.svg)

Traffic Performance Reveals Divergent Growth Trajectories

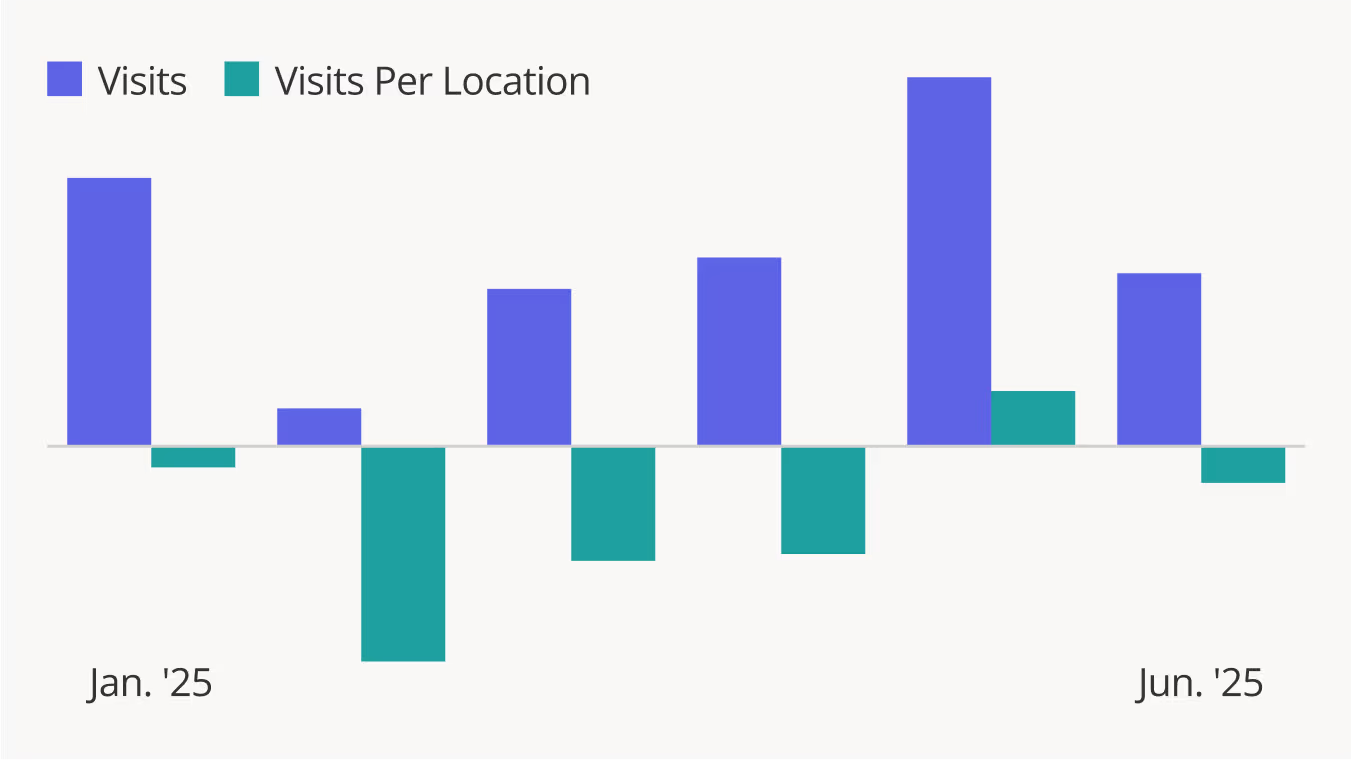

Shake Shack traffic increased an impressive 13.7% year-over-year (YoY) in Q2 2025 while average visits per venue held relatively steady at -1.7% – indicating that the chain's aggressive expansion strategy is capturing new market share without cannibalizing existing locations.

Meanwhile, although Q2 2025 visits to Wingstop were up 3.6%, the chain's average visits per venue declined 6.3% – which may suggest that discretionary dining brands serving lower-income consumers may be experiencing pressure from tightening household budgets.

Demographic Differences Between Wingstop & Shake Shack

Analyzing trade area demographic data reveals that Wingstop's captured market has a median household income of $69.5K – significantly lower than Shake Shack's $97.0K. Wingstop's trade area also includes a much higher proportion of households with children.

Wingstop attracts families with tighter budgets who must stretch their dining dollars further, which likely contributed to the decline in average visits per venue during this period of economic uncertainty. Meanwhile, Shake Shack's appeals to higher-income consumers with more discretionary spending power could explain the chain's impressive visit strength despite the ongoing headwinds.

Small Shifts in Visitor Loyalty

Looking at the change in visit frequency compared to 2024 also suggests that Wingstop is feeling the impact of its visitors' tighter budgets.

