.svg)

Just as the dining space was beginning to recover from the COVID pandemic, the ongoing inflation brought a fresh set of challenges to the sector in 2022 and 2023. How did the headwinds impact Burger King, Popeyes Louisiana Kitchen, Taco Bell, KFC, and other leading brands from the RBI and Yum! Portfolio? We dove into the data to find out.

RBI & Yum! 2023 Foot Traffic Recap

Restaurant Brands International (RBI) and Yum! Brands each own three QSR banners along with one fast-casual chain. RBI owns the Burger King, Popeyes Louisiana Kitchen, and Tim Hortons brands as well as fast-casual sub chain Firehouse Subs. Yum! Brands operates the KFC, Pizza Hut, and Taco Bell fast-food banners and the fast-casual The Habit Burger Grill.

Both companies’ banners saw year-over-year (YoY) growth in Q1 2023, likely aided by favorable comparisons to an Omicron-plagued Q1 2022. And although traffic dropped off as the year went on – perhaps due to consumers cutting back on dining out – the dip was subdued, with visits staying relatively close to 2022 levels.

RBI’s banners ended the year with just a 2.5% YoY dip in Q4 2023, although Firehouse Subs, Popeyes Louisiana Kitchen, and Tim Hortons all saw positive visit growth for three out of four quarters of 2023.

Following three quarters of YoY visit growth for the Pizza Hut banner and for the company as a whole, Yum! Brands also began feeling the impact of the consumer spending contraction, with the company’s Q4 2023 foot traffic performance 3.7% lower, on average, than in 2022.

.png)

Who Visits Yum! and RBI Banners?

The wider QSR space tends to serve trade areas composed of Census Block Groups with an overall median household income (HHI) that is lower than the median HHI nationwide ($63.2K for QSR compared with $69.5K nationwide). And the median HHI in the trade areas of Pizza Hut, Taco Bell, KFC, Burger King, Tim Hortons, and Popeyes is even lower than the median HHI in the wider QSR space.

The relatively low median HHI in the trade areas of RBI and Yum! Brands’ QSR banners means that visitors to these chains may be feeling particularly frugal, which could explain the slight dips in foot traffic towards the end of 2023.

But some of these brands are already implementing changes to woo back their budget-conscious customers. Taco Bell recently unveiled a new value menu that includes some items priced at $1.99, and several other chains in the Yum! and RBI portfolio have launched national campaigns advertising wallet-friendly promotions – which may well bring foot traffic back up in 2024.

.png)

Yum! & RBI QSR Banners Draw More Singles

QSR chains seem particularly attractive to singles, with the trade area of the average QSR brand containing a larger share of one-person and non-family (roommate) households compared to the nationwide average (33.8% to 33.2%). And analyzing the household composition of the QSR banners of RBI and Yum! reveals that the trade areas of these brands tend to include an even larger share of one-person and non-family households than the wider QSR industry. (Pizza Hut is the sole exception, with one-person and non-family households making up 33.6% of households in its trade area – slightly less than the QSR industry average of 33.8%, but still more than the nationwide average of 33.2%.)

The trade areas of QSR brands also tend to include a greater share of large households (households of four or more people) compared to the percentage of 4+ person households nationwide. But Yum! And RBI banners (with the exception of Popeyes) seem to serve fewer 4+ person households compared to the QSR average (although Pizza Hut, Taco Bell, KFC, Burger King, and Tim Hortons still have more 4+ person households in the trade areas compared to the nationwide average.)

This trade area demographic data could help Yum! and RBI plan their 2024 promotions – discounts on larger orders could be particularly appealing to Popeyes diners, but may not necessarily drive demand among the visitor base of the other QSR banners. At the same time, all brands analyzed may benefit from offering value-priced individual items that can help singles living alone or with roommates budget smartly.

.avif)

RBI & Yum! In 2024

With food-away-from-home prices expected to increase in 2024, chains that offer low-cost options are likely to see a resurgence – and RBI and Yum! may well benefit from consumers’ continued thriftiness.

