We checked in with McDonald’s, Wendy’s, Wingstop, and Shake Shack to see how they performed in Q2 2024 – and examined location analytics for McDonald’s latest concept – CosMc’s – to uncover emerging visitation trends for the new chain.

Ezra Carmel

Jul 23, 2024

3 minutes

Summer is a time when many consumers are on the go – and vacationers moving between activities look to quick-service restaurants (QSR) and fast-casual chains to fill up and beat the heat.

We checked in with McDonald’s, Wendy’s, Wingstop, and Shake Shack to see how they are performing heading into the summer, and examined location analytics for McDonald’s latest concept – CosMc’s – to uncover emerging visitation trends for the new chain.

Key Takeaways

In Q2 2024, Wingstop and Shack Shack saw respective year-over-year (YoY) visit growth of 31.9% and 28.3% – driven in part by the chains’ aggressive expansion strategies.

Also in Q2 2024, McDonald’s visits grew by 0.4% YoY and Wendy’s grew by 1.4%.

McDonald’s new CosMc’s restaurant draws higher-income consumers than the traditional McDonald’s chain – helping McDonald’s attract new audiences.

Wingstop and Shake Shack Sizzle in Summer

Popular wing and burger destinations Wingstop and Shake Shack are thriving this summer, as both chains double down on expansion plans. Shake Shack is on track to add dozens of new locations to its 300+ domestic shacks in 2024, and Wingstop’s hundreds of newly added locations bring its U.S. restaurant count to nearly 2000 venues.

These aggressive expansion strategies are playing a significant role in the chains’ respective visit growth. In June 2024, Wingstop’s visits were up 34.2% YoY, while Shake Shack’s were up 28.1%.

As the chains expand their footprints, both are taking steps to increase store efficiency and improve service. Wingstop recently adopted a new in-house transaction software, while Shack Shack continues to streamline the kiosk ordering experience.

Value on the Fast-Food Menu

The experience at many eateries continues to change – as do the prices diners see on their menus. During the first months of 2024, inflation drove price increases across the QSR space. And as consumers took note of the higher prices, “the summer of value wars” got underway – with a long list of chains, including fast-food giants McDonald’s and Wendy’s, introducing low-cost meals and menus to reel in inflation-wary diners.

Despite price hikes felt by consumers, in Q2 2024, McDonald’s visits grew by 0.4% YoY and Wendy’s grew by 1.4%. And the late-June launch of McDonald’s and Wendy’s new limited-time $5 bundles – which are already making their impact felt on the ground – may drive further foot traffic growth for the two chains throughout the summer.

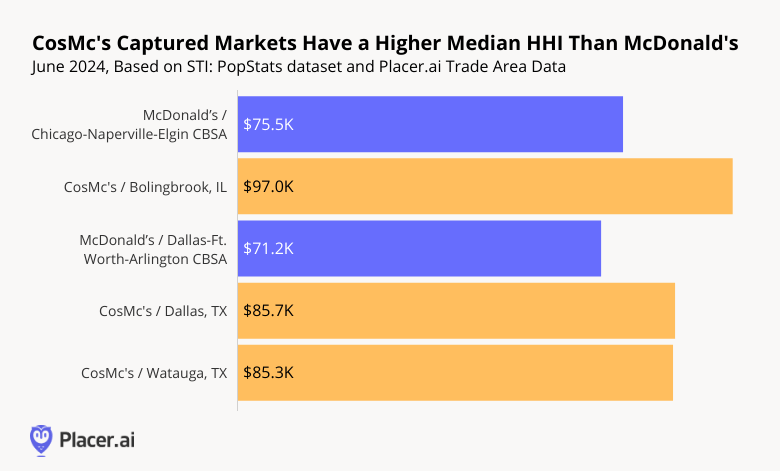

CosMc’s Draws Higher-Income Visitors into McDonald’s Orbit

While many fast-food diners are looking for value this summer, they’re also proving eager to try new culinary experiences. McDonald’s spin-off restaurant CosMc’s landed in late 2023, with throngs of eager diners lining up for a taste of the unique concept. Since the first location opened in Bolingbrook, IL, several new CosMc’s have emerged to heavy fanfare, including one in Watauga, TX and another in Dallas.

And although CosMc’s is still in its infancy, location analytics shows that the concept already drives traffic from more affluent consumers than the traditional McDonald’s chain.

In June 2024, for example, the median household income (HHI) in the captured market of the Bolingbrook, IL CosMc’s was $97.0K – significantly higher than that of McDonald’s in the Chicago metro area ($75.5K) or of McDonald’s nationwide ($65K).

A similar trend could be observed in the Dallas-Ft. Worth-Arlington CBSA – where the captured markets of local CosMc’s featured significantly higher median HHIs than those of McDonald’s.

As a beverage-led concept, CosMc’s may drive more traffic from higher-income consumers than a traditional McDonald’s – where simple soft drinks typically come as an inexpensive meal add-on. And as a result, the chain may help McDonald’s bring a new consumer cohort into the fold.

Looking Ahead

Summer 2024 is undoubtedly shaping up to be the “Summer of Value” and perhaps the “Summer of Fast Food” as well. Will favorable trends continue in the months ahead?

How did Chipotle and sweetgreen fare in the second quarter of 2024 – and what are they doing right? We dove into the data to find out.

Lila Margalit

Jul 22, 2024

4 minutes

The fast-casual space has been having a moment – with rising QSR prices leading many diners to embrace an upgraded experience. So with Q2 2024 in the rearview mirror, we dove into the data to check in with two fast-casual restaurant chains that have been doing particularly well: Chipotle and sweetgreen. How did their Q2 performance compare to that of the wider fast-casual segment? And what is it, exactly, that they are doing right?

We dove into the data to find out.

Key Takeaways:

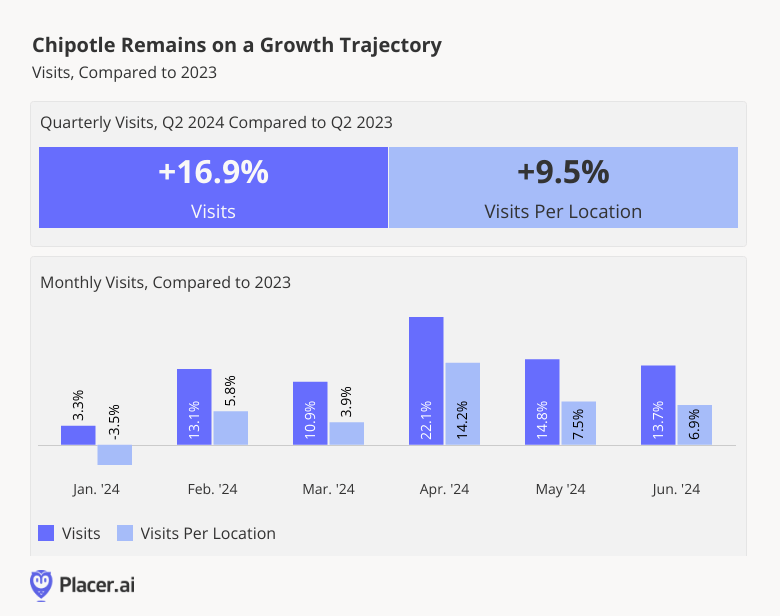

In Q2 2024, Chipotle saw year over year (YoY) increases in both overall visits (16.9%) and visits per location (9.5%) – outperforming the wider fast-casual segment on both metrics.

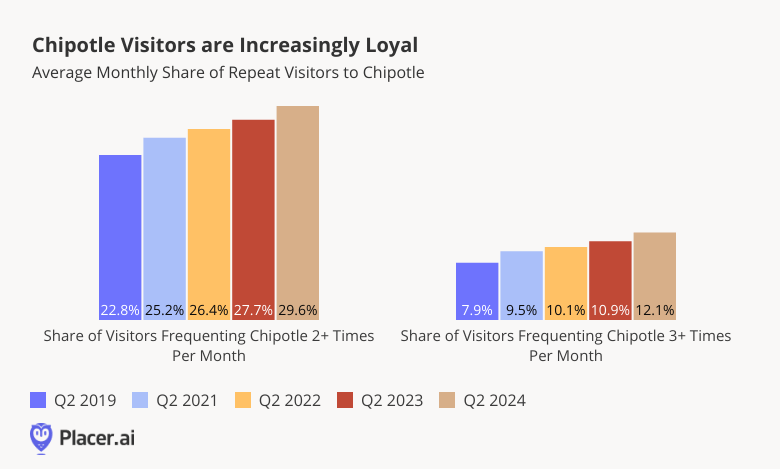

Chipotle’s growth is likely due in part to the growing loyalty of its customer base – which has increased significantly each year since 2019.

Sweetgreen also performed exceptionally well in Q2 2024, with visits and visits per location up a respective 19.9% and 5.9%.

Sweetgreen is finding success by leaning into what it does best – drawing the weekday lunchtime crowd.

