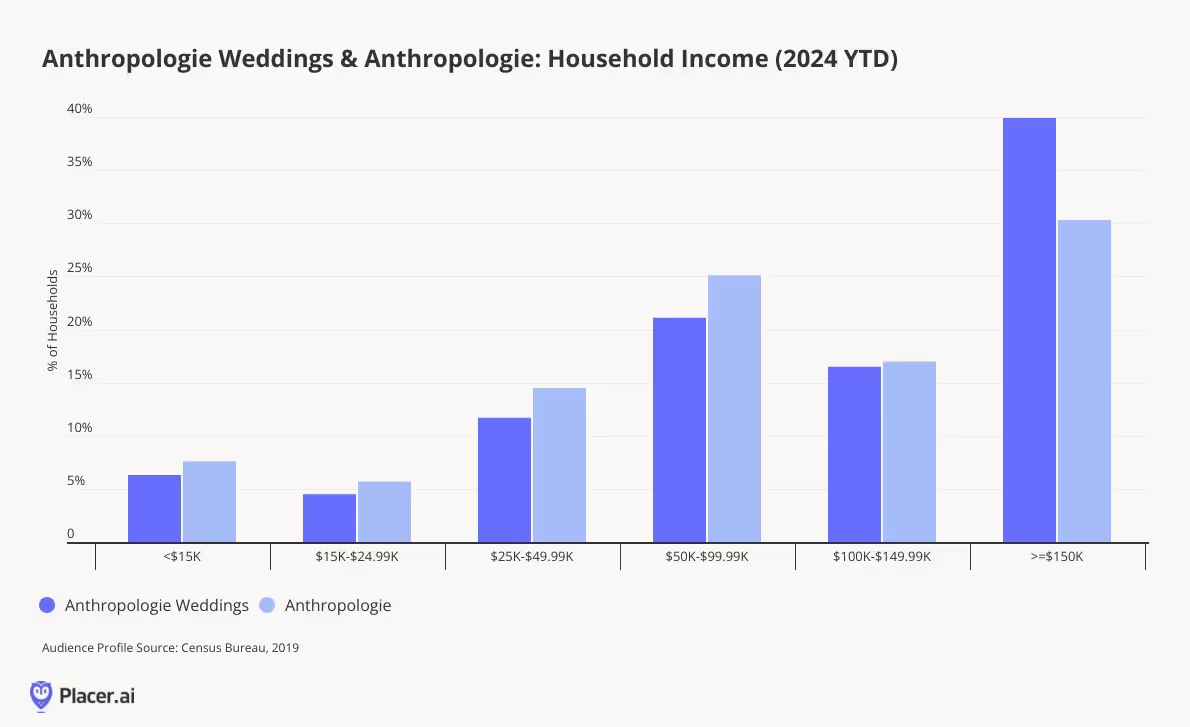

Looking at year-over-year change in visitation, Anthropologie Weddings locations have consistently seen traffic growth in 2024 and have outperformed the total chain from a visitation perspective. The wedding shop is not located in all Anthropologie stores, but the stores that do have the concept cater to a higher income and trendy consumer; the location selection of towns such as Newport Beach, Westport, CT, and Newton, MA has certainly benefited the stores.

The median household income of visits to Anthropologie weddings is $117K compared to $94K chainwide. Despite the higher income profile of visitors to the wedding focused stores, Anthropologie Weddings still does appeal to value-conscious brides, despite socioeconomic status; most bridal gowns are under $2,500, which is still relatively affordable based on the industry standard.

Looking at the audience segmentation of visitors to Anthropologie Weddings compared to the total chain using PersonaLive, the wedding shops saw almost double the share of visits from Educated Urbanites, a key segment for a bridal business to not only capture, but convert. All of this highlights the success of the brand’s wedding strategy, from its location selection, to assortment and experience, which are distinctly Anthropologie, but also fitting of a special trip. Other retailers looking to make a splash in the bridal market should certainly look to Anthropologie as a case study in brand extension.

David’s Bridal had a challenging start to 2024, mirroring a few years of challenging foot traffic to its stores. However, around the midpoint of the year, there’s been an acceleration in visitation across the chain. Looking at visitation trends for 2023 and 2024, the brand started to close the gap in August. As a true value centered bridal retailer, the brand may have found its moment in the current economic climate.

Looking at the change in visitation throughout 2024, from January to July, on average, visits were down 32% YoY; from August through the most recent week, visits were down only 2% year-over-year. That’s a great improvement in trend against the backdrop of a challenging year, and even more interesting when thinking about the lead time brides have for ordering wedding gowns; most dresses for fall weddings would have been ordered in the winter or spring months, where David’s Bridal sees higher levels of visitation.

.avif)

The audience segmentation of the brand has also shifted over that time. Compared to 2023 as a benchmark, the period of August 2024 through present has seen a higher share of visits from Suburban Boomers and Melting Pot Families, and a slight increase in Young Professionals. The brand also stocks special occasion and homecoming dresses, which both could appeal to these groups.

