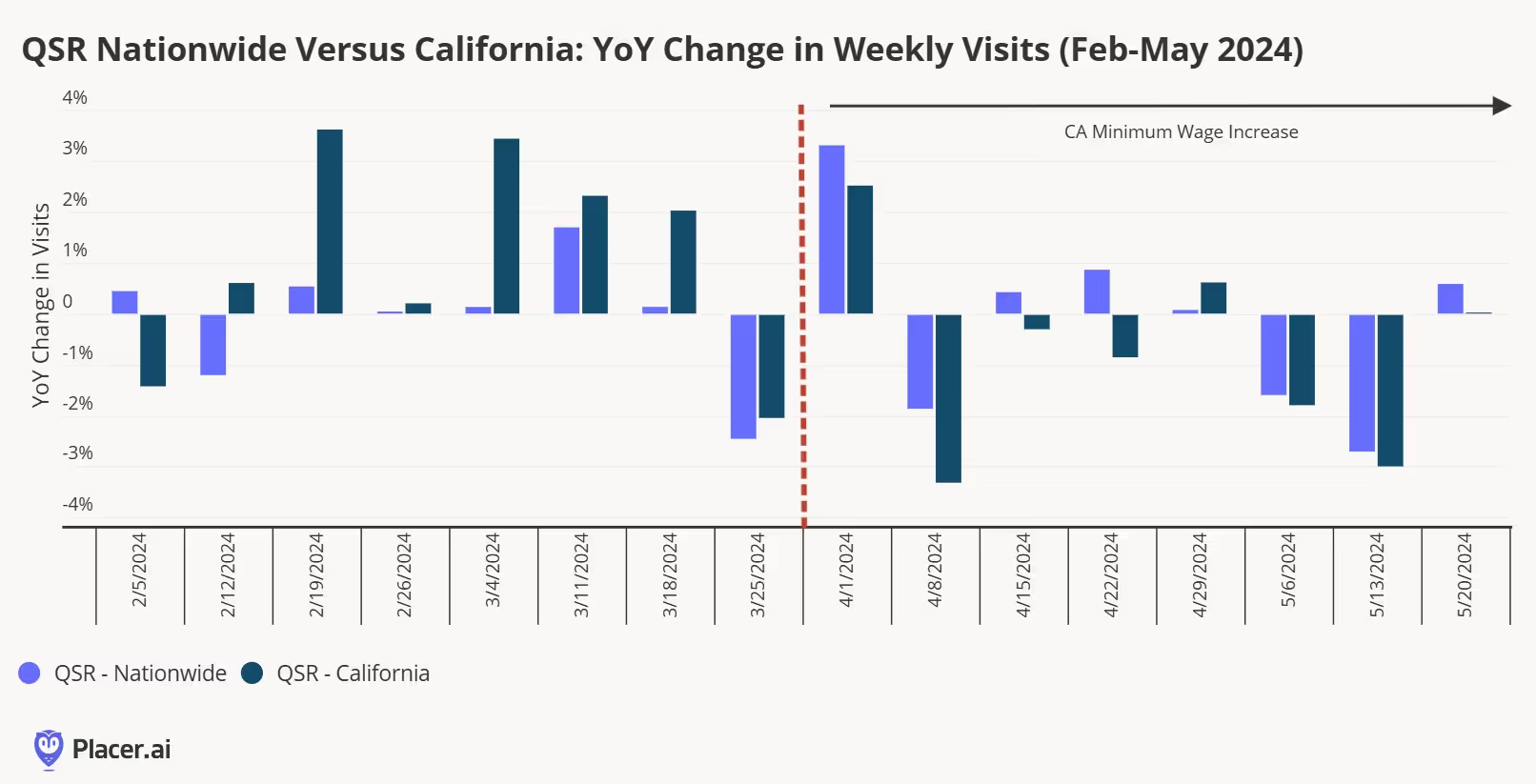

Over the past few months, we’ve noted how consumers–particularly from lower-income trade areas–have started to migrate from QSR to value-grocers, dollar stores, and convenience stores. Against that backdrop, we wanted to examine visitation trends for QSR chains in the state of California, where a $20 per hour minimum wage law was put in place on April 1 for employees of fast-food chains with more than 60 locations nationwide (with some exemptions for smaller stores at grocery stores, airports, and entertainment venues). This represented a 25% increase from the previous minimum wage for fast-food employees of $16 per hour (which remains the state’s minimum wage for other categories except for workers in healthcare facilities, which also saw minimum wage increased to $20 per hour).

