.svg)

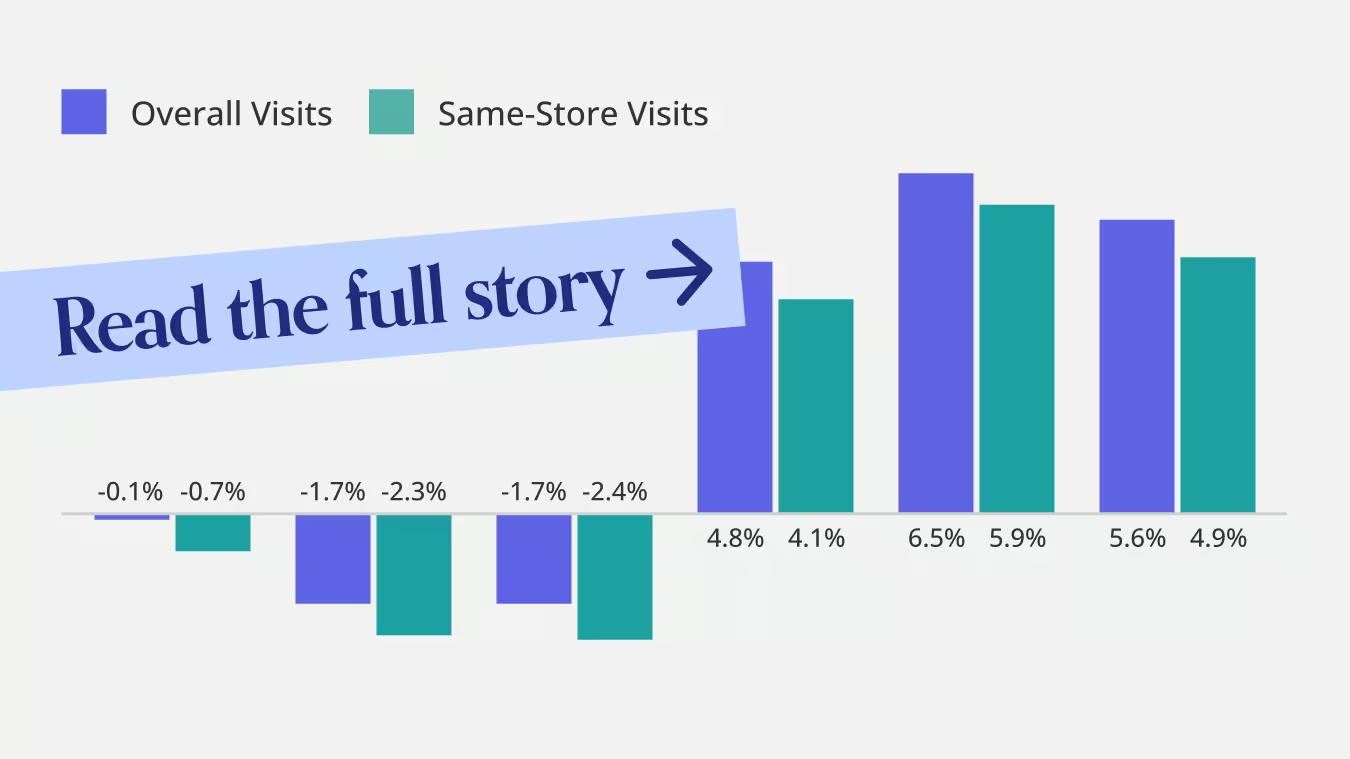

McDonald’s Builds Visit Momentum Heading Into 2026

McDonald’s ended 2025 with clear visit momentum, reversing earlier softness and posting steady gains in the back half of the year. Same-store visits followed a similar trajectory, indicating that growth was driven by stronger underlying demand rather than unit expansion. This late-year rebound positions McDonald’s with solid visit momentum heading into 2026, suggesting improving consumer engagement as the year closed.

Higher-Frequency Diners Drive McDonald’s Visit Growth

Some of the visit growth is likely due to the chain's popular Q4 LTOs – but diving deeper into the visit frequency data suggests that McDonald’s long-term investment in its loyalty program is also playing a part. The company's launch of MyMcDonald’s Rewards in 2021 seems to have succeeded in shifting traffic toward higher-frequency, incremental visits rather than relying on new customer acquisition.