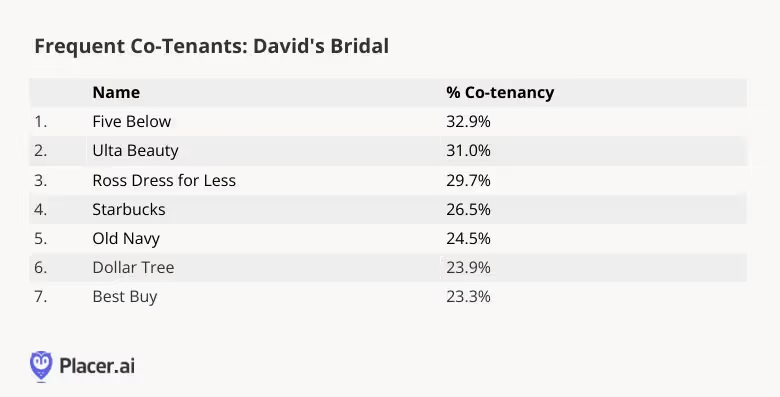

Using Placer’s Frequent Co-Tenants report, David’s Bridal locations tend to be co-located with other specialty retailers, including Five Below, Ulta Beauty, and Ross Dress for Less, who are also value oriented and the latter two retailers have been doing well in securing more traffic. The stores may have benefits from their co-location with retailers that meet current consumer desires.

Weddings continue to be a big business across the U.S., and retailers that support the wedding industry have a lot of opportunities for growth, if they can find and appeal to the right consumer cohorts. Brides of all levels are looking for an elevated experience and selection, no matter her budget.

For fashion-focused consumers, there’s never been more choices available to shop. While luxury brands and retailers are still viewed as the trend setters, there are many brands in the mid-tier luxury market gaining traction. At a time when perceived value is paramount to shopper decision-making, brands that provide a great experience and on-trend styles that won’t break a budget are winning visits.

Product knowledge, recommendations and styling tips can all be accessed in the digital and social world, which gives smaller brands a fighting chance at connecting with shoppers who may not have stores located near them. Those brands whose social presence also coincides with a physical shopping experience, they’re able to build a cult-like following.