As a result of the minimum wage increase, most chains have raised prices in the region anywhere from the mid-single digits to the midteens. We compared year-over-year visit trends for QSR chains nationwide and California, and it’s clear that the menu price increase is having an impact. During February-March 2024 (we’ve excluded January due to inclement weather across much of the country), year-over-year QSR visit trends in the state of California had been running slightly ahead of national averages (below). However, this abruptly shifted when the minimum wage increase went into effect, with the nationwide visit trend year-over-year exceeding the state average seven of the eight weeks during the April-May 2024 timeframe.

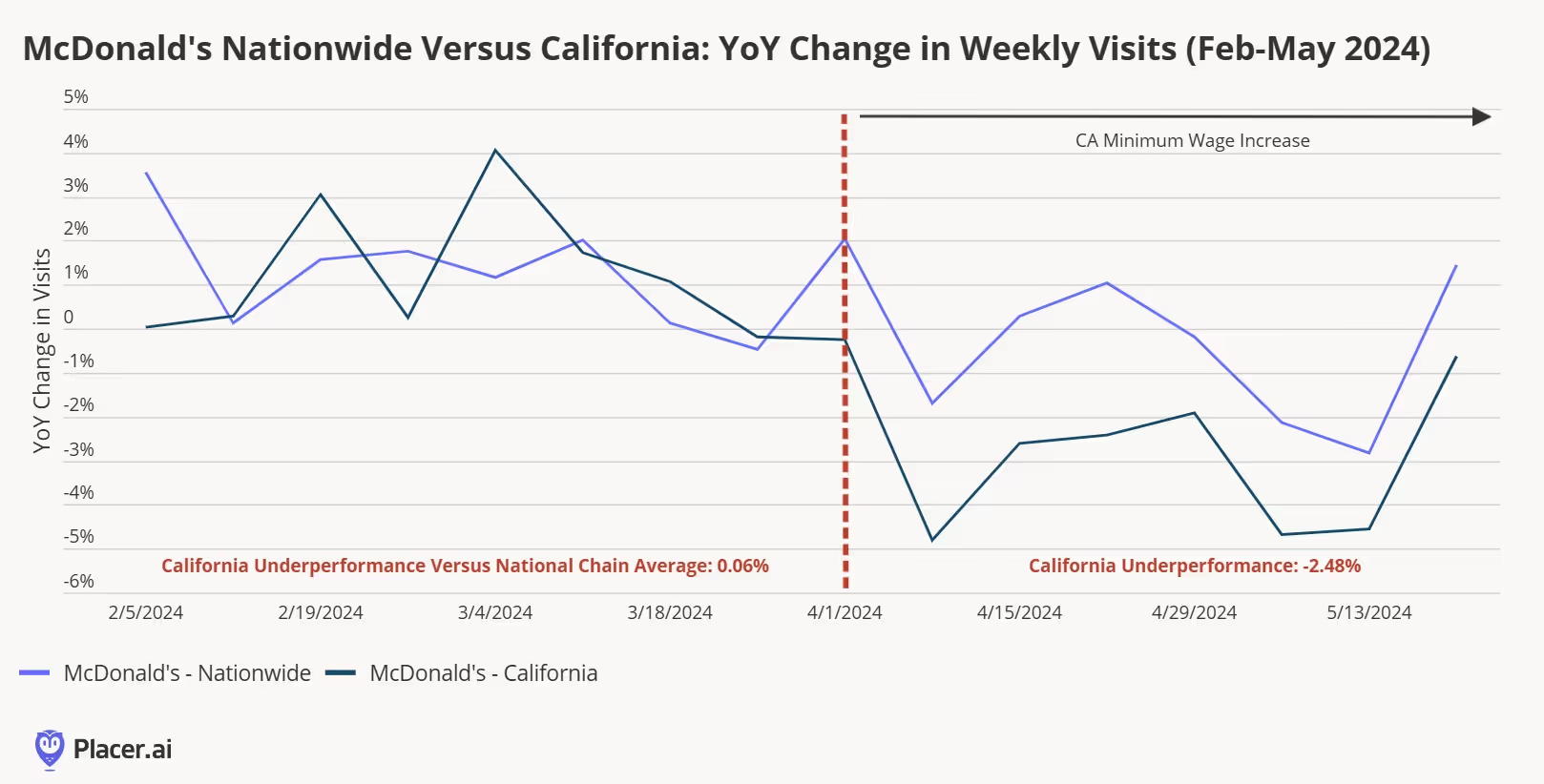

We also see the impact at the chain level. Below, we’ve looked at year-over-year visitation trends for McDonald’s nationwide and in California (where about 9% of its restaurants are located) from February through May. Again, we see a situation where McDonald’s California was seeing roughly the same year-over-year visit trends as its national average during February-March but underperformed by almost 250 basis points after the minimum wage increase went into effect.