In December 2023, Placer.ai released the white paper: The Retail Opportunity of Stadiums. Below is a taste of our findings. To read more data-driven consumer research, visit our resource library.

Fan Tastes: Beyond the Bleachers

While every stadium provides a similar core of traditional game day eats, each venue also offers a unique set of dining options, both on- and off-premise. The visitor bases of the various venues also exhibit unique dining tastes – a reminder that no customer or fan base is alike. Aligning on- or off-site dining options with offerings that align with a given customer base’s preferences can improve overall visitor satisfaction and boost revenues.

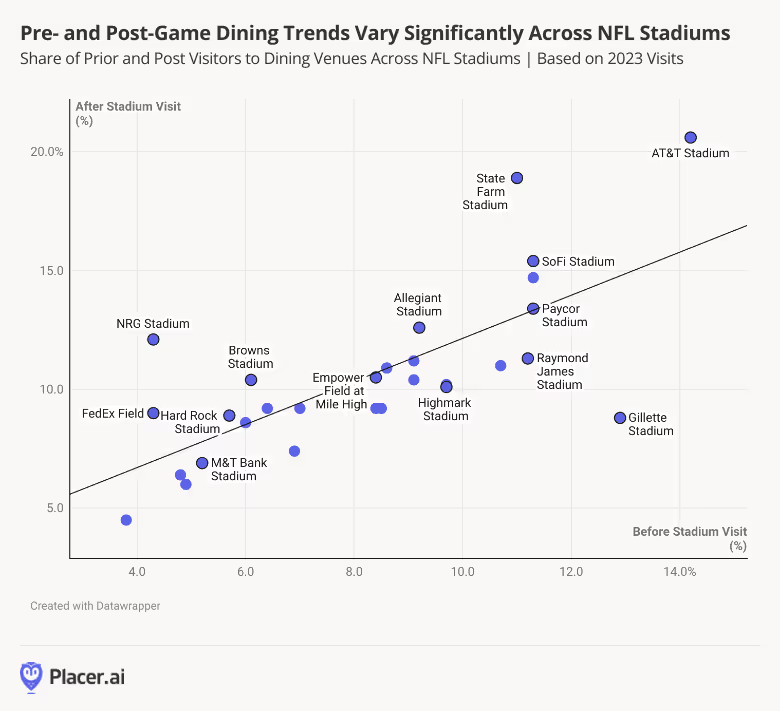

The chart below shows the share of visitors coming to a stadium from a dining venue (on the x-axis) or going to a dining venue after visiting the stadium (on the y-axis). The data reveals a correlation between pre-stadium dining and post-stadium dining – stadiums where many guests visit dining venues before the stadium also tend to have a large share of guests going to dining venues after the event. For example, the AT&T Stadium in Arlington, Texas, saw large shares of visitors grabbing a bite to eat on their journey to or from the stadium, while the M&T Bank Stadium in Baltimore, Maryland saw low rates of pre- and post stadium dining engagement.

These trends present opportunities for both local businesses and stadium stakeholders. For example, venues with high dining engagement can explore partnerships with local restaurants, while those with lower rates can build out their in-house dining options for hungry sports fans.