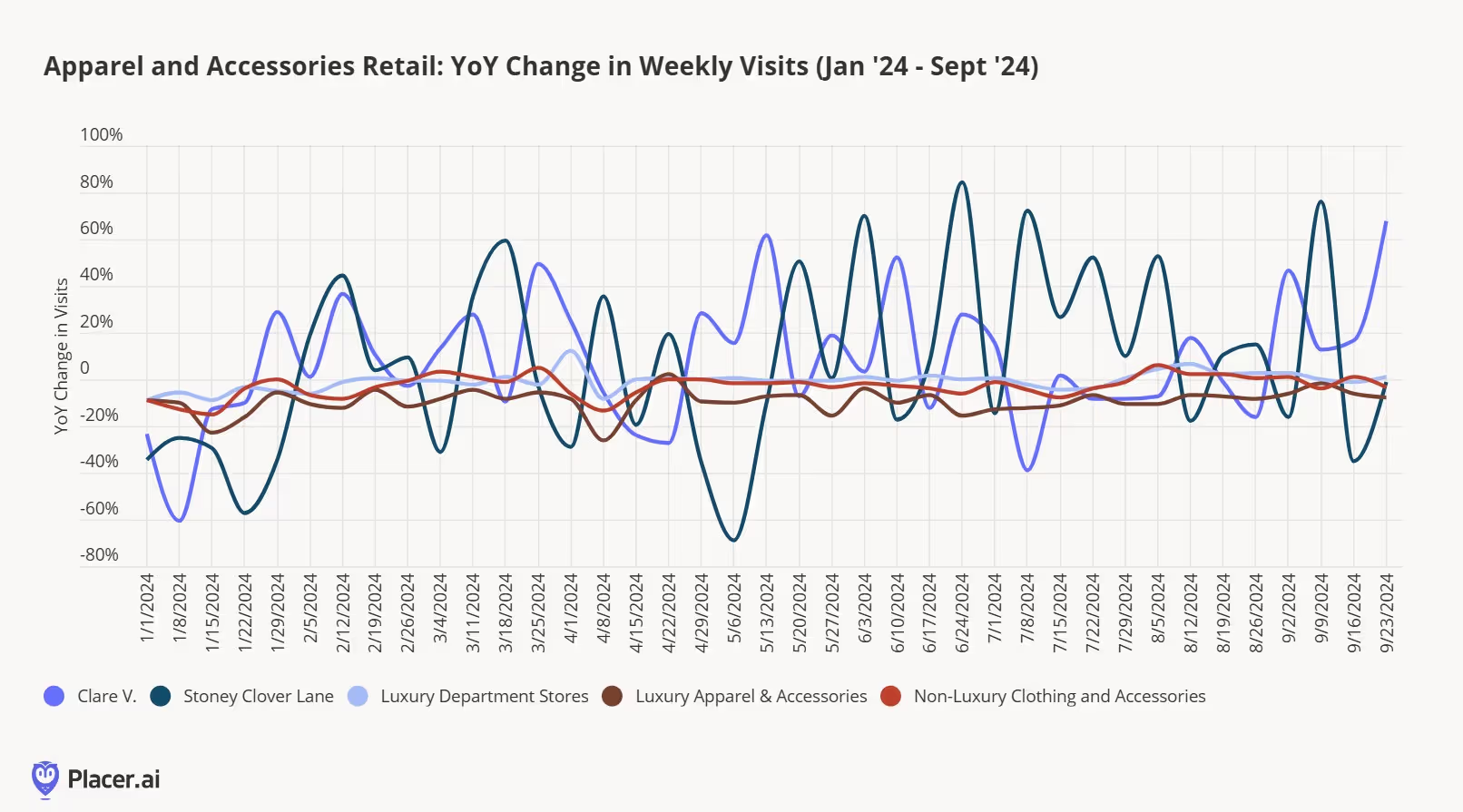

Accessories is a market that’s even further fragmented when it comes to the number of consumer choices, specifically in areas like handbags. Brands that have found their niche in the mid-tier market, like Clare V. and Stoney Clover Lane, have been able to hedge against the headwinds facing most discretionary brands. Although each brand has a handful of locations in comparison to accessory behemoths, their unique selection, brand storytelling and ability to assimilate to local environments have helped them to garner quite the following.

In comparing both brands to other apparel and accessories sectors, they have outperformed the other areas handily throughout 2024. Certainly fashion is very cyclical; one day, a brand is hot, and within a few weeks the craze might be over. However, both of these brands have been around since before the pandemic and continued to climb.

Looking further into Stoney Clover Lane, the brand is known for its colorful nylon pouches, purses and luggage that consumers can customize with a broad assortment of patches. The brand has also had licensing partnerships with brands such as American Girl and Disney.

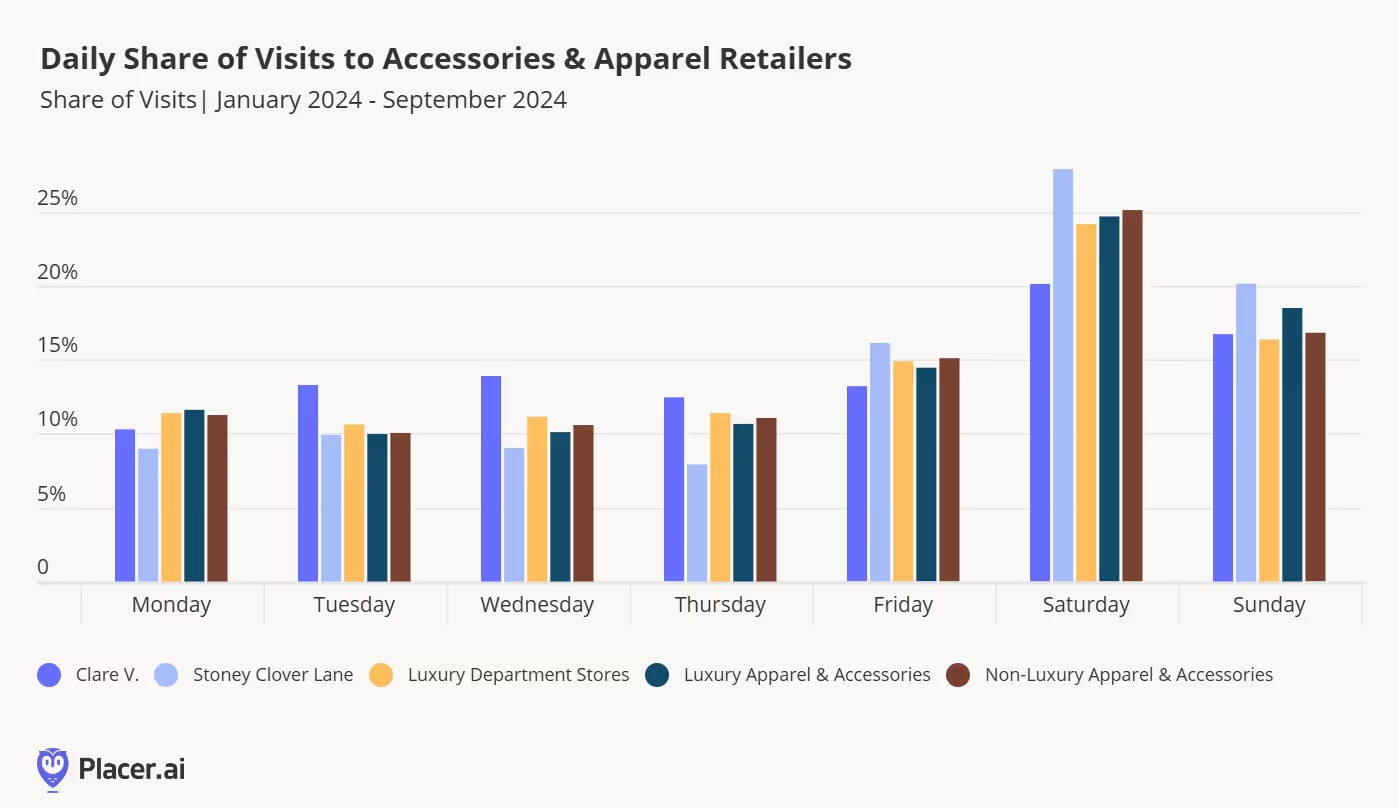

Its physical retail presence combines experiences and an expansive assortment where consumers can customize their bags in store with patches and also attend local events. The brand has the highest percentage of weekend visits compared to the competitive set, and it’s clear that it’s a destination retailer for visitors.

