.svg)

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

0

0

0

0

----------

0

0

Articles

Article

Kohl’s: More Than a Meme?Find out if Kohl's is more than just a meme stock.

Lila Margalit

Jul 28, 2025

1 minute

Article

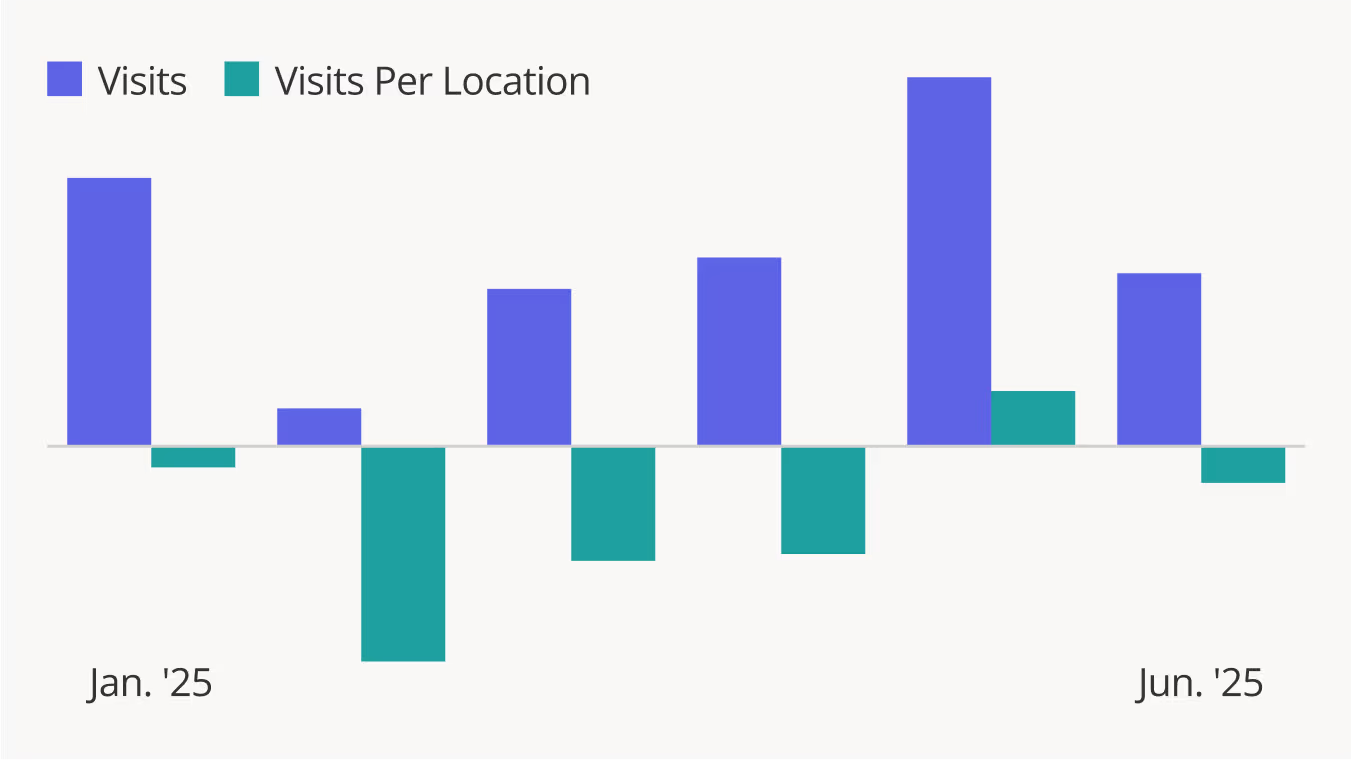

More From Less: How CVS's Rightsizing Strategy Drove Growth in Q2 2025CVS's rightsizing strategy is boosting performance. Our Q2 2025 analysis shows the chain's higher foot traffic and impressive visit growth per location with fewer stores.

Lila Margalit

Jul 28, 2025

3 minutes

.avif)

Guest Contributor

All The Things I Think I Think About Retail Over The Last Quarter: Kool-Aid, Kmart, and the Kohl’s Dumpster FireDiscover how Q1 retail predictions for Costco, Target, and Starbucks unfolded, revealing key lessons on brand identity and sustainable results.

Chris Walton

Jul 25, 2025

5 minutes

Article

Dutch Bros Visits Surge, Dunkin & Starbucks Traffic Trends Improve in Q2 2025Explore Starbucks' turnaround, Dunkin's value strategy, and Dutch Bros' rapid growth for key market insights.

Shira Petrack

Jul 24, 2025

3 minutes

Article

Decoding Shake Shack & Wingstop's Q2 2025 Visit PerformanceDiscover how Shake Shack and Wingstop's divergent Q2 2025 growth highlights strategies for engaging diverse diners and navigating economic shifts.

Shira Petrack

Jul 23, 2025

2 minutes

Article

Warby Parker & Allbirds Q2 2025: Unpacking Divergent Retail StrategiesDiscover how Warby Parker's expansion and Allbirds' rightsizing strategies drive unique paths to brick-and-mortar success in 2025 retail.

Bracha Arnold

Jul 22, 2025

2 minutes

Reports

INSIDER

Report

Office Attendance Drivers in 2026: The New Rules of Showing UpDive into the data to learn how convenience-driven behaviors are impacting the office recovery – and how stakeholders from employers to office owners and local retailers can best adapt.

February 5, 2026

INSIDER

Report

Five Ways Retailers Can Leverage AI Without Losing What WorksRead the report to learn how AI is changing store roles, operations, marketing, and fleet strategy – and how to apply it without undermining what already works.

January 29, 2026

INSIDER

Report

10 Top Brands to Watch in 2026Meet the ten retail and dining powerhouses, including H-E-B, Walmart, and Dave’s Hot Chicken, redefining success and winning consumer loyalty in 2026.

January 12, 2026

Loading results...

We couldn't find anything matching your search.

Browse one of our topic pages to help find what you're looking for.

For more in-depth analyses on a variety of subjects, explore Reports.

For more in-depth analyses on a variety of subjects, explore Reports.

INSIDER

Stay Anchored: Subscribe to Insider & Unlock more Foot Traffic Insights

Gain insider insights with our in-depth analytics crafted by industry experts

— giving you the knowledge and edge to stay ahead.