Chipotle Rocks Q2 2024

In the first quarter of 2024, Chipotle reported a 14.1% YoY increase in total revenue, and a 7.0% increase in comparable restaurant sales. And the chain isn’t showing any signs of slowing down. In Q2 2024, Chipotle saw YoY chain-wide foot traffic growth of 16.9%. And while some of this increase was undoubtedly due to the chain’s continued expansion – Chipotle addedsome 247 U.S. restaurants over the past year – the average number of visits to each of Chipotle’s restaurants also increased by an impressive 9.5%. By way of comparison, fast-casual restaurants experienced average quarterly YoY visit growth of just 4.2%, and visit-per-location growth of 2.9%.

Leaning Into Loyalty

One factor that appears to be contributing to Chipotle’s remarkable visit growth is its repeat customer base – which is growing more loyal with every passing year. Between Q2 2019 and Q2 2024, the share of visitors frequenting a Chipotle at least twice a month increased from 22.8% to 29.6%, while the share of visitors frequenting a Chipotle at least three times a month grew from 7.9% to 12.1%.

This rise in loyalty has taken place against the backdrop of Chipotle’s growing loyalty program – Chipotle Rewards – which launched in Q1 2019 and today boasts more than 40 million members. The program, which lets members earn points for every dollar spent, offers diners access to personalized deals and a range of special promotions – like free delivery on National Burrito Day. (Before you ask, foot traffic data shows that National Burrito Day, which fell on Thursday, April 4th, 2024 wasn’t just a day for ordering online: It was Chipotle’s busiest Thursday of the year so far, with visits up 19.7% compared to a regular Thursday). This April, Chipotle also partnered with Tekken 8 to offer diners in-game currency in exchange for orders – with special perks for Rewards members.

Sweetgreen’s Growing Momentum

Another eatery that has been performing remarkably well in 2024 is sweetgreen – the fast-casual restaurant known for its healthy, fresh food. During Q2 2024, visits to sweetgreen were up a remarkable 19.9% YoY, a reflection of the chain’s growingfootprint. But foot traffic data shows that there is more than enough demand to sustain sweetgreen’s accelerated expansion – over the analyzed period, the average number of visits to each sweetgreen location also increased by 5.9%.

A Lunchtime Fave

A look at the hourly distribution of visits to sweetgreen shows that though the chain has made inroads into the dinner daypart, lunchtime remains its prime time to shine – especially on weekdays.

During the first half of 2024, 24.9% of weekday visits to sweetgreen took place between noon and 2:00 PM – compared to just 21.7% for the wider fast-casual category. But while sweetgreen, popular among the in-office crowd, drew a greater share of lunchtime visitors on weekdays, the fast-casual segment as a whole drew a greater share of lunchtime visitors on the weekends. Indeed, on Saturdays and Sundays, the share of lunchtime sweetgreen visitors dropped to 22.7%, while the share of fast-casual lunchtime visitors increased to 22.2%.

Still, suppertime is also a popular daypart for the salad chain on weekdays – with 20.0% of Monday - Friday visits taking place between 6:00 and 8:00 PM. As sweetgreen continues to lean into steaks and other dinner fare, it will be interesting to see if the restaurant begins to capture even more evening traffic.

Looking Ahead

Chipotle’s and sweetgreen’s strong quarter positions them well for further growth as the year wears on. Will Chipotle’s loyalty continue to increase? And will sweetgreen double down on dinner?

Follow Placer.ai’s data-driven restaurant analyses to find out.

Millennials everywhere, rejoice, because a beloved brand is back, for the next generation. Limited Too, an apparel staple for girls growing up in the 1990’s and 2000’s, has found its way back to the retail stage after years of dormancy. The brand began teasing its return a month ago, but last week brought the announcement that Limited Too’s relaunch will take place via a new apparel line at Kohl’s. With the Fourth of July over and Amazon Prime Day complete, the back-to-school season is officially upon us, even if it still feels like summer. In Kohl’s press release on Friday, the Limited Too introduction is a part of its larger back-to-school efforts, and it appears to be aimed at expanding apparel offerings for girls. And, with Kohl’s recent and upcoming additions like Sephora, Babies”R”Us, and now Limited Too, the target is clearly to woo and excite the Millennial shopper.

The relaunch of Limited Too includes fashion for girls size 7-16, the same Tween demographic that the brand originally captured. Mall-based Limited Too shut its doors in 2008, and the majority of stores were converted into rival retailer, Justice, who shuttered all of its stores in 2020. The brand revival is likely positioned by Kohl’s to appeal to parents who grew up with an affinity for the brand who can now purchase for their children.

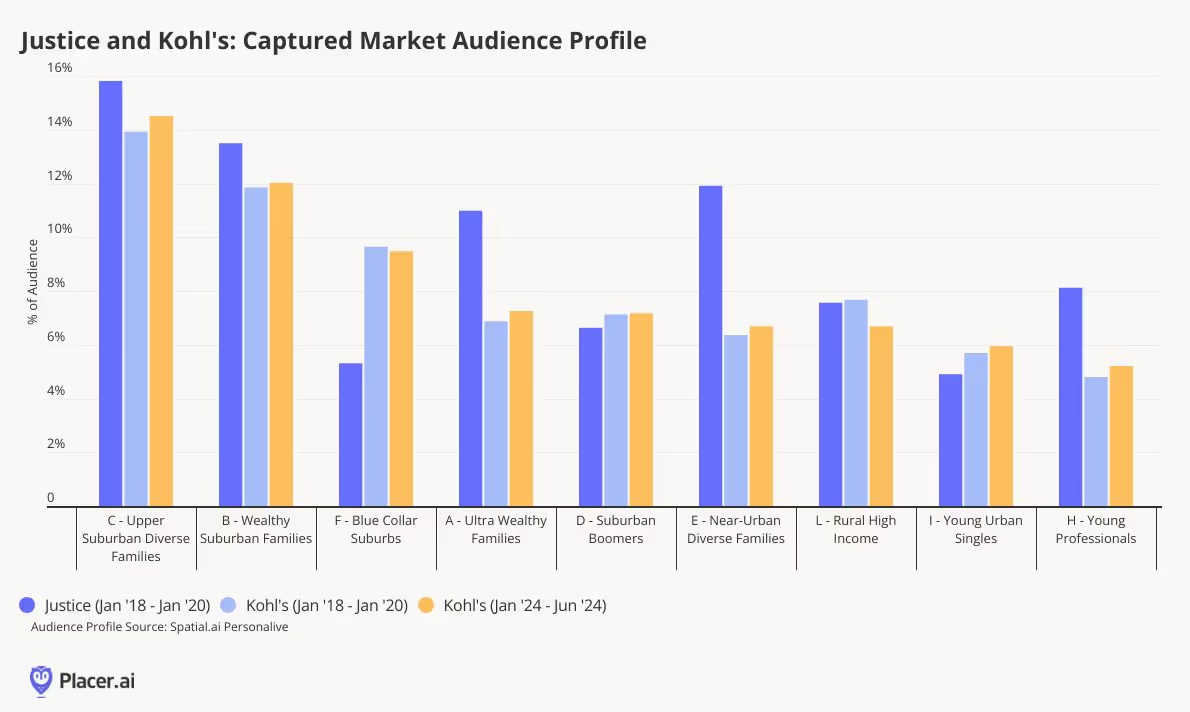

With the relaunch, how well situated is Kohl’s to attract this ideal “Limited Too Loyalist”? We took a look at a sampling of former Justice stores prior to closing, from 2018 to January 2020, and compared the audience profile of Justice visitors to Kohl’s visitors using Spatial.ai PersonaLive, both during the same time period as well as in 2024.

Our data highlights that both retailers actually have a similar audience profile of visitors, and that Kohl’s has continued to grow its percentage of Upper Suburban Diverse Families and Wealthy Suburban Families to more closely align with the former Justice demographics. Since the pandemic and through its new partnerships and planned additions, Kohl’s has been able to capture wealthier suburban families, and as Millennials continue to migrate out of urban centers, the retailer may have set itself up well to welcome these shoppers.