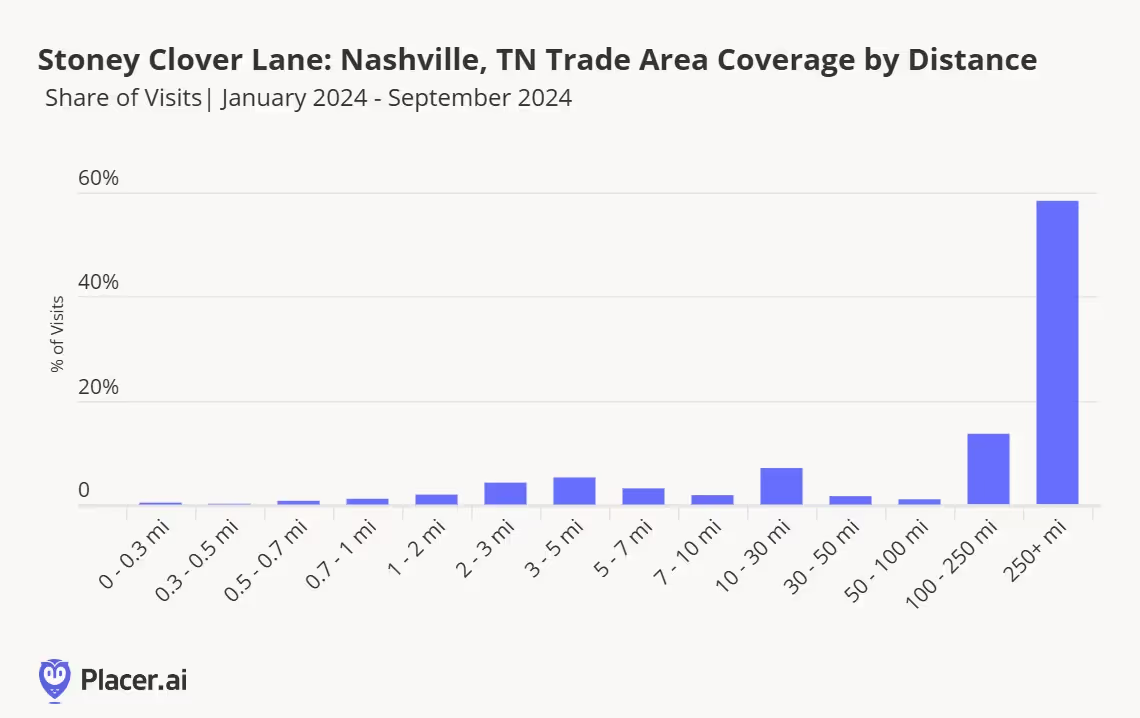

Stoney Clover Lane’s Nashville outpost, located in the popular 12 South neighborhood, offers the product customization as well as a performance stage to infuse some of the local culture into the store. Looking at the visitor journey for this location, there is a high level of cross visitation to hotels and restaurants, indicating that this store may serve as a destination for out-of-town travelers who want to shop the location. Placer’s Trade Area feature corroborates this, as there is a high concentration of visits from other Southern cities including Atlanta, Birmingham, Dallas and Miami.

Clare V. blends the iconic styles of Los Angeles and Paris into an accessories brand that feels inherently cool. Its retail locations feel like an art museum blended with your best friend’s closet and each store location incorporates the local feel of the neighborhood it inhabits, including iconic locations like the Brentwood Country Mart in Los Angeles.