Compared to pre-loyalty levels in H2 2019, a growing share of McDonald’s visits now comes from diners visiting an average of 4+ times per month, with the share of visits from consumers visiting the chain an average of 8+ times per month showing the most dramatic growth. Grouping YoY visit trends by visit frequency also shows that visits from high-frequency diners grew the most compared to H2 2024 and H2 2019. This dynamic points to a core benefit of loyalty-led growth: driving incremental visits from existing customers is typically far more efficient than acquiring new ones, especially in a mature, highly penetrated category like quick service restaurants.

McDonald’s executives have been explicit that loyalty is designed to increase frequency, not just enrollment. The continued growth of the program through 2025 – including deeper integration with value offers and digital ordering – suggests McDonald’s is still finding room to extract incremental visits from an already loyal base.

What McDonald’s Loyalty Strategy Signals for Other Restaurant Chains

For other restaurant chains, McDonald’s experience points to the value of using loyalty as a lever for incremental growth, particularly once a customer has already been acquired. While many QSR brands continue to drive expansion by entering new markets or opening additional locations, McDonald’s data illustrates how meaningful gains can also come from increasing visit frequency among existing customers. Even without McDonald’s scale, the underlying strategy is broadly applicable: converting first-time or occasional visitors into higher-frequency customers can serve as a complementary – and often more efficient – path to growth alongside physical expansion.

Will these lessons shape the QSR space in 2026? Visit Placer.ai/anchor to find out.

Placer.ai leverages a panel of tens of millions of devices and utilizes machine learning to make estimations for visits to locations across the US. The data is trusted by thousands of industry leaders who leverage Placer.ai for insights into foot traffic, demographic breakdowns, retail sale predictions, migration trends, site selection, and more.

Lessons From Dollar Tree's 99 Cents Only Acquisition

In 2024, Dollar Tree capitalized on the liquidation of the 99 Cents Only chain to execute a strategic "land grab" in the notoriously tight US retail market. By acquiring designation rights for 170 leases across priority markets like California, Arizona, Nevada, and Texas, the retailer aimed to bypass zoning hurdles and accelerate growth.

AI-powered location analytics indicates the selection process was highly disciplined: Looking at over 85 California stores that were converted from 99 Cents Only to Dollar Tree reveals that Dollar Tree cherry-picked high-performing sites that were generating 6.0% more foot traffic than the 99 Cents Only chain average in 2023. This suggests the acquisition was a calculated move to secure proven, high-quality real estate.

Beware of Cannibalization

However, 2025 performance data reveals that capitalizing on this opportunity comes with distinct operational costs. Total visits to the converted stores have dropped 38.8% compared to their 2023 baselines. While some of this decline is structural – Dollar Tree operates a lower-frequency "treasure hunt" model compared to the high-frequency grocery model of the previous tenant – a significant portion is self-inflicted through network overlap.

A staggering 36% of the new sites are located less than a mile from an existing Dollar Tree, which inevitably dilutes local traffic through cannibalization. This serves as a critical lesson for retailers considering bulk acquisitions: purchasing a portfolio "en masse" often prevents perfect network optimization, forcing the acquirer to manage the friction where new footprints compete with the old.

A "Healthy Correction"

Still, despite this cannibalization and the drop in raw volume, the transition offers a potential "healthy correction" for the business. The previous tenant collapsed under the weight of "rising levels of shrink" and low-margin grocery sales. By shifting the model, Dollar Tree is effectively filtering out non-paying visitors and low-value transactions, trading chaotic volume for a more controlled, margin-focused operation. The discrepancy between the sharp drop in total visits (-38.8%) and the more moderate dip in visits per square foot (-25.0%) suggests Dollar Tree is already rightsizing these operations, leaving some "ghost space" inactive rather than over-investing in labor to manage the entire cavernous floor.