Different Events Drive Different Dining Patterns

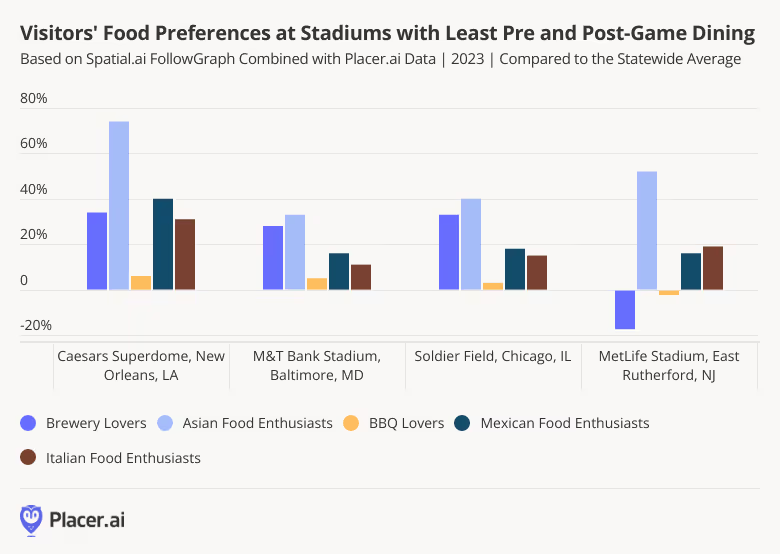

Stadiums looking to enhance their food offerings – or local entrepreneurs thinking of opening a restaurant near a stadium – can also get inspired by stadium visitors’ dining preferences. For example, psychographic data taken from the Spatial.ai: FollowGraph dataset reveals that visitors to MetLife Stadium in East Rutherford, New Jersey have a much stronger preference for Asian cuisine compared to New Jersey residents overall. With that knowledge, the stadium can enhance the visitor experience by expanding its Asian food offerings.

On the other hand, MetLife Stadium goers seem much less partial to Brewery fare than average New Jerseyans, so the stadium operators and restaurateurs may want to avoid offering too many Brewery-themed dining options. Stadium stakeholders can reserve the craft beers for Caesars Stadium, M&T Bank Stadium, and Soldier Field Stadiums, where visitors seem to enjoy artisanal brews more than the average resident in Louisiana, Maryland, and Illinois, respectively.

Major League Visits

Sports leagues like the NBA, NFL, and MLB boast billion-dollar revenues – and the venues where these games unfold hold significant commercial potential in their own rights. Stadium operators, restaurateurs, and other stakeholders can leverage location intelligence and analyze visitor behavior outside the stadiums to understand visit patterns and consumer preferences during games and in the off-season.

Read the full report here to discover more stadium insights. For more data-driven consumer research, visit our resource library.

Urban Outfitters, Inc., operates several apparel banners, including Anthropologie and the eponymous Urban Outfitters. Both brands sell bohemian-style women’s apparel and home goods, although Urban Outfitters’ selection is slightly more eclectic and also includes menswear. Location intelligence indicates that both brands have stores in areas that have the potential to attract similar types of shoppers – but in practice, the two chains’ audiences look rather different.

To better understand the contrast between the two chains, we dove into the demographic and psychographic data of Urban Outfitters’ and Anthropologie’s trade areas.

Similar Potential, Differences in Practice

Location analytics can be used to analyze a chain’s area through two different methods. The potential market trade area focuses on the demographic and psychographic makeup of the Census Block Groups (CBGs) making up the trade area, with each CBG weighted according to the population size of that CBG. The captured market trade area, on the other hand, weighs the CBGs within the trade area according to the number of visits received by the chain from each CBG. So while a potential market analysis can show the types of visitors that a chain can reach on the basis of the geographic location of the chain’s venues, the captured market reveals the audience segments within the potential trade area that actually visit the chain in practice.

For example, the median HHI for both Anthropologie and Urban Outfitters is higher in the captured market than in the potential market. This means that both brands attract visits from the higher-income households within their potential trade area.

The data also indicates that both chains have a relatively similar potential market median HHI, so both chains can reach customers with relatively similar income levels, given their store fleet configuration: Anthropologie’s potential market median HHI is only 5.5% higher than Urban Outfitters’ ($84.7K vs. $80.3K). But in practice, Anthropologie visitors tend to come from much more affluent households than Urban Outfitters visitors, with Anthropologie’s captured market median HHI 17.3% higher than Urban Outfitters’ ($103.6K vs. $88.3K).

.png)

Anthropologie & Urban Outfitters Appeal to Different Household Types

Looking at the household types in Anthropologie and Urban Outfitters’ potential markets reinforces how the two chains have the potential to draw a relatively similar visitor base. Anthropologie’s and Urban Outfitters’ potential trade areas have 38.5% and 38.8% of one-person and non-family (i.e. roommate) households, respectively, and 26.6% and 26.5% of households with children.