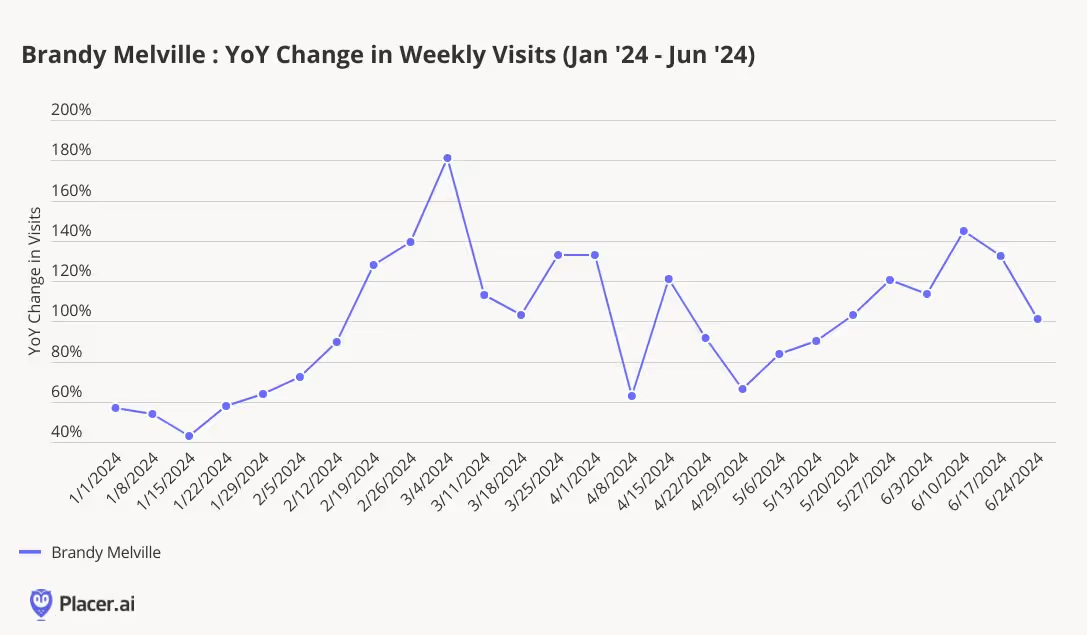

The tween apparel market today is highly fragmented, as is true with most areas of discretionary retail, with shoppers having access to countless brands and channels to choose from. Mass merchants, fast fashion, and athleisure brands are all vying for the attention of tweens, who are in turn influencing the retail decisions of their parents. A few months ago, we wrote about Brandy Melville, a somewhat controversial retailer that is still hugely popular with tweens. The retailer has the cool and elusive styling that young shoppers crave, and continues to be a strong traffic performer so far in 2024 (below). We’ve also written about the renaissance of Abercrombie & Fitch, another 2000’s brand with a strong connection to Millennials that has been able to recapture visitors’ attention, and still operates the Abercrombie Kids brand aimed at the same size range as the newly launched Limited Too.

Kohl’s new bet for the back-to-school season hangs on appealing to nostalgic Millennial parents, a group that quickly is becoming a target for many retailer strategies. We wrote last week about the rise of younger visitors to warehouse clubs, and the importance of younger shoppers to growing the member base. In a competitive and value-oriented retail environment, appealing to this group and gaining their loyalty in visits is critical to long-term success. It will be interesting to see if the Millennial love for Limited Too still remains, even after all these years.

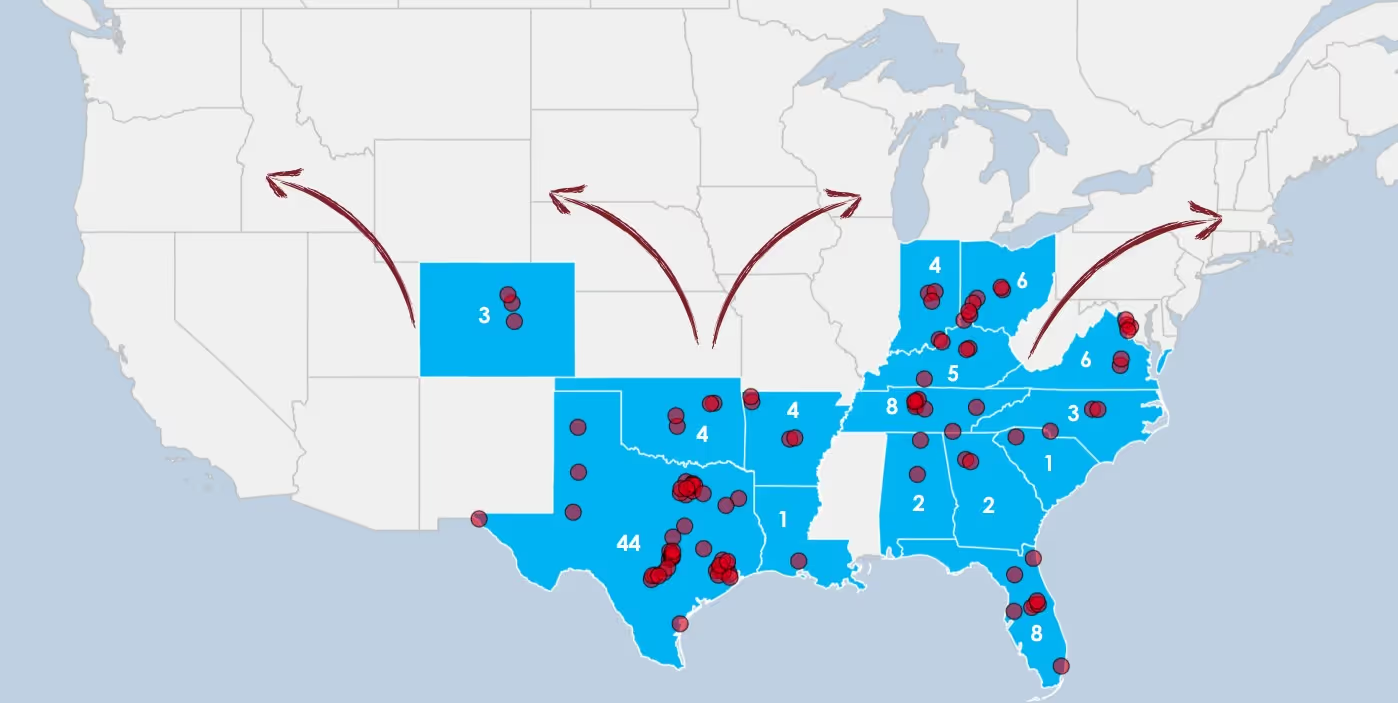

Another year, another acquisition for casual-dining restaurant leader Darden Restaurants. Following up last year’s acquisition of Ruth’s Chris Steakhouse, Darden plans to acquire Chuy's for $605M (representing 10.3x Chuy’s trailing-twelve-month adjusted EBITDA of $59, or 8.2x adjusting for run-rate G&A costs that can be eliminated by adding Chuy’s to the Darden portfolio). Chuy’s is among the leading players in the Mexican casual-dining space in terms of revenue ($451M in revenue during 2023, adjusting for the extra week in the reporting calendar), average revenue per unit ($4.5M), and restaurant-level EBITDA (20%).

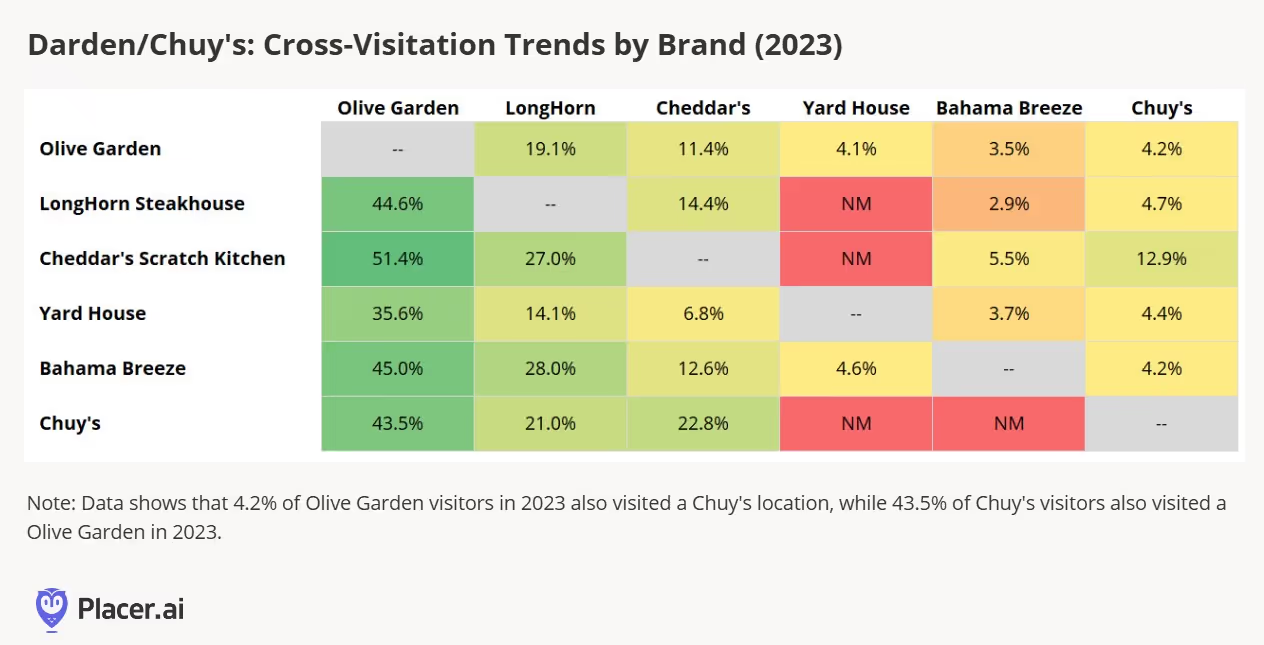

The acquisition of Chuy’s makes sense to us on a number of levels. First, and most obviously, Chuy’s fills a gap in the Darden portfolio. The company already owns the top player among casual-dining Italian chains (Olive Garden) and the number-two player in casual-dining steakhouses in addition to its other casual-dining (Cheddar’s, Yard House, Bahama Breeze) and fine-dining (Ruth’s Chris, The Capital Grille, Eddie V's, Seasons 52) concepts. By adding a casual-dining Mexican concept to its portfolio, we believe there will be an opportunity to attract incremental visitors. Below, we’ve presented cross visitation for Darden’s casual-dining brands and Chuy’s in 2023, and we see minimal overlap (although the cross-visit data is admittedly impacted by chain size and geography). According to our data, only 4%-5% of visitors to Darden’s existing restaurants also visited a Chuy’s location in 2023 (with the exception of Cheddar’s, which saw a 12.9% cross-visitation percentage).