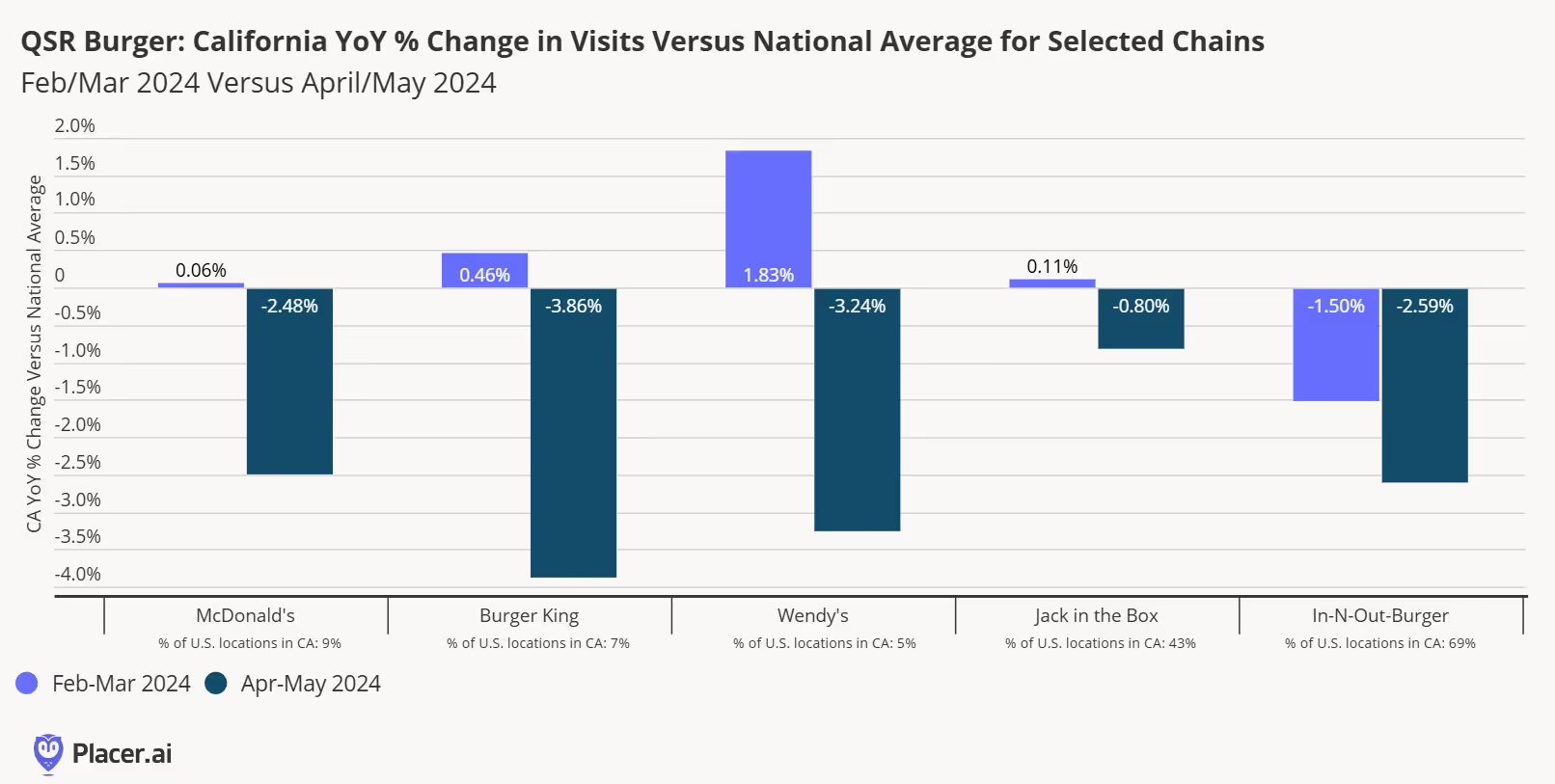

Our data indicates that QSR burger chains have generally been the hardest hit by the California increase in minimum wage and subsequent increase in menu prices. In addition to McDonald’s, we see that other large QSR burger chains in the state also underperformed their national average following the minimum wage increase. Chipotle–which raised menu prices by 6%-7% in California to help offset the minimum wage increase–also saw year-over-year visit trends in California underperform its national average in April and May.