In practice, however, Anthropologie tends to attract more households than Urban Outfitters from family-friendly neighborhoods – the share of households with children in its captured market stands at 26.3%, compared with 23.6% for Urban Outfitters’ captured market. Meanwhile, Urban Outfitters seems to be more popular among visitors from one-person and non-family households, with 43.5% of its captured market belonging to this segment, compared to 38.5% of Anthropologie’s captured market.

.png)

Psychographic Data Shows Similar Audience Segmentation Trends

Analyzing the captured and potential markets of Anthropologie and Urban Outfitters from a psychographic perspective also reveals differences between the two brands that align with the demographic profiles in the chains’ trade areas. Anthropologie tends to attract more suburban visitors – including shoppers belonging to Spatial.ai PersonaLive’s “Booming with Confidence” segment. Meanwhile, Urban Outfitters draws more Singles & Starters than Anthropologie in both its captured and potential trade area.

.png)

Location is Not the Only Factor Impacting a Chain’s Visitors

The differences between the makeup of Athropologie’s and Urban Outfitters’ potential and captured market indicate that a chain’s site selection strategy is not the only factor impacting who visits the chain’s stores in practice.

Both Anthropologie and Urban Outfitters have relatively similar psychographics and demographics in their potential trade areas, meaning that – based solely on the location of their stores – both brands’ stores have the potential to reach the same types of shoppers. But the demographics and psychographics in the captured markets are distinct, indicating that even stores carrying similar sorts of products and located in similar areas can use contrasting branding, price-points, and other factors to draw in the desired target audience.

For more data-driven retail insights, visit placer.ai/blog.

CVS and Walgreens are the two leading brick-and-mortar pharmacy chains, controlling together over 40% of the U.S. prescription drug market. And although the companies have been rightsizing their physical footprint over the past couple of years, CVS and Walgreens together still operate over 18,000 locations throughout the country.

And while the two chains may sometimes appear interchangeable, diving into the demographic differences between CVS and Walgreens’ trade areas indicates that each brand serves a slightly different audience.

Differences in Visitor Income

A chain’s potential market looks at the Census Block Groups – CBGs – where visitors to a chain come from, weighted according to the population of each CBG. And since both CVS and Walgreens operate in all 50 states and often have locations in the same town or city, the makeup of the two chains’ potential market trade area is remarkably similar – indicating that both chains have the potential to reach the same types of households.