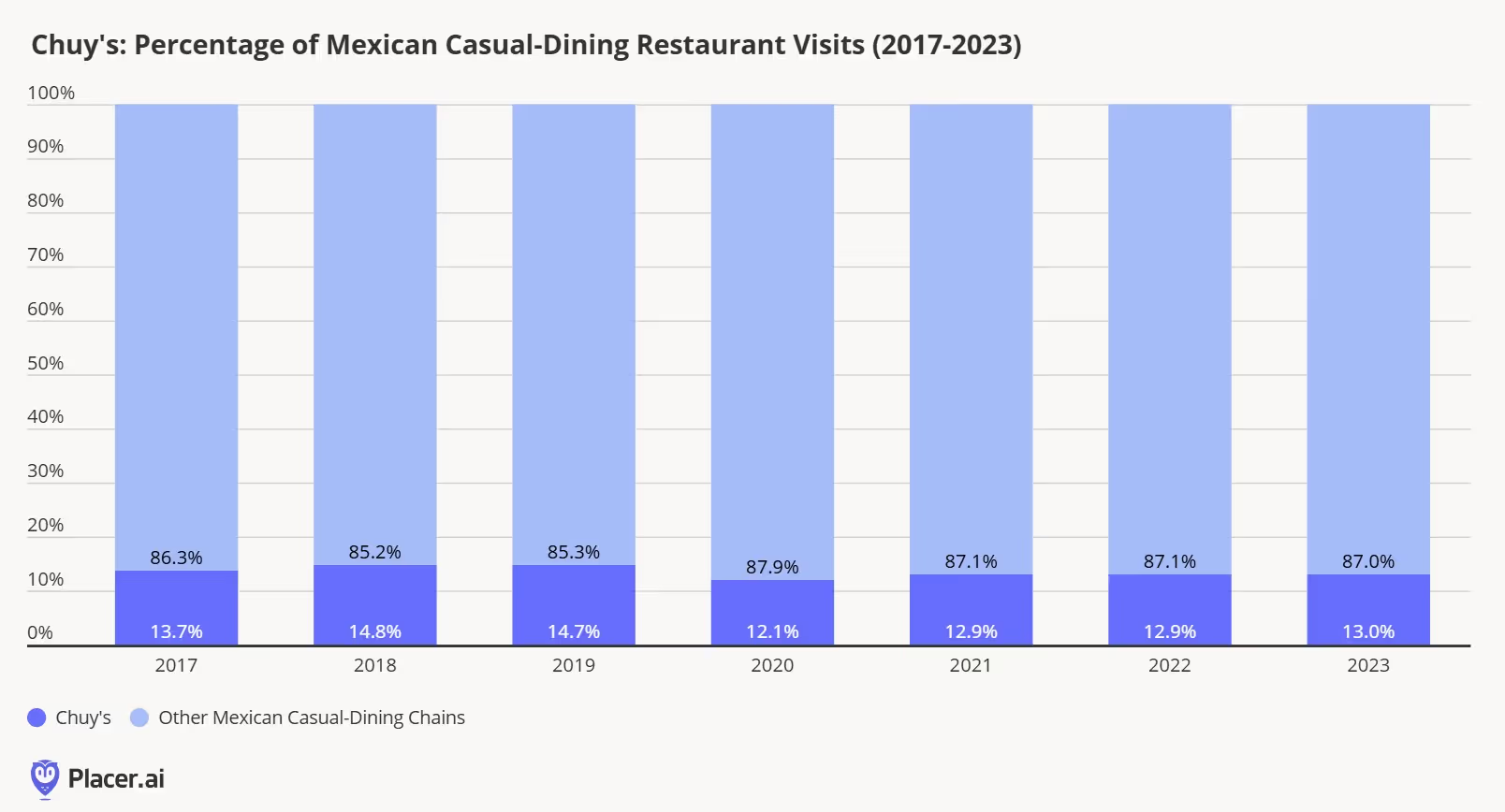

Second, despite Chuy’s being the leading player in the Mexican casual dining space, it’s still a relatively fragmented category that is ripe for consolidation. Below, we show the share of visitation data for Chuy’s compared to almost 20 other full-service Mexican restaurant chains from 2017-2023. Despite Chuy’s growth, its share of visits relative to the rest of the category has remained relatively healthy in the 12%-15% range. Backed by Darden’s purchasing, advertising, and real estate scale advantages, we see a meaningful opportunity to consolidate share of visits going forward, including visit per location improvement.

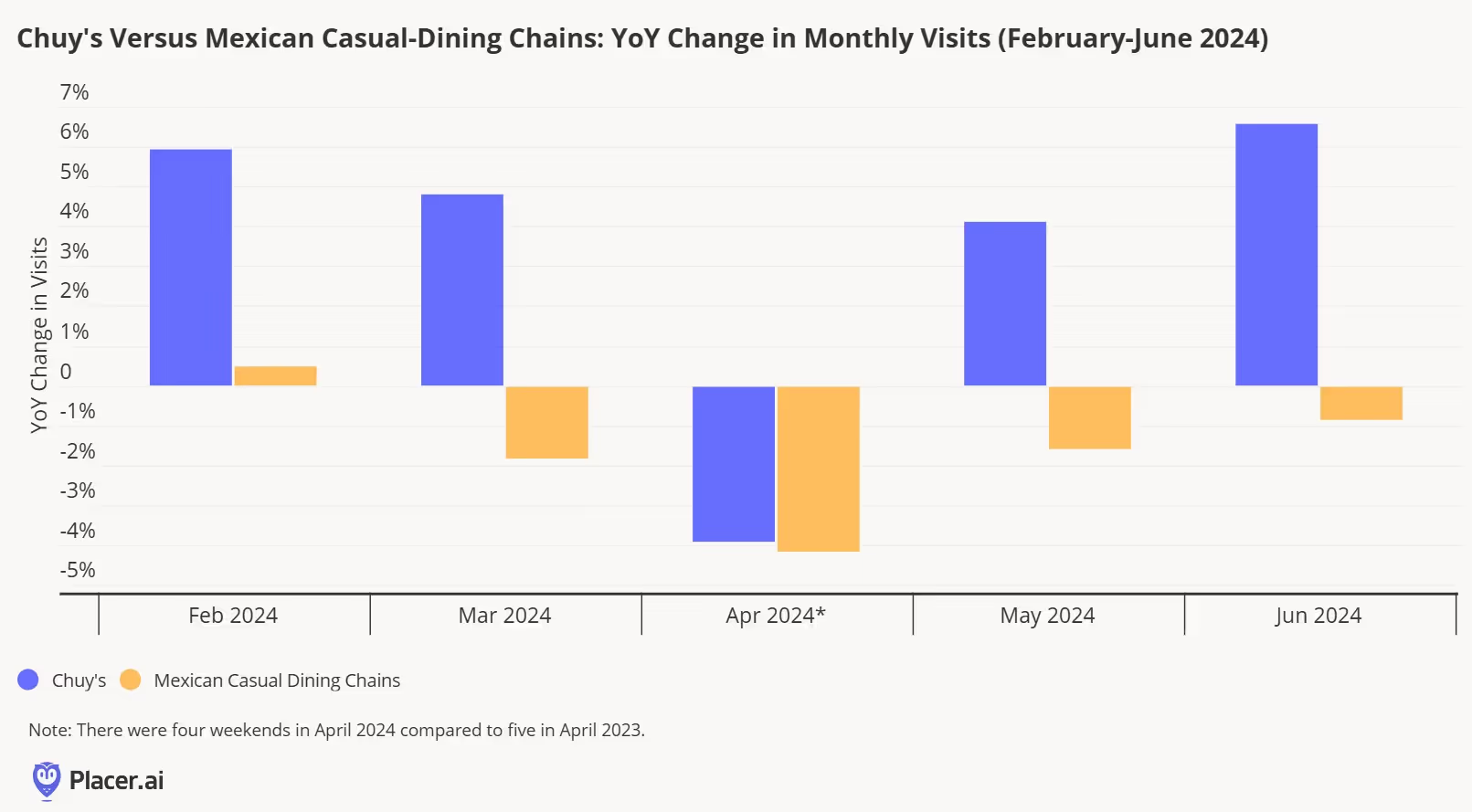

Chuy’s has been one of the leaders in the Mexican casual-dining chains in terms of visitation growth this year, outpacing monthly visits for the category by 5% on average (below). While integration will take time, applying guest experience, menu innovation, pricing, and marketing best practices from Darden should help to maintain this leadership.