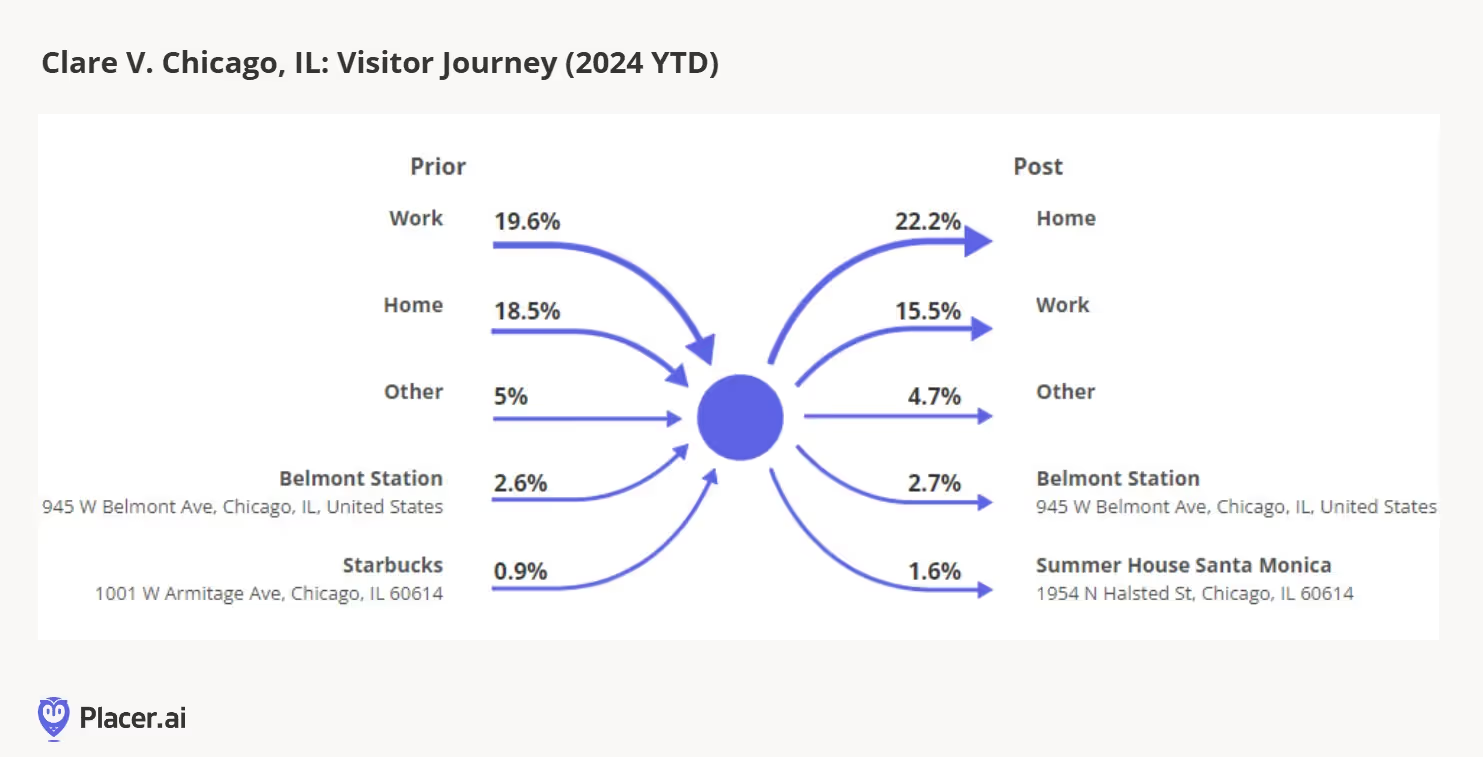

Clare V.’s Chicago shop draws a more local crowd, with a high level of cross-vistation to and from home as well as transportation services. Other neighborhood shops, restaurants and venues like Wrigley Field also have high levels of cross-visitation for visitors to Clare V.. By entrenching itself into the local look and feel of the neighborhoods it occupies, this national brand still feels like a well kept secret for those passing by. In comparing the trade area of the Chicago location in 2024 and 2023, the brand has been able to expand its reach further in Western Chicago Suburbs this year.

Retailer summer deals are in full swing, with promotional events like Amazon Prime Day and Nordstrom Anniversary Sale, Target Circle Week, and Macy’s All Star Week taking place over the past two weeks. The summer has come to signify the first large scale, cross-industry retailer push to engage with consumers and also test new promotional strategies with shoppers.

Target’s reinvigoration of its loyalty program, Target Circle, launched in April as a streamlined program with more perceived value for members and created a new paid tier called Target Circle 360. Target Circle Week, which took place between July 7-13, focused more on loyalty program members than previous iterations of the event to drive visits by loyal shoppers. The retailer promoted items across discretionary and essential categories, an effort meant to offset the challenges in the discretionary side of the business this year. Mass merchants have been especially challenged compared to warehouse clubs in the superstore category, and Circle Week, especially as the first event of the retailer's summer deals, is a barometer of what’s to come.

According to our foot traffic measurements, Target Circle Week was successful in driving incremental traffic growth, resulting in the highest percentage of growth in visits so far in 2024 on a year-over-five-year basis.

Circle Week also saw a slightly higher dwell time, with visitors spending an average of 29 minutes in store, about a minute higher than 2024 year to date. The week performed well in visits exceeding 45 minutes compared to the year-to-date percentage of visits, which could signal that shoppers coming in for deals spend longer browsing and purchasing. There was also a higher percentage of weekday visits during Circle Week compared to 2024 overall, a promising sign for the week-long event.

Looking specifically at individual store locations that over performed during Circle Week, one that stood out is Target’s original large format store location in Katy, TX. This location opened in fall 2022 to much fanfare; it features a larger curbside pick-up area, multiple shop-in-shop concepts, and a larger grocery footprint. Traffic to the Katy location also increased the most in the week of July 8-14, but it far exceeded the total traffic growth to Target, with visits up almost 55% compared to the same week in 2023, when Target’s event ran last year. Circle Week also kept visitors in store longer at the Katy location, with dwell times increasing by 2 minutes on average compared to 2024 year-to-date.