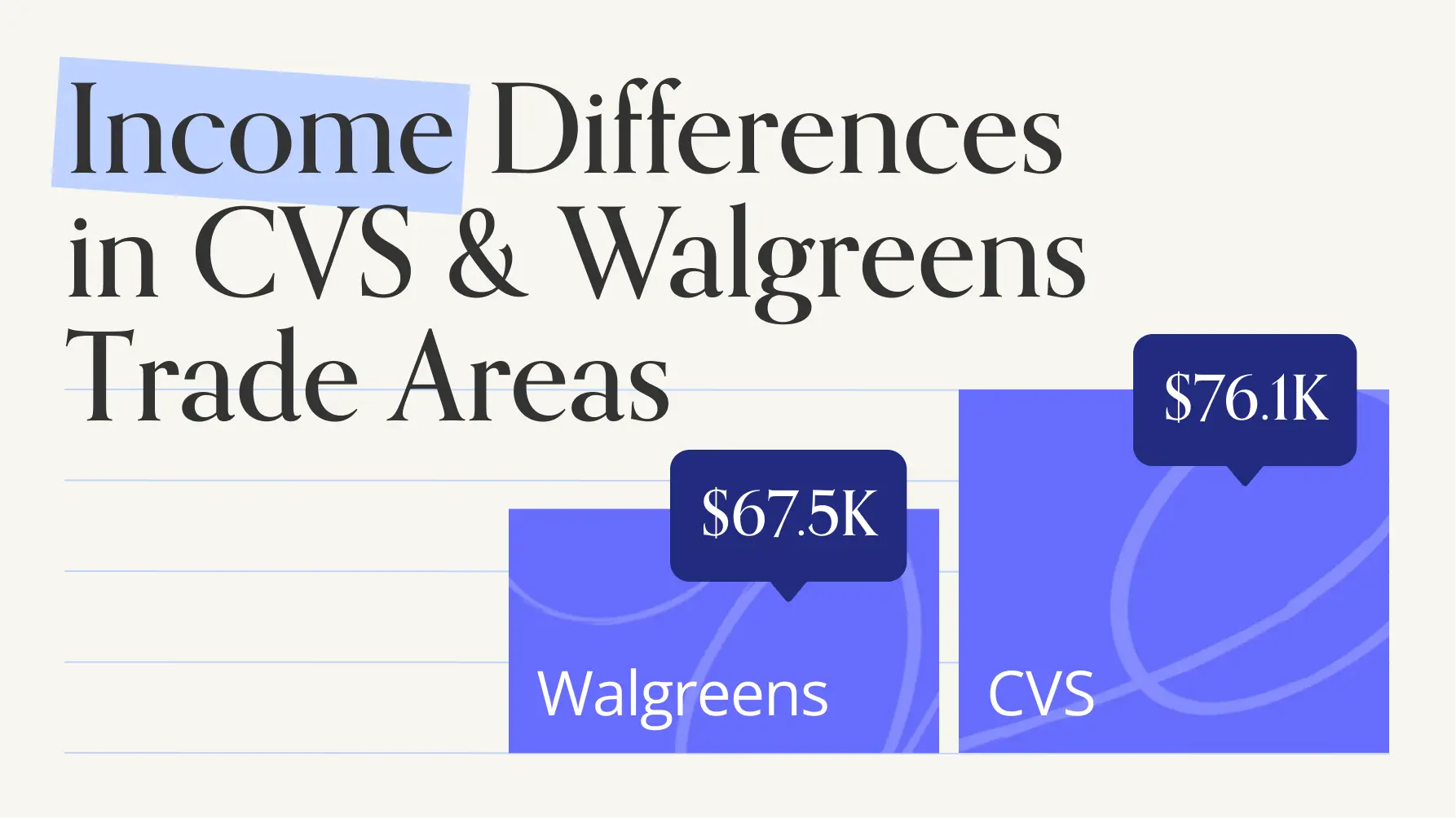

But diving into the captured market (the trade area of each chain weighted according to the actual number of visits from each CBG) reveals a major difference in trade area median household income (HHI). Although both chains have the potential to attract visitors with a median HHI of around $70.0K, visitors to CVS come from CBGs with a median HHI of $76K – meaning that visitors to CVS tend to come from the more affluent neighborhoods within CVS’s potential trade area. Walgreens visitors, on the other hand, come from CBGs with a median HHI of $67.5K, which is lower than the median HHI in the brand’s potential market, and indicates that Walgreens visitors tend to come from the less affluent neighborhood within the company’s trade area.

.avif)

CVS Attracts Larger Households, While Walgreens Serves More Singles

The two pharmacy leaders also seem to attract different shares of singles and families, although the differences are not as pronounced as the differences in median HHI.

CVS and Walgreens have equal shares of one-person & non-family households in their trade areas, but the share of this segment in Walgreens’ captured market is slightly larger than in CVS’ captured market. Still, for both brands, one-person and non-family households are slightly underrepresented in the captured market relative to the potential market, indicating that singles across the board are perhaps slightly less likely to visit brick-and-mortar pharmacy chains.

On the other hand, both CVS and Walgreens had more families (households with four or more children) in their captured market than in their potential market – although the share of this segment in CVS’ captured market was slightly higher than in Walgreens’.