At 101 company-owned restaurants today, Chuy’s is comparable to several other brands in the Darden portfolio (including Yard House at 88 units and Ruth’s Chris at 79). The chain is well established in Texas (44 company-owned units) but has a relatively small presence in other states across the Southeast and Midwest (below).

As Darden and Chuy’s management pointed out in a conference call to discuss the transaction, there are significant opportunities in both existing and new markets. Placer’s Site Selection tool (which identifies the characteristics of Chuy’s top locations–including trade area populations, demographic fit, cannibalization risk, and competition density–and finds markets/sites with similar characteristics) sees the best fits for expansion in several West, Midwest, and Northeast markets.

The first half of 2024 is proving to be more heavily visited for all types of shopping centers. June in particular is stronger than it was last year. After some January doldrums, where all shopping traffic was lower than the prior year due to weather, February began to pick up and March was particularly strong comparatively for outlet malls compared to last year. April saw a general downtick for more discretionary shopping, but May and June are looking strong so far.

The top 5 outlet malls by traffic during the last week of June were Arundel Mills, Ontario Mills, Sawgrass Mills, Legends Outlets Kansas City, and The Outlets at Orange. Among indoor malls, shoppers flocked to Mall of America, Roosevelt Field, Westfield Valley Fair, Del Amo Fashion Center, and Westfield Southcenter. Weather is always a consideration in the summer months, but as shopping centers have become increasingly sophisticated about strategically placed shade or places to take a break, it can be quite refreshing to visit an open-air lifestyle center. Tops in the nation for traffic include Ala Moana Center, Pier Park, Easton Town Center, Irvine Spectrum Center, and Victoria Gardens. As for high street retail corridors, no one can match the Big Apple. Three of the top five high streets were here, including Times Square and 42nd St at #1, SoHo at #3, and 5th Ave at #4. In second place was Michigan Ave in Chicago and in fifth place was Beverly Hills.

Against the backdrop of what remains a challenging time for full-service restaurants (FSRs), we dove into the data to check in with three of America’s leading FSR chains – First Watch, Texas Roadhouse, and Applebee’s. How did they fare in Q2 2024? And what lies in store for them in the months ahead?

Lila Margalit and Noam Maman

Jul 17, 2024

3 minutes

Against the backdrop of what remains a challenging time for full-service restaurants (FSRs), we dove into the data to check in with three of America’s leading FSR chains – First Watch, Texas Roadhouse, and Applebee’s. How did they fare in Q2 2024? And what lies in store for them in the months ahead?

Key Takeaways:

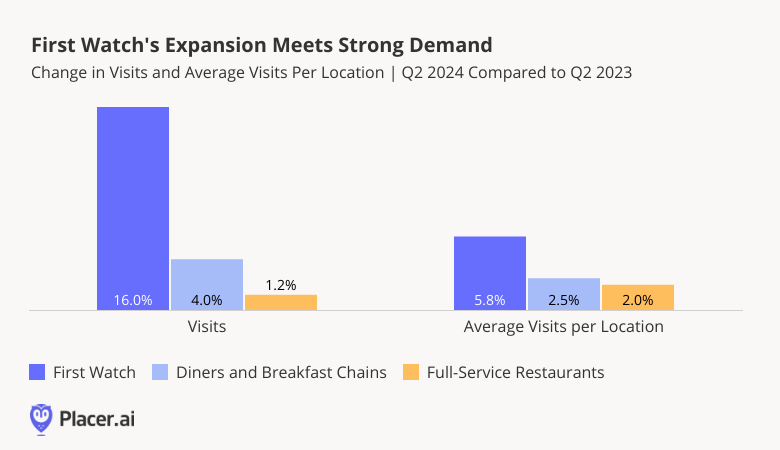

First Watch has embraced an aggressive growth strategy, and its efforts are bearing fruit: In Q2 2024, the chain saw substantial increase in both overall visits and in the average number of visits per location – outpacing both diners & breakfast chains and the wider FSR category.

Texas Roadhouse has also been in expansion mode, maintaining nearly consistent YoY visit and visit-per-location growth between January and June 2024.

In the wake of rightsizing moves by Applebee’s, the average number of visits to each of its restaurants is on the rise – a promising sign for the chain.

First Watch Rides the Wave

First Watch has emerged as a rising star in recent years, rapidly expanding its footprint while at the same time taking pains to preserve the feel of a small, local eatery. The restaurant is nimble on its feet – growing its audience through a strategy centered on continual menu innovation and special seasonal offerings.

In the past year alone, First Watch added dozens of new locations to its fleet. And foot traffic data shows that the chain’s aggressive growth strategy is meeting robust demand. In Q2 2024, YoY visits to First Watch grew by 16.0%, far outperforming FSR and diner & breakfast chain averages. And perhaps more importantly, the average number of visits to each individual First Watch restaurant rose 5.8% over the same period.

Texas Roadhouse in Growth Mode

Texas Roadhouse is another chain that has been crushing it in 2024 – and not just on Father’s Day. Over the past year, the popular steakhouse opened some 30new U.S. locations, and plans to continue expanding this year.

And foot traffic data shows that Texas Roadhouse’s high-quality, affordable offerings are resonating with consumers. Despite inflation-driven price hikes, YoY visits to the chain have continued to grow. And though some of this increase is due to the restaurant’s expansion, the average number of visits per location has also been on the rise: Between January and June 2024, Texas Roadhouse experienced near-consistent YoY visit and visit-per-location growth. Only in January and in April did visits per location falter, likely due to January’s inclement weather and an April Easter calendar shift.

On a quarterly basis, too, foot traffic to Texas Roadhouse increased 6.2% in Q2 2024 – significantly outpacing averages for both steakhouses (2.6%) and full-service restaurants (1.2%).

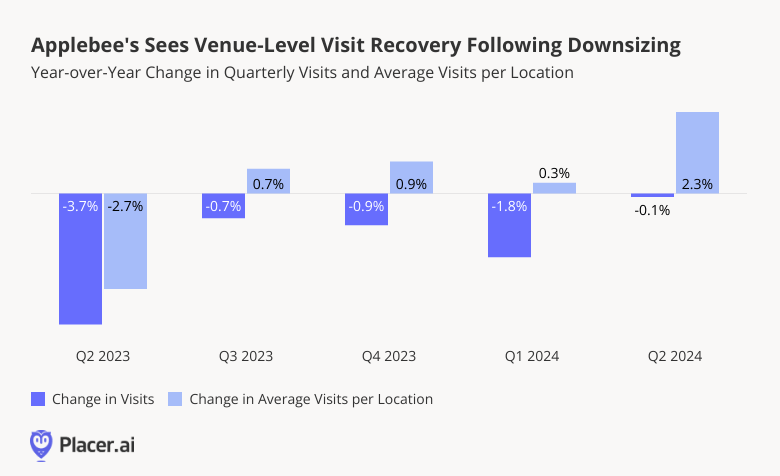

Applebee’s Rightsizes for Success

Like many full-service restaurants, Dine Brands’ Applebee’s has faced its share of headwinds in recent years. Over the past 12 months, Applebee’s shuttered at least 30 locations, contributing to a drop in the chain’s overall foot traffic. But analyzing changes in the average number of visits to each Applebee’s restaurant shows that the closures may actually be helping to put Applebee’s back on a firmer footing.

In Q2 2023, visits to Applebee’s nationwide declined 3.7% YoY, while the average number of visits per location dropped 2.7%. Since then, the chain’s YoY visit gap has narrowed – while the average number of visits per location has begun to increase. And in Q2 2024, Applebee’s closed its overall YoY visit gap and grew its visits per location by 2.3%. Though the chain has yet to return to positive unit growth, the rightsizing of its fleet appears to be bolstering Applebee’s remaining stores – positioning it for long-term success.

Bright Spots Amidst an Uncertain Future

Full-service restaurants have had a tough time in recent years, and concerns that consumer spending may moderate as the year wears on continue to weigh on the industry. Still, foot traffic data suggests that consumers are once again visiting restaurants – fueling expansion for First Watch and Texas Roadhouse, and helping shore up Applebee’s long-term prospects.

What does the rest of 2024 have in store for restaurant chains?

Follow Placer.ai’s data-driven restaurant analyses to find out.

How shifting consumer priorities are reshaping value perceptions across QSR, fast casual, and casual chains.