With the success of this event in bringing in visitors, it will be interesting to see how Target tries to maintain the momentum through the back half of the year. With the announcement of price cuts and a renewed focus on providing as much value as possible to consumers, the enhanced Target Circle program appears to be bolstering those initiatives. As we get further away from the other retailer deal day events as well, we will be able to fully examine the effectiveness of this year’s summer promotional period and also provide more observations as we approach the holiday season.

Introduction

2024 has been another challenging year for retailers. Still-high prices and an uncertain economic climate led many shoppers to trade down and cut back on unnecessary indulgences. Value took center stage, as cautious consumers sought to stretch their dollars as far as possible.

But price wasn’t the only factor driving consumer behavior in 2024. This past year saw the rise of a variety of retail and dining trends, some seemingly at odds with one another. Shoppers curbed discretionary spending, but made room in their budgets for “essential non-essentials” like gym memberships and other wellness offerings. Consumers placed a high premium on speed and convenience, while at the same time demonstrating a willingness to go out of their way for quality or value finds. And even amidst concern about the economy, shoppers were ready to pony up for specialty items, legacy brands, and fun experiences – as long as they didn’t break the bank.

How did these currents – likely to continue shaping the retail landscape into 2025 – impact leading brands and categories? We dove into the data to find out.

Conventional Value Reaching Its Ceiling

Bifurcation has emerged as a foundational principle in retail over the past few years: Consumers are increasingly gravitating toward either luxury or value offerings and away from the ‘middle.’ Add extended economic uncertainty along with rapid expansions and product diversification from top value-oriented retailers, and you have an explosion of visits in the value lane.

But we are seeing a ceiling to that growth – especially in the discount & dollar store space. Throughout 2023 and the first part of 2024, visits to discount & dollar stores increased steadily. But no category can sustain uninterrupted visit growth forever. Since April 2024, year–over-year (YoY) foot traffic to the segment has begun to slow, with September 2024 showing just a modest 0.8% YoY visit increase.

Discount & dollar stores, which attract lower-income shoppers compared to both grocery stores and superstores, have also begun lagging behind these segments in visit-per-location growth. In Q3, the average number of visits to each discount and dollar store location remained essentially flat compared to 2023 (+0.2%), while visits per location to superstores and grocery stores grew by 2.8% and 1.0%, respectively. As 2024 draws to a close, it is the latter segments, which appeal to shoppers with incomes closer to the nationwide median of $76.1K, which are seeing better YoY performance.

The deceleration doesn’t mean that discount retailers are facing existential risk – discount & dollar stores are still extremely strong and well-positioned with focused offerings that resonate with consumers. The visitation data does suggest, however, that future growth may need to focus on initiatives other large-scale fleet expansions. Some of these efforts will involve moving upmarket (see pOpShelf), some will focus on fleet optimization, and others may include new offerings and channels.

Return of the middle anyone?

Innovative and Disruptive Value Shake Up Retail and Dining

Still, in an environment where consumers have been facing the compounded effects of rising prices, value remains paramount for many shoppers. And brands that have found ways to let customers have their cake and eat it too – enjoy specialty offerings and elevated experiences without breaking the bank – have emerged as major visit winners this year.

Trader Joe’s Drives Visits With Private Label Innovation

Trader Joe’s, in particular, has stood out as one of the leading retail brands for innovative value in 2024, a trend that is expected to continue into 2025.

Trader Joe’s dedicated fan base is positively addicted to the chain’s broad range of high-quality specialty items. But by maintaining a much higher private label mix than most grocers – approximately 80%, compared to an industry average of 25% to 30% – the retailer is also able to keep its pricing competitive. Trader Joe’s cultivates consumer excitement by constantly innovating its product line – there are even websites dedicated to showcasing the chain’s new offerings each season. In turn, Trader Joe’s enjoys much higher visits per square foot than the rest of the grocery category: Over the past twelve months, Trader Joe’s drew a median 56 visits per square foot – compared to 23 for H-E-B, the second-strongest performer.

Chili’s Beats QSR at its Own Game

Casual dining chain Chili’s has also been a standout on the disruptive value front this past year – offering consumers a full-service dining experience at a quick-service price point.

Chili’s launched its Big Smasher Burger on April 29th, 2024, adding the item to its popular ‘3 for Me’ offering, which includes an appetizer, entrée, and drink for just $10.99 – lower than than the average ticket at many quick-service restaurant chains. The innovative promotion, which has been further expanded since, continues to drive impressive visitation trends. With food-away-from-home inflation continuing to decelerate, this strategy of offering deep discounts is likely to continue to be a key story in 2025.

The Convenience Myth

Convenience is king, right?

Well, probably not. If convenience truly were king, visitors would orient themselves to making fewer, longer visits to retailers – to minimize the inconvenience of frequent grocery trips and spend less time on the road. But analyzing the data suggests that, while consumers may want to save time, it is not always their chief concern.