Increasingly Affluent Dollar Tree Audience Key to New Stores' Success

And this excess square footage is only a liability if it remains empty; turning it into an asset requires leveraging the fundamental change in who is now shopping these aisles. The shift in shopper demographics – where "Wealthy Suburban Families" have replaced the "Young Urban Singles" and "Melting Pot Families" of the previous tenant – is crucial for Dollar Tree's future. This new audience, which is less price-sensitive, provides the ideal environment for Dollar Tree to deploy its "Multi-Price" strategy.

While CFO Jeff Davis has cited "start-up costs" regarding these conversions, the long-term opportunity is clear: if Dollar Tree can utilize the extra square footage to showcase this higher-margin assortment, these locations could evolve from overlapping burdens into profitable flagships that capture a share of wallet the traditional small-box fleet never could.

For more data-driven CRE insights, visit placer.ai/anchor.

Placer.ai leverages a panel of tens of millions of devices and utilizes machine learning to make estimations for visits to locations across the US. The data is trusted by thousands of industry leaders who leverage Placer.ai for insights into foot traffic, demographic breakdowns, retail sale predictions, migration trends, site selection, and more.

.avif)

Indoor Malls Led On a Full-Year Basis, Open-Air Outperformed Over the Holidays

Indoor malls outperformed both open-air centers and outlet malls on a full-year basis as the only format to post visit gains during all four quarters – signaling a shift from recovery into growth.

Open-air shopping centers came in second – and though the format trailed indoor malls on a full-year basis, open-air shopping centers came out on top over the holidays, with Q4 visits up 2.0% year over year (YoY) and December traffic up 1.5%. This seasonal strength can be attributed to the format's sit-down and alcohol-forward dining options, which attract social holiday visits, as well as layouts that support quick trips and easy access to both essential and discretionary retail.

Meanwhile, outlet malls remained the weakest-performing format throughout 2025, with an annual traffic decline driven in part by a 1.1% drop in visits during the critical holiday season. This softness could reflect a broader shift in value perception. Price-conscious consumers may be increasingly weighing time cost alongside monetary savings, and long drives can offset the appeal of discounted pricing – particularly when promotions and loyalty incentives are widely available online and in traditional retail formats. To win consumers back, outlet malls may need to reduce the perceived time tradeoff by strengthening food and entertainment offerings and positioning themselves as curated, experience-driven value destinations rather than purely price-led ones.

Families Lead Mall Visitation

Malls continue to resonate with a wide range of family segments, though different formats appeal to different household profiles. Across formats, higher-income and suburban family segments over-index among mall visitors. Indoor malls and open-air centers attract a disproportionate share of ultra-wealthy and affluent suburban households, underscoring malls’ ongoing relevance for consumers seeking family-friendly activities and experiences. Outlet malls, meanwhile, skew more heavily toward near-urban diverse families, reflecting their positioning as value-oriented destinations rather than lifestyle hubs.

At the same time, young professionals also play a meaningful role in mall traffic, over-indexing across all formats relative to their 5.8% share of the national population.

Malls Compete Within Broader Shopping Ecosystems

Across all formats, mall visitors also frequented mass merchants, big-box retailers, and off-price chains at high rates in 2025, underscoring that mall trips are often embedded within broader, multi-stop shopping routines rather than standing alone.

More than 70% of visitors across all mall formats also visited Walmart and Target at some point in 2025, and over half of mall visitors also visited Dollar Tree – underscoring how deeply mass merchants and discount chains are embedded in consumers’ retail lives. This indicates that malls face stiff competition as an everyday shopping destination. Malls that want to pull ahead in 2026 may focus on differentiating themselves from superstores by leaning into experiences and services that mass merchants cannot efficiently deliver – using tenant mix and programming to capture discretionary spend beyond routine retail needs.

Of the three formats, outlet malls showed the highest overlap with value-oriented and off-price chains, highlighting both their competitive pressure and their opportunity to redefine value. As discounted retail becomes increasingly ubiquitous, outlets can differentiate by extending value beyond merchandise—pairing sharp pricing with affordable dining, family-friendly entertainment, and experience-led programming that reinforces the outlet trip as a high-value day out, not just a bargain hunt.