July 9, 2026

The New Definition of Value

As consumer sentiment hovers near historic lows and the cost of goods remains elevated, value has become a defining theme across the dining industry. Yet within the sector's diverse restaurant categories – and for individual brands – the question is no longer whether consumers are seeking value, but what value actually means. A closer look at chains across the industry suggests that, amid ongoing economic pressure, perceptions of value are evolving. For some consumers, value may be tied to affordability and promotions; for others, it may come from quality, convenience, or experience. The result is a market with multiple paths to winning consumer traffic.

Dining Traffic Remains Unstable in 2026

After an uneven but largely resilient 2025, dining traffic in 2026 tipped into a sustained decline.

Monthly visits to the overall dining industry have trailed year-ago levels throughout 2026, with February standing as the lone exception. That month saw a 3.7% year-over-year (YoY) increase in visits, driven in part by comparisons to the period of initial tariff announcements in early 2025. But broader trends remained challenged, and May's 2.5% YoY decline marked the steepest monthly drop of the past twelve months as rising gas prices and weakening consumer sentiment appear to have added pressure to an industry already navigating a difficult environment.

Breaking Down the Industry

These headwinds, though, have not landed evenly. Across the dining sector, some segments have faced more intense pressure than others, with much of the divide coming down to how consumers are perceiving value against experience.

QSR’s Value Proposition Under Pressure From Grocery Stores & Superstores

Over the past several years, inflation and rising menu prices have gradually weakened a cost-based value proposition that has long been central to the QSR segment. More recently, elevated gas prices have added another deterrent, making a trip through the drive-thru a less compelling choice for some consumers.

Strong performance at grocery stores and superstores suggests that competition for share-of-stomach is increasingly extending beyond traditional restaurant rivals. With expanding selections of ready-to-eat and pre-prepared meals, these channels are offering consumers a combination of value, convenience, and quality that can increasingly match limited-service dining options. At the same time, ongoing pressure on household budgets appears to be driving more consumers toward lower-cost meals made at home, creating additional headwinds for the QSR segment.

Fine Dining and the Fast Casual Middle Hold Firm

Yet for many consumers, there is still a time and place for dining out, and in the face of mounting economic pressure, several dining formats have found foot traffic success. Fine dining has posted traffic growth in nearly every month of 2026, with March standing as the lone exception. That decline was likely influenced by a calendar shift, as March 2026 contained one fewer Saturday than March 2025 – a meaningful headwind for full-service restaurants given the outsized role weekends play in driving visits. The segment's sustained growth points to the resilience of higher-income consumers and the enduring appeal of premium, occasion-driven dining experiences.

Fast casual and casual dining have also proven relatively resilient. The fast casual category saw positive YoY foot traffic in every month of 2026 so far, while casual dining's performance has rebounded since the March calendar shift that likely weighed on YoY traffic. A second calendar shift in May 2026 led to an extra Saturday in the month, which likely helped the segment's overall trend. These trends suggest that both fast casual and casual dining occupy an increasingly attractive middle ground where value is defined as a combination of affordability and experience. At the same time, years of menu price hikes at QSR chains have altered the cost equation in fast casual and casual dining's favor, narrowing the price gap between fast food and more elevated dining formats. As that gap has narrowed, consumers may be placing greater emphasis on experience and quality when deciding where to dine.

Inside the Playbooks of Fast Casual Standouts

The balance between price and elevated experience has made fast casual a favorite for value in the dining industry in 2026. A closer look at two of the segment's largest players, CAVA, a relatively young concept, and Chipotle, a legacy chain navigating operational challenges, shows how brands can deliver on that value proposition in different ways and win in today’s dining landscape.

Chipotle Creates Value With LTO Experiences and Loyalty Perks

Chipotle's traffic trends in 2026 have improved compared to 2025, with the brand offering a clear example of how fast casual brands can create value by pairing menu innovation with loyalty perks.

Chipotle outpaced the broader fast casual category in YoY visits nearly every week of 2026 so far. And the graph below shows that the chain's strongest traffic gains tended to coincide with major menu launches and loyalty initiatives – a key component of its ongoing "Recipe for Growth" strategy.

The return of fan-favorite Chicken al Pastor in the week of February 9, 2026 helped drive a 16.6% YoY increase in visits. Two months later, the launch of "Rewards on Repeat" – a refreshed loyalty program offering freebies upon sign-up – generated the period's largest weekly traffic gain, with visits rising 18.2% YoY. And the introduction of Honey Chicken on April 28 provided another boost, as the chain continued to rotate limited-time protein offerings and give customers reasons to return.

These performance peaks suggest that Chipotle has been particularly effective at pairing menu novelty with loyalty perks to reinforce a value proposition anchored by quality and experience.

Chipotle's "Recipe for Growth" Drives Traffic With Loyalty and LTO Launches

Year-over-Year Change in Weekly Visits, Chipotle vs. Fast Casual, Jan.–Jun. 2026

ChipotleFast Casual

Dashed lines mark key Chipotle promotional launch dates. Week-of dates shown; launches may have occurred mid-week.

Share

Embed:

CAVA Expansion and Differentiated Dining Experience

If Chipotle illustrates the power of menu innovation and loyalty-driven engagement, CAVA highlights a different approach to creating value – one rooted in variety, customization, and a consistently differentiated dining experience.

CAVA's overall visits climbed well above 20% YoY in every month of 2026, a pace largely driven by aggressive unit expansion. Meanwhile, same-store visits, which measure traffic at locations open for at least twelve months, sustained positive YoY growth – evidence of genuine demand at existing restaurants alongside a rapidly growing footprint.

While Chipotle leans on limited-time offers, CAVA's growth rests on a consistent, customizable experience. A deep roster of proteins paired with a wide range of bases, dips, and toppings, gives the chain built-in variety that helps keep the concept feeling fresh. In addition, CAVA's Mediterranean-inspired menu offers flavors and combinations that are less easily replicated at home, helping the brand maintain a differentiated experiential value proposition and drive growth.

O Though Chipotle and CAVA are at different points in their evolution and have taken different paths to growth, both highlight the enduring appeal of fast casual's balance of value and quality. In a dining environment where consumers are increasingly weighing cost against experience, the segment's ability to deliver on both has helped make it one of the industry's strongest-performing formats.

Casual Chains Thrive On Everyday Value

Fast casual isn't the only dining segment benefiting from consumers' evolving perception of value. In 2026, several casual dining chains have found success by pairing accessible price points with the elevated experience of a sit-down meal.

Brands such as BJ's Restaurant & Brewhouse, Chili's Grill & Bar, Bonefish Grill, Cicis, and The Cheesecake Factory all posted positive YoY visit growth in multiple months this year, demonstrating that even in a challenging economic environment, diners are motivated when they feel they are getting more in return. These results are particularly notable given the impact of calendar shifts, which weighed on March 2026 comparisons – and provided a tailwind to May performance.

Unlike many fast casual chains, these brands have not relied heavily on a steady stream of limited-time offers to drive traffic. While menu innovation remains part of the playbook, promotions often serve as ticket builders or engagement tools rather than primary traffic catalysts. Instead, these successful casual dining chains have focused on creating everyday value that diners can depend on, narrowing the price gap between limited-service restaurants and full-service dining.

The result is a value equation that encompasses table service, a more relaxed dining environment, and a place to socialize or celebrate an occasion. In an environment where consumers are increasingly weighing cost against overall experience, that combination appears to be helping several casual dining chains maintain positive traffic momentum.

The State of Dining in 2026

Although dining traffic has softened in 2026, the industry's performance suggests that consumers have not stopped spending on restaurants altogether. Instead, they have become more selective about where they dine and what they expect in return.

Across segments, the strongest performers have found different ways to deliver value. For some brands, that means menu innovation, loyalty engagement, and differentiated experiences. For others, it means dependable affordability paired with the service and atmosphere of a sit-down meal. As economic pressures continue to shape consumer behavior, the data suggests that value is no longer defined by price alone, but by the balance of cost, convenience, quality, and experience.

Find out where Americans are moving in 2026, why they're relocating, and how developers, investors, and retailers can stay ahead of the trends.

June 18, 2026

The Geography of Domestic Migration

During the pandemic and its aftermath, Americans were on the move. Millions left expensive coastal markets for lower-cost destinations across the Sun Belt, while boomtowns such as Bozeman, Boise, and Austin struggled to keep pace with the influx of new residents.

That wave of relocation has since cooled, as return-to-office mandates, higher mortgage rates, and a shrinking affordability gap between coastal cities and many COVID-era hotspots have dampened the incentive to move. But even in a slower market, domestic migration remains one of the most powerful forces shaping local economies, housing markets, and consumer demand.

This report leverages AI-powered location analytics to examine the relocation patterns reshaping the United States in 2026 – where Americans are moving, the demographic and economic forces driving those decisions, and how retailers, investors, developers, and policymakers can respond to the opportunities and challenges created by these shifts.

Which major metros are attracting the most new residents? Which pandemic-era standouts have seen growth stall or reverse? And what factors best predict a large metro area's domestic migration growth potential in 2026?