Looking at the superstore and grocery segments (among others) reveals that the proportion of visitors spending under 30 minutes at the grocery store is actually increasing – from 73.3% in Q3 2019 to 76.6% in Q3 2024. This indicates that shoppers are increasingly willing to make shorter trips to the store to pick up just a few items.

At the same time, more consumers than ever are willing to travel farther to visit specialty grocery chains in the search of specific products that make the visit worthwhile.

Cross visitation between chains is also increasing – suggesting that shoppers are willing to make multiple trips to find the products they want – at the right price point. Between Q3 2023 and Q3 2024, the share of traditional grocery store visitors who also visited a Costco at least three times during the quarter grew across chains.

Does this mean convenience doesn’t matter? Of course not. Does it indicate that value, quality and a love of specific products are becoming just as, if not more, important to shoppers? Yes.

The implications here are very significant. If consumers are willing to go out of their way for the right products at the right price points – even at the expense of convenience – then the retailers able to leverage these ‘visit drivers’ will be best positioned to grow their reach considerably. The willingness of consumers to forego convenience considerations when the incentives are right also reinforces the ever-growing importance of the in-store experience.

So while convenience may still be within the royal family, the role of king is up for grabs.

Serving Diners Quicker With Automatization

Chipotle Draws Crowds With Autocado

Convenience may not be everything, but the drive for quicker service has emerged as more important than ever in the restaurant space. Diners want their fast food… well, as fast as possible. And to meet this demand, quick-service restaurants (QSRs) and fast-casual chains have been integrating more technology into their operations. Chipotle has been a leader in this regard, unveiling the “Autocado” robot at a Huntington Beach, California location last month. The robot can peel, pit, and chop avocados in record time, a major benefit for the Tex-Mex chain.

And the Autocado seems to be paying off. The Huntington Beach location drew 10.0% more visits compared to the average Chipotle location in the Los Angeles-Long Beach-Anaheim metro area in Q3 2024. Visitors are visiting more frequently and getting their food more quickly – 43.9% of visits at this location lasted 10 minutes or less, compared to 37.5% at other stores in the CBSA.

Are diners flocking to this Chipotle location to watch the future of avocado chopping in action, or are they enticed by shorter wait times? Time will tell. But with workers able to focus on other aspects of food preparation and customer service, the innovation appears to be resonating with diners.

McDonald’s Leans into Automation in Texas

McDonald’s, too, has leaned into new technologies to streamline its service. The chain debuted its first (almost) fully automated, takeaway-only restaurant in White Settlement, TX in 2022 – where orders are placed at kiosks or on app, and then delivered to customers by robots. (The food is still prepared by humans.) Unsurprisingly, the restaurant drives faster visits than other local McDonald’s locations – in Q3 2023, 79.7% of visits to the chain lasted less than 10 minutes, compared to 68.5% for other McDonald’s in the Dallas-Fort Worth-Arlington, TX CBSA. But crucially, the automated location is also busier than other area McDonald’s, garnering 16.8% more visits in Q3 than the chain’s CBSA-wide average. And the location draws a higher share of late-night visits than other area McDonald’s – customers on the hunt for a late-night snack might be drawn to a restaurant that offers quick, interaction-free service.

Evolving Retail Formats - Finding the Right Fit

Changing store formats is another key trend shaping retail in 2024. Whether by reducing box sizes to cut costs, make stores more accessible, or serve smaller growth markets – or by going big with one-stop shops, retailers are reimagining store design. And the moves are resonating with consumers, driving visits while at the same improving efficiency.

Macy’s Draws Local Weekday Visitors With Small-Format Stores

Macy’s, Inc. is one retailer that is leading the small-format charge this year. In February 2024, Macy’s announced its “Bold New Chapter” – a turnaround plan including the downsizing of its traditional eponymous department store fleet and a pivot towards smaller-format Macy’s locations. Macy’s has also continued to expand its highly-curated, small-format Bloomie’s concept, which features a mix of established and trendy pop-up brands tailored to local preferences.

And the data shows that this shift towards small format may be helping Macy’s drive visits with more accessible and targeted offerings that consumers can enjoy as they go about their daily routines: In Q3 2024, Macy’s small-format stores drew a higher share of weekday visitors and of local customers (i.e. those coming from less than seven miles away) than Macy’s traditional stores.

Harbor Freight Tools and Ace Hardware Serve Smaller Growth Markets With Less Square Footage

Small-format stores are also making inroads in the home improvement category. The past few years have seen consumers across the U.S. migrating to smaller suburban and rural markets – and retailers like Harbor Freight Tools and Ace Hardware are harnessing their small-format advantage to accommodate these customers while keeping costs low.

Harbor Freight tools and Ace Hardware’s trade areas have a high degree of overlap with some of the highest growth markets in the U.S., many of which have populations under 200K. And while it can be difficult to justify opening a Home Depot or Lowe’s in these hubs – both chains average more than 100,000 square feet per store – Harbor Freight Tools and Ace Hardware’s smaller boxes, generally under 20,000 square feet, are a perfect fit.