.avif)

CVS Appeals to Families

CVS’ relative popularity with family segments also comes through when looking at the psychographic makeup of its trade area. When compared to Walgreens, CVS’s captured market included larger shares of three out of four family-oriented segments analyzed by the Spatial.ai: PersonaLive dataset – Ultra Wealthy Families, Wealthy Suburban Families, and Near-Urban Diverse Families. Walgreens’ captured market did include larger shares of Upper Suburban Diverse Families, but the difference was minimal – 9.8% for Walgreens compared to 9.5% for CVS.

.avif)

Differences and Overlaps between CVS and Walgreens Visitors

CVS and Walgreens carry a very similar product selection, and the two chains’ nearly identical potential trade area makeup indicates that both brands’ locations have the potential to reach the same types of customers. But diving into CVS and Walgreens’ captured market reveals some differences between the two chains’ audiences – CVS tends to attract more affluent visitors, while Walgreens seems slightly more popular among singles.

For more data-driven retail insights, visit placer.ai/blog.

What does 2024 hold for malls and shopping centers? We dove into the data to unearth the trends likely to shape the space in the coming year.

- Greater Diversity Among Mall Tenants

The move towards greater tenant diversity in malls shaped the shopping center space in recent years, and the trend appears set to be taken to the next level in 2024. Placemaking – crafting public spaces that go beyond utilitarian needs to foster social interaction and exchange – is at the forefront of many urban development initiatives, and the trend is already boosting retail performance in successful placemaking projects.

Fenton, a mixed-use district in Cary, N.C., opened in June 2022. The project showcases the potential of placemaking to transform an underutilized space into a vibrant “live-work-play” community with something for individuals and families of all ages. The retail and entertainment village includes shops, restaurants, seasonal attractions, entertainment venues, and other diverse offerings that are establishing Fenton as a community hub and a prime destination for residents. Visits were up 53.2% between July and December 2023 compared to the same period in 2022, while median dwell time increased from 64 to 83 minutes.

.avif)

Across the country, in Phoenix, AZ, Park Central Mall – the state’s first open-air shopping center – was also redesigned as a mixed-use development Park Central. The complex includes restaurants, office space, medical facilities, and bioscience research labs, with more hospitality and housing under construction. And although the project first reopened in 2019, visits to the revitalized Park Central continue to grow – between 2022 and 2023, foot traffic to Park Central increased by 32.8% while median dwell time grew from 75 to 80 minutes.

.avif)

- Higher-Income Visitors Likely to Drive Mall Visit Growth in 2024

In 2023, malls attracted relatively high income shoppers – and as the trend is likely to continue in 2024, with high-income shoppers displaying significantly stronger consumer confidence than their middle- and low-income counterparts.

Households in the potential market trade areas of Indoor Malls, Open-Air Lifestyle Centers, and Outlet Malls tended to have higher incomes relative to the nationwide median – and the median HHI was even higher in the malls’ captured market trade area. This means that many of these malls are located within relatively affluent communities (hence the relatively high potential market median HHI) and attract the higher-income shoppers within those areas (as shown by the even higher captured market median HHI).

With middle-income shoppers expected to tighten their budgets in 2024, high-income consumers will likely remain a significant share of mall-goers in 2024 as well.

.avif)

- Malls Will Continue Attracting Younger Shoppers

Malls used to be the place for teens to hang out on weekends – and it looks like shopping centers are once again attracting younger generations of consumers. Between 2019 and 2023, the share of “Young Professionals” and “Young Urban Singles” in the captured market trade areas of Indoor Malls, Open-Air Shopping Centers, and Outlet Malls increased. At the same time, the share of older segments – “Suburban Boomers” and “Sunset Boomers” – decreased.

As Gen-Z shoppers rediscover physical stores and increasingly seek out the mall-going experience, the share of younger consumers visiting shopping centers may well grow larger in the upcoming year.