Wingstop still maintains a significant advantage in customer loyalty, with 16.8% to 18.1% repeat monthly visitors in H1 2025 compared to Shake Shack's 10.5% to 11.4%. But comparing these numbers to 2024 reveals that Wingstop's share of repeat visitors has declined slightly since 2024, while Shake Shack has posted modest monthly gains throughout H1 2025.

This shift suggests that budget-conscious families may be reducing their regular Wingstop visits to save money, while Shake Shack's strategic expansion is bringing locations closer to customers which could be driving increased repeat visitation.

Wingstop's Well-Positioned For Long-Term Resilience

Despite facing economic headwinds, Wingstop's continued positive visit growth and superior customer loyalty metrics demonstrate the brand's strong fundamentals and deep connection with its core family demographic.

As economic conditions stabilize, Wingstop's established customer base and proven appeal to budget-conscious families positions the chain for a strong rebound, particularly given that families with children represent a large and resilient market segment that will likely return to regular dining patterns when household budgets recover.

Visit Placer.ai/anchor for the latest data-driven dining insights.

Movie theater visits were up year-over-year in Q2 2025, but traffic generally remains significantly below 2019 levels – with the exception of Cinemark, where visits are almost on par with pre-pandemic levels. We analyzed the data to understand how movie-going behavior has changed since COVID and why Cinemark is staying ahead of the curve.

Year-over-Year Strength

Movie theater traffic jumped year-over-year (YoY) in Q2 2025 thanks to the release of several successful blockbusters, including A Minecraft Movie, Sinners, Lilo & Stitch, and Mission Impossible: The Final Reckoning.

Movie Visits Lag Pre-COVID Levels – But Cinemark Bucks the Trend

Still, baseline movie theater attendance remains significantly lower than it was pre-pandemic. And although YoY trends for AMC, Regal, and Cinemark were relatively consistent, comparing these chains' recent visit trends to pre-pandemic traffic reveals major differences in long-term performance.

Between July 2024 and June 2025, visits to the two largest chains – AMC and Regal – were 33.2% and 40.0% lower, respectively, than they were between July 2018 to June 2019. The visits per location gap was slightly narrower – due to rightsizing efforts that consolidated traffic into fewer movie theaters – but the data still indicates that AMC and Regal theaters are generally emptier than they were in 2018-2019.

But bucking the trend is Cinemark, which saw traffic to its flagship Cinemark brand dip just 2.6% compared to pre-COVID, while average visits per location were relatively stable at -0.8%. Thanks to this impressive recovery, Cinemark has significantly strengthened its position in the wider movie theater landscape.

Cinemark's Fuller Theaters

A deeper look at the data confirms Cinemark's success in attracting moviegoers. Cinemark theaters average more visits both per location and per square foot, indicating that their higher visit numbers stem from fuller theaters rather than larger venues or more locations.

Blockbusters Playing Larger Role in Driving Movie Visits

But just because Cinemark's visit numbers are relatively aligned with 2018-2019 traffic levels does not mean that the chain has not been impacted by the shift in post-COVID movie-going behavior.

Comparing monthly visits between July 2018-June 2019 and July 2024-June 2025 reveals increased traffic volatility at all three chains, with higher peaks and deeper valleys compared to average monthly baselines. This volatility likely stems from blockbusters playing a more central role in driving movie visits. Fewer consumers now go to movies casually – instead, they save their limited movie budgets for major releases.

The data also shows that all three chains have seen a relative drop in visits to matinee screenings (before 5 PM) along with a relative increase in late-night visits (9 PM to 1 AM) – which could also be consistent with a more intentional and less casual movie-going pattern.

And Cinemark hasn't been immune to these changes. The chain has also experienced similar monthly visit volatility, fewer matinee visits, and more late-night visits – matching the patterns seen at AMC and Regal.

Cinemark's Success – Less Affluent, More Family-Friendly Visitor Base

So what is driving Cinemark's success? Some of the answer may lie in its strategic focus on less affluent family audiences. Compared to AMC and Regal, Cinemark attracts visitors from areas with lower median household incomes and higher concentrations of families – a positioning the chain seems to be deliberately cultivating.

Cinemark has built an ecosystem designed for budget-conscious families: their Movie Club membership includes monthly rollover ticket credits and concession discounts, while their Summer Movie Clubhouse offers discounted family packages. Select locations also feature Camp Cinemark auditoriums – screening rooms specifically designed to be child-friendly.

This strategy creates a virtuous cycle. While Cinemark's lower-income audience has tighter entertainment budgets, they're also less likely to have premium home theater setups that compete with the theatrical experience.

When these families do decide to splurge on entertainment, Cinemark's value-oriented approach and family-friendly amenities make it the logical choice – turning occasional visits into a more loyal customer base that sustains traffic even during industry-wide downturns.