This has allowed both chains to tap into the smaller markets which are attracting growing shares of the population. And so while Home Depot and Lowe’s have seen moderate visits declines on a YoY basis, Harbor Freight and Ace Hardware have seen consistent YoY visit boosts since Q1 2024 – outperforming the wider category since early 2023.

Hy-Vee Bucks the Trend by Going Big

Are smaller stores a better bet across the board? At the end of the day, the success of smaller-format stores depends largely on the category. For retail segments that have seen visit trends slow since the pandemic – home furnishings and consumer electronics, for example – smaller-format stores offer brands a more economical way to serve their customers. Retailers have also used smaller-format stores to better curate their merchandise assortments for their most loyal customers, helping to drive improved visit frequency.

That said, a handful of retailers, such as Hy-Vee, have recently bucked the trend of smaller-format stores. These large-format stores are often designed as destination locations – Hy-Vee’s larger-format locations usually offer a full suite of amenities beyond groceries, such as a food hall, eyewear kiosk, beauty department, and candy shop. Rather than focusing on smaller markets, these stores aim to attract visitors from surrounding areas.

Visit data for Hy-Vee’s large-format store in Gretna, Nebraska indicates that this location sees a higher percentage of weekend visits than other area locations – 37.7% compared to 33.1% for the chain’s Omaha CBSA average – as well as more visits lasting over 30 minutes (32.9% compared to 21.9% for the metro area as a whole). For these shoppers, large-format, one-stop shops offer a convenient – and perhaps more exciting – alternative to traditionally sized grocery stores. The success of the large-format stores is another sign that though convenience isn’t everything in 2024, it certainly resonates – especially when paired with added-value offerings.

A Resurgence of Legacy Brands

Many retail brands have entrenched themselves in American culture and become an extension of consumers' identities. And while some of these previously ubiquitous brands have disappeared over the years as the retail industry evolved, others have transformed to keep pace with changing consumer needs – and some have even come back from the brink of extinction. And the quest for value notwithstanding, 2024 has also seen the resurgence of many of these (decidedly non-off-price) legacy brands.

In apparel specifically, Gap and Abercrombie & Fitch – two brands that dominated the cultural zeitgeist of the 1990s and early 2000s before seeing their popularity decline somewhat in the late aughts and 2010s – may be staging a comeback. Bed Bath & Beyond, a leader in the home goods category, is also making a play at returning to physical retail through partnerships.

Anthropologie, another legacy player in women’s fashion and home goods, is also on the rise. Anthropologie’s distinctive aesthetic resonates deeply with consumers – especially women millennials aged 30 to 45. And by capturing the hearts of its customers, the retailer stands as a beacon for retailers that can hedge against promotional activity and still drive foot traffic growth.

And visits to the chain have been rising steadily. In Q4 2023, the chain experienced a bigger holiday season foot traffic spike than pre-pandemic, drawing more overall visits than in Q4 2019. And in Q3 2024, visits were higher than in Q3 2023.

Meeting the Evolving Needs of Millennials

And speaking of the 35 to 40 set – the generation that all retailers are courting? Millennials. Does that sound familiar? Yes, because this is the same generational cohort that retailers tried to target a decade ago. As millennials have aged into the family-formation stage of life, their retail needs have evolved, and the industry is now primed to meet them.

Sam’s Club Draws Value-Conscious Singles and Starters

From the revival of nostalgic brands like the Limited Too launch at Kohl’s to warehouse clubs expanding memberships to younger consumers as they move to suburban and rural communities, there are myriad examples of retailers reaching out to this cohort. And Sam’s Club offers a prime example of this trend.

Over the past few years, millennials and Gen-Zers have emerged as major drivers of membership growth at Sam’s Club, drawn to the retailer’s value offerings and digital upgrades – like the club’s Scan & Go technology. Over the same period, Sam’s Club has grown the share of “Singles and Starters” households in its captured market from 6% above the national benchmark in Q3 2019 to 15% in Q3 2024. And with plans to involve customers in co-creating products for its private-label brand, Sam’s Club may continue to grow its market share among this value-conscious – but also discerning and optimistic – demographic.

Taco Bell Brings in Crowds With Value Nostalgia Menu

Millennials are also now old enough to wax nostalgic about their youth – and brands are paying attention. This summer, Taco Bell leaned into nostalgia with a promotion bringing back iconic menu items from the 60s, 70s, 80s, and 90s – all priced under $3. The promotion, which soft-launched at three Southern California locations in August, was so successful that the company is now offering the specials nationwide. The three locations that trialed the “Decades Menu” saw significant boosts in visits during the promotional period compared to their daily averages for August. And people came from far and wide to sample the offerings – with a higher proportion of visitors traveling over seven miles to reach the stores while the items were available.

What Lies Ahead?

Hot on the heels of a tumultuous 2023, 2024’s retail environment has certainly kept retailers on their toes. While embracing innovative value has helped some chains thrive, other previously ascendant value segments, including discount & dollar stores, may have reached their growth ceilings. Consumers clearly care about convenience – but are willing to make multiple grocery stops to find what they need. At the same time, legacy brands are plotting their comeback, while others are harnessing the power of nostalgia to drive millennials – and other consumers – through their doors.