Maximizing Visit Quality Across Mall Formats in 2026

Mall success in 2026 will likely hinge on maximizing the quality and purpose of each visit. Indoor malls are best positioned to double down on experiential retail, entertainment, and family-friendly programming that supports longer dwell times and higher discretionary spend. Open-air centers can continue to capitalize on convenience and dining-led visitation by optimizing for short, high-intent trips – particularly during peak seasonal periods.

For outlet malls, the opportunity lies in expanding the definition of value. As discounts become easier to access everywhere, outlets can differentiate by applying value thinking to food, entertainment, and experiences – turning the outlet trip into an affordable day out rather than a pure bargain hunt. Across all formats, operators and retailers that align tenant mix, layout, and programming with how consumers actually shop – across channels and formats – will be best positioned to capture wallet share in an increasingly fragmented retail landscape.

For more data-driven retail insights, visit placer.ai/anchor.

Placer.ai leverages a panel of tens of millions of devices and utilizes machine learning to make estimations for visits to locations across the US. The data is trusted by thousands of industry leaders who leverage Placer.ai for insights into foot traffic, demographic breakdowns, retail sale predictions, migration trends, site selection, and more.

Holiday 2025 Delivered Broad-Based Traffic Growth

Despite the ongoing consumer headwinds, the 2025 holiday shopping season delivered year-over-year (YoY) gains for both retail and dining chains nationwide, with the majority of states registering retail and dining traffic increases during the holiday window. And while performance varied meaningfully by category and format, aggregate retail traffic numbers point to significant consumer engagement throughout the end of 2025.

Bifurcation Defined Holiday Apparel Performance

Bifurcation has been a defining trend of consumer behavior in 2025 and continued to shape shopping patterns during the holiday season. Thrift stores and off-price retailers led the apparel category with traffic up 11.7% and 6.6% (November 1st to December 24th, 2025), respectively, compared to last year’s holiday period. Luxury chains and department stores also posted modest gains (+1.8%), while traditional apparel chains saw slight declines (-1.8%) and mid-tier department stores experienced more pronounced traffic drops (-6.2%).

Experience-Forward Open-Air Centers Outperformed Other Mall Formats

Open-air shopping centers led mall-format performance during the 2025 holiday season, with visits up 1.7% YoY, as consumers gravitated toward environments that offered a more festive, experiential atmosphere and a wider mix of dining options. The format likely received an additional lift from warmer-than-average weather across much of the country, which encouraged shoppers to fully take advantage of the outdoor amenities and social experiences open-air centers offer during the holidays.

Indoor mall traffic was largely flat (+0.8%) – a positive signal given ongoing consumer headwinds, especially for mid-tier formats – suggesting that traditional malls were able to maintain relevance during a pressured spending environment.

Meanwhile, outlet mall visits declined slightly (-0.8%), likely reflecting reduced appetite for destination-driven, discretionary trips as shoppers prioritized convenience, everyday value, and locally accessible retail over longer, deal-oriented excursions during the holidays.

Value – Beyond Just Low Prices – Won in the Superstore Space

Within the superstore category, wholesale clubs and discount & dollar stores outperformed mass merchants. This performance underscores consumers’ continued shift toward value-driven retail during the holidays and highlights that “value” extends beyond low prices alone; wholesale clubs, with their compelling value propositions, are also seeing meaningful gains in the current consumer environment.

Self-Gifting Categories Outpaced Traditional Holiday Segments

Categories most closely tied to self-gifting outperformed more traditional holiday segments during the 2025 season. Pet stores and services (+5.5% YoY) and home improvement retailers (+3.4% YoY) led the way, perhaps because purchases from these categories are typically positioned as practical investments in everyday life, ranging from caring for pets to improving and maintaining living spaces.

In contrast, home furnishings (-0.8%) lagged, as these purchases tend to be more decorative or occasion-driven and therefore more likely to be intended as gifts for others rather than immediate, utility-focused upgrades. Traffic to electronics stores also dipped slightly (-1.5%). Together, these trends underscore a consumer preference for spending that delivers direct, everyday value to themselves over more traditional, outward-facing holiday gifting.