Cinemark Highlights Path to Success for Movie Theaters

While most movie theater chains continue to struggle with significantly lower attendance compared to pre-pandemic levels, the strong YoY performance suggests that the movie theater recovery story is still being written. Cinemark's success demonstrates that chains willing to adapt their strategies to serve underserved audiences can not only survive but thrive in the transformed post-pandemic entertainment landscape.

For more data-driven consumer insights, visit placer.ai/anchor.

Major retailers held promotional events around Amazon's Prime Day sales event. How did the promotional events impact retail foot traffic? And what does the data reveal about the state of consumers going into the second half of 2025?

July Promotional Events Mostly Boosted Mid-Week Visits

Comparing daily visits to major retailers during their July campaigns against same-day YTD averages (e.g., Sunday July 6th traffic versus average Sunday visits in 2025) reveals that sales primarily boosted weekday traffic. Visits increased Monday through Friday during the promotional periods, but every retailer that extended its campaign to Saturday – typically the busiest in-store shopping day – experienced traffic declines compared to YTD Saturday averages.

Individual retailer analysis shows Best Buy achieved the strongest response, with visits increasing 13.2% to 21.9% between July 7th and 11th compared to same-day YTD averages, and the final day (Sunday July 13th) posting a 7.2% increase. Conversely, Dollar General saw the weakest performance – only three of seven promotional days generated visit increases, all remaining in low single digits.

This pattern suggests consumers leveraged sales for big-ticket purchases at discounts but didn't use the opportunity to stock up on lower-priced items.

Generally Lower YoY Visit Numbers

Comparing average daily visits during 2024 and 2025 July campaigns shows generally lower in-store traffic this year. Timing likely played a role – except for Best Buy, all analyzed retailers ran their 2024 campaigns before Amazon Prime Day, while this year all five overlapped with Amazon's event. This means that, unlike in 2024, Target, Walmart, Kohl's, and Dollar General directly competed with Amazon Prime Day in 2025, potentially driving the in-store traffic decline.

This calendar shift makes Walmart's performance particularly noteworthy. Average daily visits during "Walmart Deals" increased 8.9% compared to last year – despite facing direct Amazon competition for the first time.

Walmart's strength may stem from its recent "Who Knew?" advertising campaign, which may have kept the retailer top-of-mind for many customers during this period of intense retail competition.

The YoY visit growth during July campaigns represents another milestone in the company's turnaround and brand refresh, demonstrating the legacy retailer's continued relevance in today's competitive retail landscape.

The data reveals that consumers approached July 2025 promotional events with strategic intent, focusing on high-value purchases during convenient weekday shopping windows rather than impulse buying across all categories.

Walmart's standout performance amid increased competition suggests that strong brand messaging and strategic positioning can overcome market headwinds, providing optimism for retailers heading into the second half of 2025.

For more data-driven retail insights, visit placer.ai/anchor.

McDonald's recent re-introduction of the snack wrap joins the recent wave of nostalgia-driven menu innovations – and initial data suggests that the fan-favorite is already driving up visits to the chain. On July 10th – the day of the launch – McDonald's traffic nationwide was up 15.0% compared to the 2025 YTD daily average and 11.4% higher than the YTD Thursday average, and visits remained high on Friday and Saturday as well.

The Snack Wrap's return comes at a critical time for McDonald's, as the chain continues to lean on menu innovations to turn around its recent traffic plateau plateau and sales dips.

Will the initial excitement translate into a sustained visit hike?

Visit placer.ai/anchor for the latest data-driven dining analysis.

.avif)

JOANN's Demise Likely Not Due to Lack of Demand

Following years of volatility and multiple bankruptcies filings, JOANN – the 82-year-old fabric and craft retailer – shuttered its final stores in May 2025, with many stores already closing in April 2025. But diving into traffic trends for some of JOANN's competitors suggest that JOANN's bankruptcy and ultimate closure was not necessarily the result of lowered demand for crafting supplies.

Year-over-year (YoY) visit trends to JOANN stores were mostly stable prior to the closure announcements, and traffic skyrocketed as consumers descended on the bargain-priced fabrics and sewing supplies during the chain's liquidation sales. And since the closures, visits to other crafting retailers has skyrocketed, with traffic to Michael's – JOANN's main competitor that even bought chain's intellectual property – up 9.2% YoY in June 2025.

What Brought JOANN & Party City Down?

JOANN is not the only hobby and crafts chain to go bankrupt over the past twelve months – Party City, which had filed for bankruptcy in 2023, also shut its last remaining stores in February 2025. And though Party City's main focus may have been party supplies, the retailer also carried an assortment of arts and crafts supplies. This means that in H1 2025 two craft-forward legacy retailers permanently shut down.

