.svg)

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

0

0

0

0

----------

0

0

Articles

Article

The Commuters Shaping Downtown ColumbusDowntown Columbus continues to anchor the metro’s economy, attracting a diverse mix of commuters that power its growing workforce.

Ezra Carmel

Jan 23, 2026

3 minutes

Article

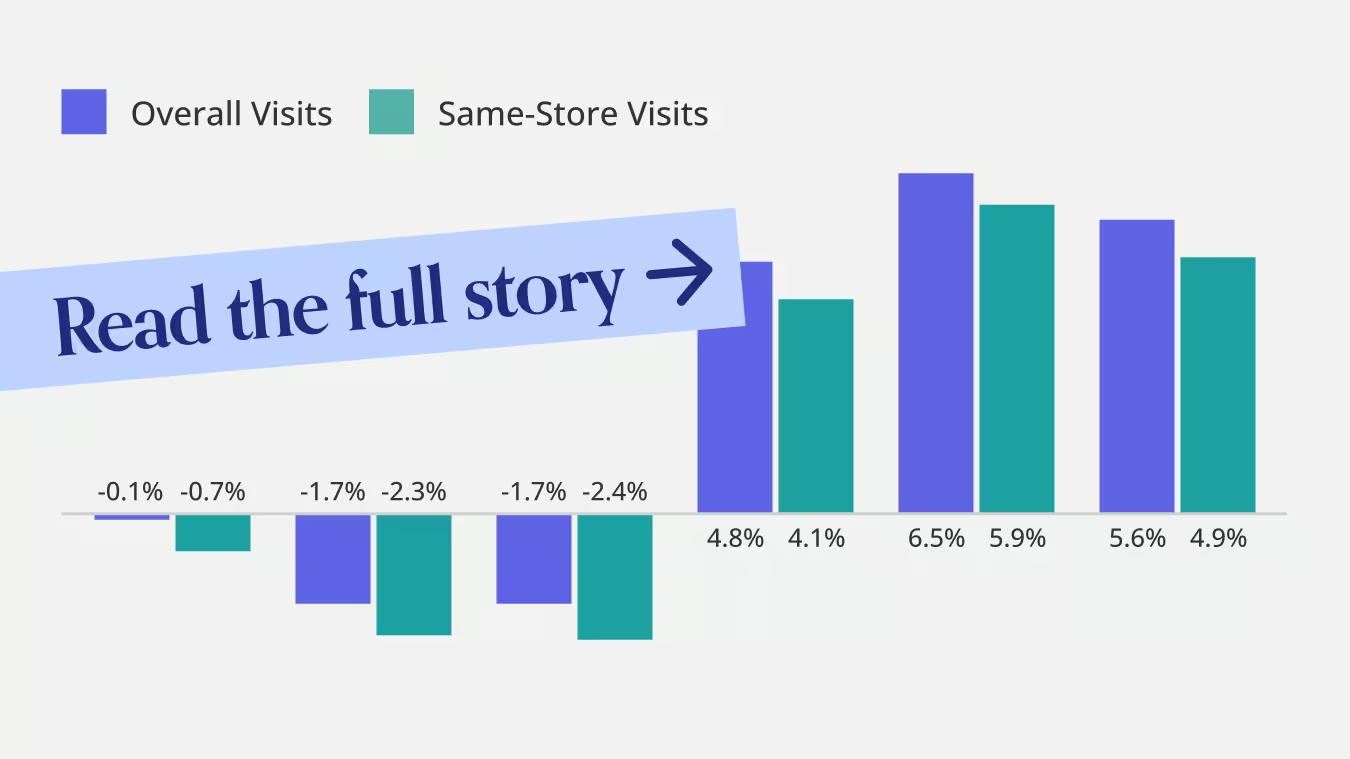

Chipotle’s Growth Is No Longer Just About New RestaurantsChipotle’s visit growth in 2025 was driven by expansion, but late-year data shows early signs of same-restaurant stabilization and faster pickup-driven visits gaining share.

Lila Margalit

Jan 22, 2026

3 minutes

Article

What Other QSR Brands Can Learn From McDonald’s Loyalty StrategyMcDonald’s ended 2025 with renewed visit momentum, driven in part by higher-frequency diners and its loyalty strategy. See what other QSR brands can learn about driving incremental growth through customer frequency.

Shira Petrack

Jan 21, 2026

3 minutes

Article

Opportunity vs. Operational Reality in Dollar Tree's 99 Cents Only AcquisitionDollar Tree’s 99 Cents Only lease acquisition reveals a smart real estate land grab complicated by cannibalization – but with long-term upside from a more affluent shopper base.

Shira Petrack

Jan 20, 2026

3 minutes

.avif)

Article

Which Gym Is Right For You in 2026?Using AI-powered location analytics, we reveal which gyms are less crowded at peak times, skew younger or older, and attract the most singles.

Ezra Carmel

Jan 16, 2026

4 minutes

Article

Placer.ai Overall Retail, E-Commerce Distribution, Industrial Manufacturing Index, December 2025Brick-and-mortar retail closed 2025 strong, with rising foot traffic across stores, logistics hubs, and a stabilizing manufacturing sector.

Shira Petrack

Jan 15, 2026

2 minutes

Reports

INSIDER

Report

Rethinking the Mall Anchor in 2025: A Visit-Focused Approach Discover how mall anchors are transforming in 2025 – and how a foot-traffic-focused approach to choosing key tenants can drive visits and shopper engagement.

May 29, 2025

8 minutes

INSIDER

Report

Grocery in 2025: Visitation Trends and Consumer BehaviorDive into the data to see the trends shaping the grocery space in 2025 and uncover actionable insights for strategic decision-making in the competitive food-at-home market.

May 15, 2025

8 minutes

INSIDER

Report

The Current Pace of the Fitness SpaceDive into the data to explore recent visitation patterns and consumer trends in the fitness space - and uncover potential keys to success, rooted in location intelligence.

May 5, 2025

8 minutes

Loading results...

We couldn't find anything matching your search.

Browse one of our topic pages to help find what you're looking for.

For more in-depth analyses on a variety of subjects, explore Reports.

For more in-depth analyses on a variety of subjects, explore Reports.

INSIDER

Stay Anchored: Subscribe to Insider & Unlock more Foot Traffic Insights

Gain insider insights with our in-depth analytics crafted by industry experts

— giving you the knowledge and edge to stay ahead.