Interstate Flows: Which States Gained and Lost Residents?

South Carolina and Delaware Set the Pace

The latest statewide migration data shows that the slower relocation pace observed in 2024 persisted into 2025. No state recorded net inflows or outflows exceeding 0.7% of its starting population. And while several smaller states continued to attract new residents at meaningful rates, none of the nation's six most populous states saw net in-migration exceed 0.2%.

Among those smaller states, South Carolina and Delaware led the nation with net in-migration equal to 0.7% of their populations, followed by Idaho (0.6%), Maine (0.5%), Tennessee (0.4%), and North Carolina (0.3%). For most of these states, migration accelerated relative to 2024, though Delaware's inflow rate moderated slightly and North Carolina held steady.

Despite their differences, these states tend to offer a similar mix of lifestyle amenities, relatively low congestion, and opportunities for growth. Many also benefit from business-friendly climates, favorable taxpolicies, or housing costs that remain attractive relative to the higher-cost markets from which they draw new residents.

Vermont Trails Behind

At the other end of the spectrum was Vermont, which saw the nation’s largest net outflow as share of population in 2025, losing 0.4% of its population to domestic relocation. The decline deepens a reversal that first emerged in 2024, when the state swung to a net loss of 0.2%, after attracting inflows of 0.8% and 0.5% in 2022 and 2023, respectively.

Vermont's reversal likely reflects a combination of factors, including return-to-office mandates and the waning appeal of remote work. Housing undersupply in the state may have alsocontributed, illustrating how important infrastructure investments are to sustaining migration gains over time.

South Carolina, Delaware, and Idaho Lead the Nation in Domestic Migration Growth in 2025

Net Domestic Migration as a Share of Each State's Starting Population, 2025

Net Migration by State

−0.4%0.0%0.7%

Top Migration Magnets

2024

2025

*Analysis for each year is from Jan. – Dec.

Share

Embed:

Florida Sees Accelerated Inflow as Legacy Exodus States Slow Losses

Among the nation's six most populous states, Florida was the only one to see accelerating net in-migration in 2025, attracting new residents equal to 0.2% of its starting population, up from 0.1% the year before. Texas, by contrast, slowed from 0.1% net in-migration in 2024 to essentially flat in 2025, highlighting the cooling of what was once one of the country's strongest pandemic-era migration magnets.

Meanwhile, the legacy "exodus" states continue to lose residents, but at a slower pace than in previous years. Illinois and California have seen their migration deficits steadily narrow, with further improvement in 2025. Between 2022 and 2025, Illinois moved from -0.8% → -0.2% → -0.2% → -0.1%, while California moved from -0.9% → -0.4% → -0.3% → -0.2%. And though New York has held steady at -0.2% over the past two years, this marks a significant moderation from 2022, when the state experienced net outmigration equal to 1.1% of its population.

Major Insights:

Smaller states dominated migration gains in 2025, led by South Carolina, Delaware, Idaho, Maine, Tennessee, and North Carolina.

Vermont posted the nation's largest outflow after attracting strong inflows just a few years earlier.

Florida was the only top-population state to see meaningful net in-migration in 2025.

Texas' migration boom continued to cool, with net in-migration falling to flat in 2025.

Outmigration from New York, Illinois, and California is slowing, but these states are still losing residents overall.

Zooming In: Net Migration Across Metro Boundaries

Statewide trends reveal important shifts, but a closer look at the nation's ten largest metropolitan areas suggests that broader interstate averages increasingly mask diverging local realities. Several metros are attracting residents through interstate domestic migration even when their states as a whole are experiencing little or no net migration growth.

Phoenix (+0.3%), for example, stood out as the nation's top-performing large metro in 2025, despite Arizona's absence from the list of leading migration destinations – with the majority of its inflow coming from out of state.

Dallas (+0.2%) ranked second, continuing its rebound from -0.1% in 2023 even as Texas' statewide migration gains cooled. Like Phoenix, Dallas drew a majority of its new residents from outside the state, underscoring its growing appeal as a national migration destination. Houston, meanwhile, moved in the opposite direction, falling from 0.1% net in-migration in 2023 to -0.1% in 2025. While it is too early to call this a sustained reversal, the divergence between the two metros may reflect Dallas's growing pull as a corporate magnet alongside rising housing costs and weather-related challenges in Houston.

Metro-level data also suggests that the pandemic-era "big-city exodus" narrative is continuing to fade. Los Angeles improved from -0.8% in 2023 to -0.3% in 2025, while New York held steady at -0.3% after improving in 2024. Even Miami (-0.6%), which ranked last among major metros despite Florida's continued statewide gains, saw its outflows moderate from 2023 levels. And while Illinois continued to post net outmigration, Chicago (0.0%) reached migration neutrality in 2025 after recording losses in both 2023 and 2024.

Major Insights:

Phoenix was the nation's top large-metro migration destination in 2025.

Dallas gained momentum while Houston lost ground, highlighting growing divergence within Texas.

Miami continued to post the largest outflows among major metros despite Florida's broader migration success.

The LosAngeles, Chicago, and the New York metro areas all saw migration losses ease.

Florida Dominates Large Metros

Despite Miami's struggles – and Florida’s relatively modest 0.2% inflow – a look beyond the top 10 large metros reveals that the Sunshine State is home to six of the nation's eight fastest-growing large metros nationwide.

Those top-performing metros, defined as CBSAs with 500K+ residents that added at least 0.8% of their population through net domestic migration over the past year, share a similar profile: lower housing costs, retiree appeal, suburban density, and an easy drive to a larger economic hub.

Much of the growth of these Florida metro areas, however, is being fueled from within Florida itself. While major out-of-state metros such as New York (6.1%) and Chicago (2.0%) remained important sources of new residents, nearly half of the net migration into Florida's top destination metros came from elsewhere in the state. In 2025, Miami (22.5%), Orlando (13.0%), Tampa (5.8%), and Naples (4.2%) together accounted for 45.5% of the net positive migration feeding these fast-growing markets.

Major Insights:

Mid-sized Florida metros dominate the national migration leaderboard.

Florida's migration pipeline is overwhelmingly driven by in-state movement.

The Affordability Factor

The migration flows feeding the nation’s fastest-growing large metros suggest that affordability remains a powerful driver of domestic relocation.

In 2025, seven of the eight top destination metros analyzed above had lower typical home values than their largest feeder markets. Lakeland–Winter Haven, FL, for example, had a typical home value of $313.4K in December 2024, compared with $404.9K in Orlando and $380.2K in Tampa – its two largest sources of net migration. Even North Port–Bradenton–Sarasota, FL – the most expensive Florida metro in this group – drew its largest share of net migration from the New York metro area, where home values are substantially higher.

The lone exception was Charleston–North Charleston, SC, whose largest source of net migration was Baltimore – a market with lower typical home values than the destination. Even in Charleston, however, affordability appears to have played a role. New York, a significantly more expensive market, ranked a close second in 2025, accounting for 6.5% of net positive migration into Charleston, just behind Baltimore’s 6.8%.

While housing costs are only one factor influencing migration decisions, the data suggests that households continue to gravitate toward markets where homeownership is comparatively more attainable than in the places they leave behind.

Most Top Migration Destinations Pull Residents From More Expensive Housing Markets

Typical Home Values* in Top Feeder Markets to Destination Hubs, 2025

Destination HubTop Feeder Market

*Typical home value based on Zillow Research’s Zillow Home Value Index (ZHVI) for Dec. 2024, immediately preceding the analyzed migration period (Jan.–Dec. 2025).

Share

Embed:

Major Insights:

Most high-growth metros attract residents from more expensive housing markets.

Relative affordability continues to be a primary driver of domestic migration.

Demographics Over Dollars

But as important as affordability is in explaining today’s domestic migration patterns, age appears to be an even stronger determinant of where people choose to relocate.

Among mid-sized and large metros (250K+ residents) experiencing significant population shifts – defined as gaining or losing at least 1.0% of their starting population through domestic migration over the past two years – households are increasingly moving toward older, more established communities.

The data reveals a clear negative relationship between migration performance and age differential – a metric calculated by subtracting the median age of the destination market from the weighted median age of its feeder markets. Negative values indicate movement toward older communities, while positive values indicate movement toward younger ones. In other words, the metros attracting the strongest migration inflows tend to be older than the markets sending them residents.

The data also shows a clear positive relationship between migration performance and retiree concentration. Metros with larger shares of residents aged 65 and older generally saw stronger migration gains over the past two years, while younger metros tended to attract fewer newcomers. This suggests that retiree-driven relocation has become an increasingly important driver of migration. At the same time, the influx of younger residents points to the broader appeal of these communities, which offer a mix of affordability, amenities, and lifestyle advantages.