So what brought JOANN and Party City down? While several factors contributed, one significant challenge faced by both companies was their size. Although JOANN had a loyal following in some circles, the retailer's brick-and-mortar footprint was relatively moderate – in 2024, JOANN received less than half as many visits as Michaels, due in part to its significantly smaller store fleet. Party City was even smaller, receiving less than half the visits going to Hobby Lobby last year.

This means that Party City and JOANN likely lacked the economies of scale and marketing dominance of the Hobby Lobby and Michaels – making it harder to stay afloat in an increasingly competitive market. And Party City and JOANN's mid-size brick-and-mortar footprint likely also made it more difficult to compete with mass merchants such as Walmart and Target.

How Did Blick Emerge Unscathed?

But if the market consolidation forces of recent years drove JOANN and Party City out of business – what to make of the endurance of tiny Blick and its 0.3% visit share? The answer to that may lie in another trend. The bifurcation of consumer spending since COVID has sustained demand for premium, quality brands and products alongside significant growth for value-oriented retail chains. And looking at the trade area median household income for the five analyzed chains highlights Blick's affluent visitor base – and suggests that the chain has successfully positioned itself as a premium purveyor of quality arts supply.

This in turn allows Blick to operate in a wholly different field where it is not competing directly with the Hobby Lobbies (or Walmarts) of the world. Instead, it has carved out a defensible niche where the defining competitive metric isn't price, but the quality and curation of its products.

The divergent paths of JOANN and its competitors highlight the new realities of the craft retail market, where operating without the scale of a Michaels or the premium, defensible niche of a Blick can create a significant liability.

For more data-driven retail insights, visit placer.ai/anchor.

Office supplies behemoth Staples has faced a challenging few years, contending with stiff competition from online rivals and evolving office visit trends that have reduced demand for some of its core products. Consumer cutbacks in discretionary spending driven by recent inflationary pressures have also taken their toll on the retailer, which has closed dozens of stores over the past several years.

But by remaining agile and pivoting towards services and B2B offerings, Staples has defied expectations – showing how retailers can succeed by staying in tune with shifting consumer needs and habits. We dove into the data to explore Staples’ recent visit growth and some of the factors behind its current success.

That Was(n’t so) Easy!

Last month, Staples brought back its iconic “That Was Easy!” button, highlighting the chain’s mission to simplify customers’ lives through products and solutions. But though Staples’ impressive traffic resurgence might appear to have been effortless, its current growth is the result of a carefully orchestrated pivot towards meeting the practical demands of shoppers in 2025.

In addition to its staple (pun intended) office and school supplies, Staples is ramping up its business-focused services. The chain recently began a pilot with Verizon to expand its tech offerings – with the explicit purpose of offering the telecom giant access to more small business visitors. The company has also expanded its onsite services, offering everything from print-while-you-wait to travel-related options like passport photos.

And a look at Staples’ foot traffic over the past several months shows these efforts are paying off. Since January 2025, visits and average visits per location to Staples have been consistently elevated year over year (YoY), with the sole exception of February, when retailers across categories were impacted by stormy weather and the comparison to a leap year. And as the year has worn on, Staples’ visitation trends have only gotten stronger, with June seeing a 10.3% increase in overall foot traffic and a 13.2% increase in average visits per location compared to 2024.

Traffic Surpasses Pre-COVID Levels

Despite the challenges of the past several years – and the closure of dozens of stores since 2019 – Staples’ foot traffic is also now higher than it was pre-COVID. In Q2 2025, overall visits to the chain exceeded Q2 2019 levels by 5.6%. And each open store is seeing far more foot traffic than it did before the pandemic, with average visits per location rising by 23.9% over the same period.

A Pivot to Services and B2B

Location analytics reinforce the notion that it is Staples’ pivot to services and B2B solutions that is largely fueling this comeback.

August, for example, has traditionally been Staples’ busiest month of the year, as students and families descend on the chain to stock up on back-to-school supplies. But in recent years, the month has become less of an outlier, with traffic spread more evenly across the calendar.

Moreover, the number of frequent visitors to Staples – i.e. those who return to the chain multiple times per month – has grown steadily since 2019. Between H1 2019 and H1 2025, the share of customers visiting Staples at least twice a month on average edged up from 12.0% to 12.8%, and the proportion of those making three or more monthly visits climbed from 3.5% to 4.9%. This shift points to a consumer base increasingly reliant on Staples for ongoing needs rather than episodic purchases.

Stepping Up to Meet New Demands

Staples’ recent visit success sheds light on the power of pivoting to meet shifting consumer demands. By emphasizing services and leaning into B2B offerings, Staples has transformed itself into a go-to destination for new audiences – reinforcing the importance of adaptability and innovation in retail.

For more data-driven retail analyses, visit Placer.ai/anchor.