.avif)

Looking Ahead to 2024

Last year’s ongoing inflation brought a unique set of challenges to a brick-and-mortar space still recovering from the pandemic’s impact. But 2023 ended with a surge in consumer confidence, and 2024 may well bring a positive shift to malls and the wider retail landscape. And shopping centers – especially those that offer a diversity of experience and succeed in catering high-income and/or younger shoppers – can take advantage of the opportunities in the year ahead.

For more data-driven insights, visit placer.ai/blog.

How did the brick-and-mortar divisions of Walmart, Target, and other leading retailers perform this holiday season? Which days drove the most visits, and how did foot traffic performance this year compare to 2022? We dove into the data to find out.

General 2023 Holiday Season Trends

Looking at daily visits to Target, Walmart, mid-tier department stores (including Macy’s, JCPenney, Kohl’s Belk, and Dillard’s), luxury department stores (including Saks Fifth Avenue, Neiman Marcus, Bloomingdale’s, and Nordstrom) and Best Buy reveals several common trends.

In all cases, retail visits began to creep up over the days leading up to Thanksgiving (Monday through Wednesday) as consumers took advantage of early Black Friday discounts. And the visit increase on Black Friday 2023 relative to the Q4 daily average was larger than in 2022 – perhaps thanks to budget-conscious consumers holding out for the steep discounts offered the day after Thanksgiving. The Christmas Eve Eve (December 23rd) and Super Saturday spikes were also particularly pronounced in 2023, likely thanks to the combination of both retail events falling on the same day this year.

All retailers and retail segments analyzed also saw smaller surges on Boxing Day (December 26th) 2023 when compared to 2022, likely due to calendar differences. Christmas fell on a Sunday in 2022, so December 26th was declared a federal holiday in lieu of December 25th, and many private-sector employers likely gave time off as well – giving consumers the opportunity to hit the stores and enjoy after-Christmas sales. But Boxing Day still drove visit peaks across the board in 2023 (albeit not smaller peaks than in 2022) – indicating that Boxing Day is now a U.S. phenomenon as well.

December 27th, 28th, and 29th saw a greater increase relative to the daily Q4 average in 2023 compared to 2022, culminating in a larger New Years Eve Eve (December 30th) spike. The December 30th surge may be because this year’s December 30th fell on a Saturday, which is a major shopping day in its own right. But the increase in the days prior to New Years Eve Eve, when after-Christmas sales were in full force, could indicate that consumers are still particularly attune to sales events.

Still, despite the similarities across retail categories, foot traffic data also reveals some important differences between the segments.