What the 2025 Holiday Season Reveals About the 2026 Consumer Mindset

Overall, location analytics for the 2025 holiday season suggest that consumers remained highly engaged despite ongoing economic pressure, but their spending behavior continued to fragment. Across apparel, superstores, and discretionary categories, shoppers consistently gravitated toward retailers that delivered clear value – whether through low prices, strong quality-to-price ratios, or products tied to personal utility and well-being. The outperformance of thrift, off-price, wholesale clubs, and self-gifting categories underscores a consumer mindset that is both pragmatic and selective, balancing budget consciousness with targeted willingness to spend.

Looking ahead to 2026, these patterns suggest that retailers should move beyond one-dimensional value messaging and instead sharpen their core propositions. Formats that clearly articulate why they are “worth the trip” – through pricing power, assortment differentiation, or alignment with everyday consumer priorities – will be best positioned to win share. As bifurcation persists, success will increasingly depend on understanding which consumer needs a brand serves best and doubling down on those strengths, rather than attempting to compete broadly across a squeezed and highly segmented retail landscape.

For more data-driven consumer insights, visit placer.ai/anchor.

Placer.ai leverages a panel of tens of millions of devices and utilizes machine learning to make estimations for visits to locations across the US. The data is trusted by thousands of industry leaders who leverage Placer.ai for insights into foot traffic, demographic breakdowns, retail sale predictions, migration trends, site selection, and more.

With budgets stretched and food inflation lingering, many dining concepts assume that value – specifically, a compelling price-per-food-item ratio – is the key to driving traffic in 2025. And this approach may work: chains like Chili's have shown that an array of deals – such as the 3 For Me and the Triple Dipper Deal – has helped the casual dining brand significantly outpace the wider dining category for more than a year.

But looking at recent QSR traffic trends suggests a more nuanced story. At both McDonald’s and Burger King, the strongest visit lifts in recent months came from experiential promotions and culturally resonant LTOs – not from discounts.

Boo Buckets & The Grinch Meal Outperform Extra Value Meals

McDonald’s reintroduced its Extra Value Meals on September 8, 2025 – but despite substantial promotional support, the rollout produced only a modest uptick in visits that week. And while traffic improved slightly in the weeks that followed, analyzing recent foot traffic trends highlights that the real inflection points came from experiential activations.

The return of Monopoly, which gave registered app users the chance to win prizes ranging from free food to high-value rewards, sustained elevated visits for weeks through gamification. Boo Buckets sparked a Halloween-season surge driven by nostalgia and collectability and drove a 10.8% increase in weekly visits compared to the January to August weekly visit average. And The Grinch Meal generated the strongest spike of the entire period by tapping into holiday IP and playful packaging. This data highlights that while consumers may appreciate affordability, moments that feel fun, shareable, and culturally relevant may sometimes be more effective at bringing them through the door.

LTOs Outperform Deal Weaks at Burger King

Burger King’s recent performance shows a similar pattern. The rollout of the limited-time Monster Menu generated a stronger visit lift than either Treat Week or Perks Week, both of which focused on giveaways and discounts. The debut of the chain’s nearly $20 Advent Calendar also outperformed Treat Week and Perks Week, underscoring how novelty and excitement may have a greater impact than price-based incentives.

And the strongest surge came with the debut of the SpongeBob Menu, which produced the strongest spike of the entire period and pushed weekly visits well above the January to August average. By pairing a beloved character franchise with themed packaging, kids’ meal tie-ins, and a sense of occasion, Burger King tapped into the same emotional drivers fueling McDonald’s biggest wins.

Designing Value for 2026: Different Playbooks for QSR and Full-Service Chains

While price sensitivity will likely continue to influence dining decisions in 2026, recent QSR data underscores an important point: Consumers may be watching their wallets, but price alone doesn’t determine where they choose to eat. Chili’s success shows that a compelling value platform can be a powerful differentiator in full-service dining, where the experience is already baked into the visit. But the same strategy doesn’t automatically translate to the QSR landscape, where affordability is expected and price-based promotions quickly blur together.