Relocators are Gravitating Towards Older, More Established Communities – With Retirees Helping Fuel the Trend

Net Migration as Share of Starting Population, 2024–2025*

Net Migration vs. Weighted Age Differential

Net Migration vs. Share of Residents 65+

*Analysis includes metro areas with 250K+ residents and domestic migration gains or losses of at least 1.0% during the study period. Weighted Age Differential compares the destination market’s median age with the weighted median age of origin markets, with positive values indicating migration toward younger markets and negative values indicating migration toward older markets. Age data: Census ACS 2020–2024.

Share

Embed:

Major Insights:

People are moving to older, more established communities.

Markets with larger 65+ populations are attracting more domestic relocators.

The New Migration Map: Strategic Implications

The pandemic-era urban exodus is giving way to a more nuanced migration landscape. Large urban markets are stabilizing, while growth is increasingly concentrated in smaller states, secondary metros, and intra-state corridors. Affordability remains a powerful pull, but retirees, lifestyle considerations, and local market dynamics are also playing an increasingly important role in where Americans choose to live.

To capitalize on these shifts in 2026, civic leaders, commercial real estate (CRE) investors, retailers, and developers should:

Monitor smaller states gaining migration momentum. Among the nation's most populous states, only Florida saw (modest) net in-migration in 2025. By contrast, smaller states like South Carolina, Delaware, Idaho, Maine, Tennessee, and North Carolina continued to attract substantial inflow. Investors, retailers, and developers that monitor these patterns may be better positioned to identify emerging growth opportunities.

Invest ahead of growth. Vermont's reversal shows how important it is for housing supply and infrastructure to keep pace with demand. High-growth communities will also need the retail, healthcare, transportation, and service capacity required to support expanding populations.

Look beyond state-level narratives that can obscure local opportunities. Florida led the nation in fast-growing large metros even as Miami lost residents, while Texas saw Dallas gain momentum as Houston fell behind. Likewise, although Arizona was not a top destination state, Phoenix remained the nation's leading major metro for migration gains.

Treat states as migration ecosystems. In Florida, for example, domestic migration is increasingly redistributed across a network of interconnected metros – as costs rise in one market, residents shift to nearby alternatives. Tracking these spillover effects can help identify tomorrow's growth markets before they show up in the rankings.

Don't write off major urban markets. While New York, Los Angeles, and Miami continue to experience net outflows – and Chicago has yet to return to positive territory – migration losses have moderated substantially from their pandemic-era peaks. As these markets stabilize, investments in livability, affordability, and quality of life could help strengthen their long-term competitiveness and economic vitality.

Protect affordability as a competitive advantage. Across the nation's fastest-growing metros, migration flows continue to move from more expensive housing markets to less expensive ones. As demand rises, preserving attainable housing will be critical to maintaining the cost advantages that attract new residents and businesses.

Prepare for a retiree-driven demographic realignment. Older Americans are playing an outsized role in shaping domestic migration patterns, but the communities attracting them are increasingly appealing to a broader range of households as well. As these markets grow, demand is likely to increase for healthcare, recreation, hospitality, and housing, creating opportunities across a wide range of sectors.

Explore key signals guiding data-driven site selection from brands actively expanding their brick-and-mortar footprints.

May 21, 2026

Predicting The Next Best Location

Across segments, retail and dining expansions converge on a common set of priorities, including identifying markets with strong demand, ensuring alignment with target audiences, and leveraging local consumer behavior to drive synergy. Using AI-powered location intelligence, we analyzed five expanding brands and segments to uncover the core principles driving successful site selection.

1. Identifying Sustainable Growth in an Increasingly Saturated Market

Nationwide visits to coffee chains are up in 2026, with established brands and newcomers alike seeing their traffic increase as consumer headwinds lead some to shift their discretionary spend towards more affordable indulgences. But past visit growth does not necessarily indicate future opportunity – it may instead signal market saturation. Relying solely on overall visit trends to guide expansion could lead chains into highly competitive markets where existing supply already meets demand.

For example, analyzing traffic trends in 10 major metro areas where coffee visits increased year-over-year (YoY) in Q1 2026 reveals significant gaps between overall traffic trends and per-location demand. In some CBSAs, overall traffic growth significantly outpaced per-location traffic trends – suggesting that supply is already meeting (or exceeding) demand and limiting room for new coffee locations despite overall category growth. But in other metro areas, where overall visit growth appears smaller, per-location traffic is actually booming – indicating that the underlying demand is resilient enough to support additional coffee concepts.

These patterns highlight the importance of looking beyond topline growth to identify where true whitespace still exists.

Strategic Takeaways:

Relying solely on aggregate category performance can obscure regional white space. A market-level view may reveal opportunities for stronger returns in areas where consumer demand is gaining momentum.

Combining overall visit and visits per location data offers a more complete view of where demand is both strong and sustainable.

2. Ensuring Demographic Alignment on the Hyperlocal Level

Effective site selection matches both regional and local demographics to a brand’s target customer, supporting performance and reinforcing positioning. But even in well-aligned metros, results depend on site-level precision – locations where the trade area visitor profile most closely reflects the brand’s core audience are best positioned to drive incremental upside.

An analysis of Alo locations in the DC area suggests that the company is adopting this strategy. Within the already high-income metro area of Washington-Arlington-Alexandria, individual Alo Yoga stores are placed in centers that draw even more affluent visitors – maximizing the revenue potential of each location.

In fact, Alo's newest stores in the metro area – One Loudoun and Bethesda Row – drive traffic from households with higher median incomes than even the established area locations. This signals a clear focus on premium retail corridors and affluent consumer segments, which reinforces the brand’s positioning while capturing higher-spending customers at the site level.

Strategic Takeaways:

Beyond traffic potential, effective site selection requires a clear understanding of both regional and hyperlocal demographics, as well as the brand’s target audience.

As brands expand, aligning locations with core customer bases can drive success while reinforcing brand positioning.

3. Finding Retail Nodes With Complementary Visitation Patterns

Beyond driving traffic potential and demographic alignment, site selection should also ensure that a brand’s identity and operating model are well matched to the visitation patterns of prospective locations. Barnes & Noble offers a clear example. The company’s ongoing resurgence has relied in part on repositioning itself as a local cultural and social hub, with a stronger emphasis on local curation and community-driven events.

And analyzing Barnes & Noble’s 2026 openings shows a clear tilt toward centers with a higher share of local traffic than the chain average – supporting its shift away from a purely transactional retail model toward a more community-centric experience built around local curation, events, and repeat visitation. By prioritizing locally driven centers, the company’s site selection strategy not only captures relevant traffic but also reinforces its broader repositioning as a neighborhood-oriented brand.

Strategic Takeaways:

Site selection strategy should look to align a brand’s identity and operating model with real-world visitation patterns at prospective locations.

For brands leaning into local curation, choosing centers with predominantly nearby visitors may be the key to performance and preserving brand identity.

4. Understanding the Benefits of Competitor Proximity

Effective site selection recognizes that proximity to competitors can function as a demand driver, amplifying traffic rather than diluting it.

In practice, this often takes the form of clustering – deliberately locating near similar or complementary concepts to capture shared demand. Shake Shack provides a clear example. Analyzing the chain's store fleet shows that many locations sit near other QSR and fast-casual concepts, creating opportunities to capture dining-based traffic. At the same time, strong cross-visitation patterns indicate that these co-located brands share a common customer base, positioning the brand closer to consumers who are already likely to visit. And, at least for Shake Shack, this strategy appears to be working – traffic to the chain increased 19.9% YoY in Q1 2026.

Strategic Takeaways:

As in retail, co-tenancy in the restaurant space can be mutually beneficial – establishing a center as a dining destination, driving incremental traffic, and increasing a brand’s opportunities to win share-of-stomach.

Incorporating cross-visitation analysis into site selection helps pinpoint locations where target customers are already visiting nearby brands. Centers that already attract a brand’s overlapping customer base provide a stronger foundation for incremental growth.

5. Balancing Growth and Cannibalization Risk

Incorporating trade area analysis into site selection can also help determine whether a new location will generate new traffic or risk cannibalizing existing demand. Aldi, a rapidly expanding grocery chain, offers a relevant example.

The company opened a fourth Las Vegas store on S Decatur Blvd in October 2025, positioned between existing locations on W Craig Rd and S Rainbow Blvd, approximately eight miles from each. And analyzing the core trade area of each of the four Las Vegas locations indicated limited visitor cannibalization over the last six months, despite the stores’ close proximity. Only 6.2% and 7.6% of the S Decatur Blvd store’s trade area overlapped with the W Craig Rd and S Rainbow Blvd stores’ trade areas, respectively.

These findings show that there is no one-size-fits-all approach to store spacing – it varies by brand, category, and market. Analyzing a company’s existing store network alongside competitor density and overall demand can help determine how closely locations can be placed without hurting performance. In many cases – especially in high-frequency categories like grocery – markets can support stores that are closer together than expected.

Strategic Takeaways:

Site selection strategy needs to take into account local demand and visitation behavior typical of the category as a whole and of existing locations in particular.

Trade area analysis can reveal where a market allows for network densification without significant risk of visit cannibalization.

.svg)

.png)

.png)

.avif)