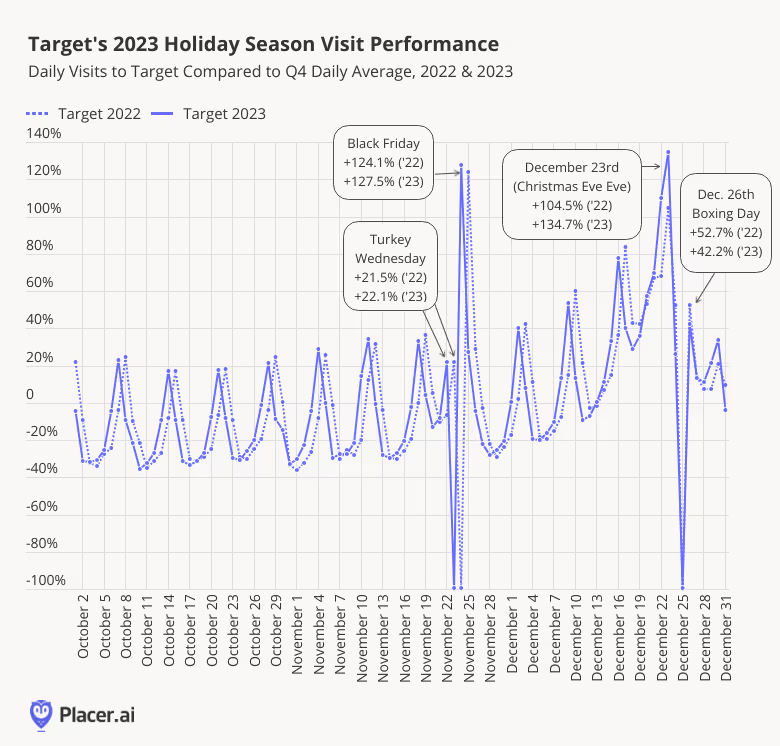

Target’s Major December Visit Build-Up

Visits to Target began to increase in November 2023 relative to October as the retailer offered “Four Weeks of Early Black Friday Deals,” starting October 29th. And like the other categories analyzed, Target saw its first small visit peak of the season on the Wednesday before Thanksgiving (also known as Turkey Wednesday thanks to the massive Grocery visit spikes on the day). Visits on the day before Thanksgiving were up by 21.5% and 22.1%, in 2022 and 2023, respectively, despite foot traffic on an average Wednesday tends to be lower than the Q4 daily average – indicating that “Turkey Wednesday” also holds retail significance for grocery-adjacent categories.

Visits then spiked on Black Friday and returned to seasonally normal levels on Saturday. Throughout December, foot traffic continued to swell, with every week exceeding the previous week’s visit performance. The intensity of the visit growth picked up the week before Christmas, with Christmas Eve Eve/Super Saturday seeing a significant jump. Finally, Target visits on Boxing Day and the week following Christmas also exceeded the Q4 daily average as consumers took advantage of end-of-season sales and looked for festive attire for their New Year’s Eve celebrations.

Walmart’s Grocery Offerings Drive Its Holiday Visit Patterns

The holiday season visit pattern at Walmart differs from those at Target in several instances. The superstore’s Turkey Visit spike was significantly more pronounced than Target’s, likely thanks to Walmart’s more extensive grocery offerings. Walmart also saw smaller spikes on Black Friday – perhaps due to the retailer’s famous “everyday low prices,” which may reduce the appeal of specific sales events. The Christmas Eve Eve/Super Saturday surge were also lower than for Target, but the Super Saturday increase relative to Black Friday spike was more pronounced, with some consumers probably visiting Walmart for last-minute groceries ahead of their Christmas dinners.

.avif)

Luxury Department Stores Visit Trends Influenced by Calendar Differences

Visits to luxury department stores (Saks Fifth Avenue, Neiman Marcus, Nordstrom, and Bloomingdale’s) followed the general retail foot traffic trends, with larger peaks on Black Friday and on Christmas Eve Eve/Super Saturday in 2023 compared to 2022. Boxing Day 2023 drove a smaller visit spike relative to last year, but foot traffic was still 98.2% higher than the Q4 2023 daily average – indicating that the day is still emerging as an important retail milestone, especially for pricier segments.

.avif)

Different End of Year Trends for Mid-Tier and Luxury Department Stores

Mid-tier department stores (Macy’s, Kohl’s, JCPenney, Belk, and Dillard’s) saw more significant spikes on Black Friday and Christmas Eve Eve/Super Saturday, and smaller spikes on Boxing Day. Luxury’s department stores’ biggest post-Christmas visit peak was on Boxing Day, but mid-tier department stores experienced their largest end-of-year increase on New Year’s Eve Eve (December 30th).

.avif)

Retail Milestones Drive Massive Visit Surges for Best Buy

Best Buy saw the strongest Q4 visit spike on Black Friday out of all the retailers and retail segments analyzed, with foot traffic up a whopping 510.9% compared to its Q4 2023 daily average. The electronics leader also had the largest Christmas Eve Eve/Super Saturday bump – with visits up 188.1% – and Boxing Day boost, with traffic up 112.9% compared to the Q4 daily average. The visit surges over the holiday season’s retail milestones indicate that demand for electronics remains strong – even as some consumers may be putting off large purchases due to economic headwinds.

.avif)

The holiday season drove significant retail foot traffic across categories, with every segment displaying its own unique Q4 visitation pattern. How will these sectors perform in the year ahead?

Visit placer.ai/blog to find out.