Consumers still care about value – but value now spans both price and experience. For full-service restaurants, this means leaning harder into the affordability side of that equation. With ambiance, service, and hospitality already part of the offering, emphasizing everyday value or reliable deal structures may help guests justify dining out more often.

For QSR brands, the calculus is different, and price alone may not be enough to unlock meaningful incremental traffic. Instead, traffic data shows that the strongest results in the QSR space come from experience-driven LTOs, cultural tie-ins, and moments that feel fun, collectible, or social. In other words, fast-food chains may need to focus less on matching grocery-store economics and more on delivering the kind of excitement consumers simply can’t get at home.

As budgets remain tight and expectations continue to evolve, the brands that win won’t be those that chase the lowest price – but those that understand how to deliver the right kind of value for their category: affordability where it matters, and memorable experiences where it counts.

For more data-driven insights, visit placer.ai/anchor.

Placer.ai leverages a panel of tens of millions of devices and utilizes machine learning to make estimations for visits to locations across the US. The data is trusted by thousands of industry leaders who leverage Placer.ai for insights into foot traffic, demographic breakdowns, retail sale predictions, migration trends, site selection, and more.

Early November Momentum Sets the Tone

Prior to Black Friday, mall visits across the three formats (indoor malls, open-air shopping centers, and outlet malls) were running comfortably ahead of 2024 levels. But during the week of Black Friday 2025, visits to indoor malls and open-air centers flattened or even dropped year over year – suggesting that many shoppers had moved their trips to earlier in November, when mall retailers had begun rolling out early Black Friday promotions.

Softer Black Friday Weekend Activity on Saturday and Sunday

A closer look at daily traffic across the Black Friday weekend reveals how this shift played out. Friday performed well across all formats, with indoor mall visits rising 3.1% year over year, open-air centers up 1.7%, and outlet malls essentially flat but still slightly positive. But Saturday and Sunday traffic declined YoY, weighing down on Friday's gains and pulling the whole week into negative YoY territory.

So Friday retained its status as the high-impact day, but the rest of the weekend showed signs of promotional fatigue – or simply that shoppers had already taken advantage of the deals they wanted.

If visit counts capture one dimension of consumer behavior, dwell time reveals another. The share of visits lasting more than an hour declined across all mall formats relative to last year, indicating a more mission-driven shopper – someone who arrives with a plan, moves efficiently, and heads on to the next task. The trend may also hint at a strategic shift: some consumers may have used earlier November visits to scout specific items or sizes, allowing them to streamline their Black Friday trips and focus on securing the best deals both inside and outside the mall.

Early Engagement Carries November Across the Finish Line

Most importantly, a broader look at year-over-year monthly visits shows that the early surge in November traffic more than offset the softness during Black Friday week, ultimately providing November 2025 with an overall YoY traffic boost. This pattern suggests that the holiday season’s momentum is becoming less dependent on a single weekend and increasingly shaped by how effectively retailers engage shoppers throughout the month – and the longer holiday season as a whole.

Implications for Holiday Retail

Black Friday mall data suggests that consumers are still engaging deeply with physical retail, yet the cadence of that engagement is evolving. They are starting earlier, concentrating their in-person activity in shorter bursts, and reserving their longest visits for fewer occasions. For retailers, this dynamic underscores the importance of capturing Friday’s surge, aligning promotions with earlier November interest, and offering experiences compelling enough to draw shoppers back later in the weekend. For landlords, the data highlights opportunities to support purposeful shopping with frictionless navigation, efficient operations, and programming that encourages dwell at moments when the natural impulse may be to move quickly.

As December data comes into view – from Super Saturday to the final week before Christmas – the key question will be whether these patterns continue or whether late-season urgency reshapes the curve once again. For now, the early read is clear: shoppers are showing up, but on their own terms, and malls that adapt to this more intentional consumer are positioned to capture the strongest returns.

For more data-driven consumer insights, visit placer.ai/anchor.

Placer.ai leverages a panel of tens of millions of devices and utilizes machine learning to make estimations for visits to locations across the US. The data is trusted by thousands of industry leaders who leverage Placer.ai for insights into foot traffic, demographic breakdowns, retail sale predictions, migration trends, site selection, and more.