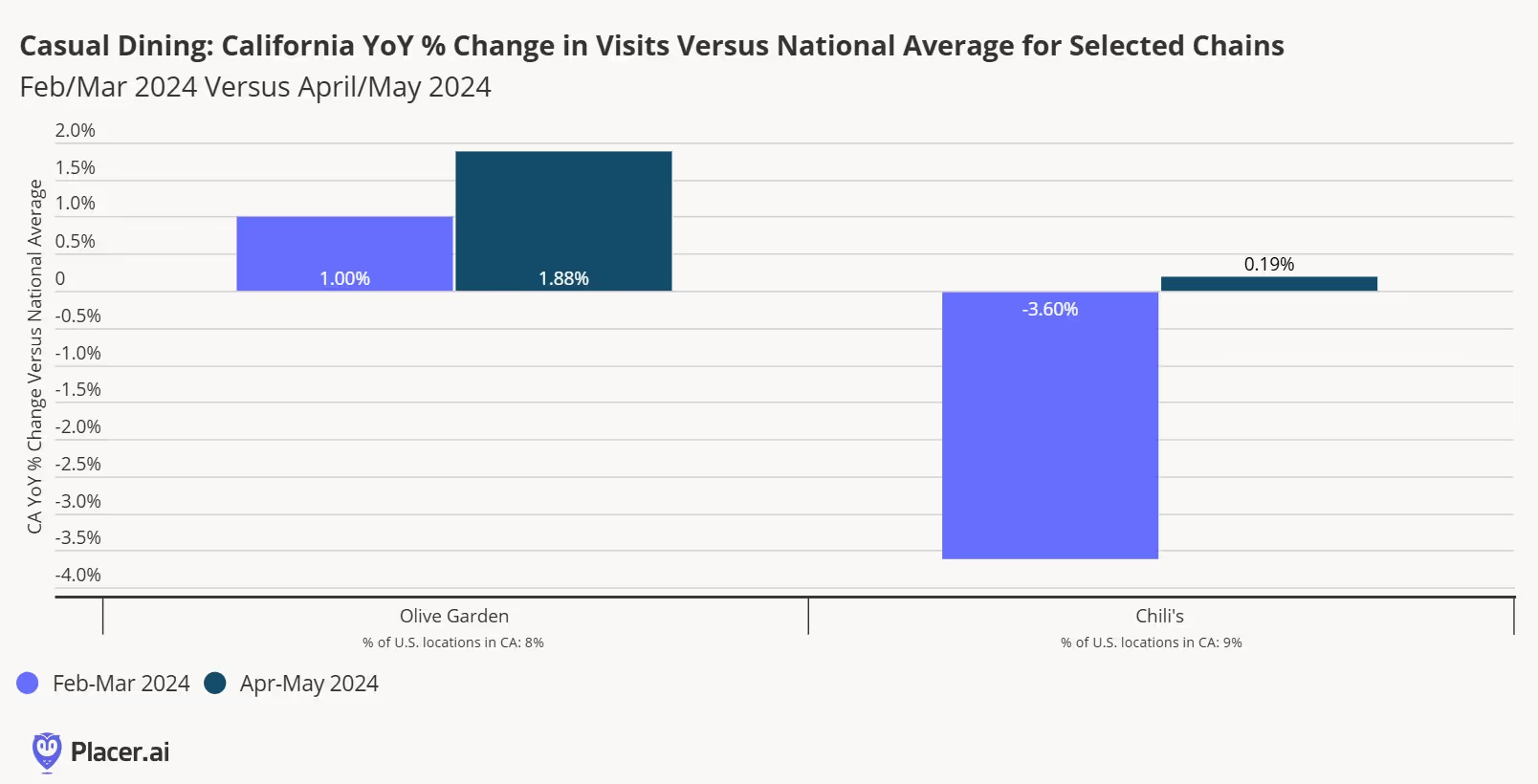

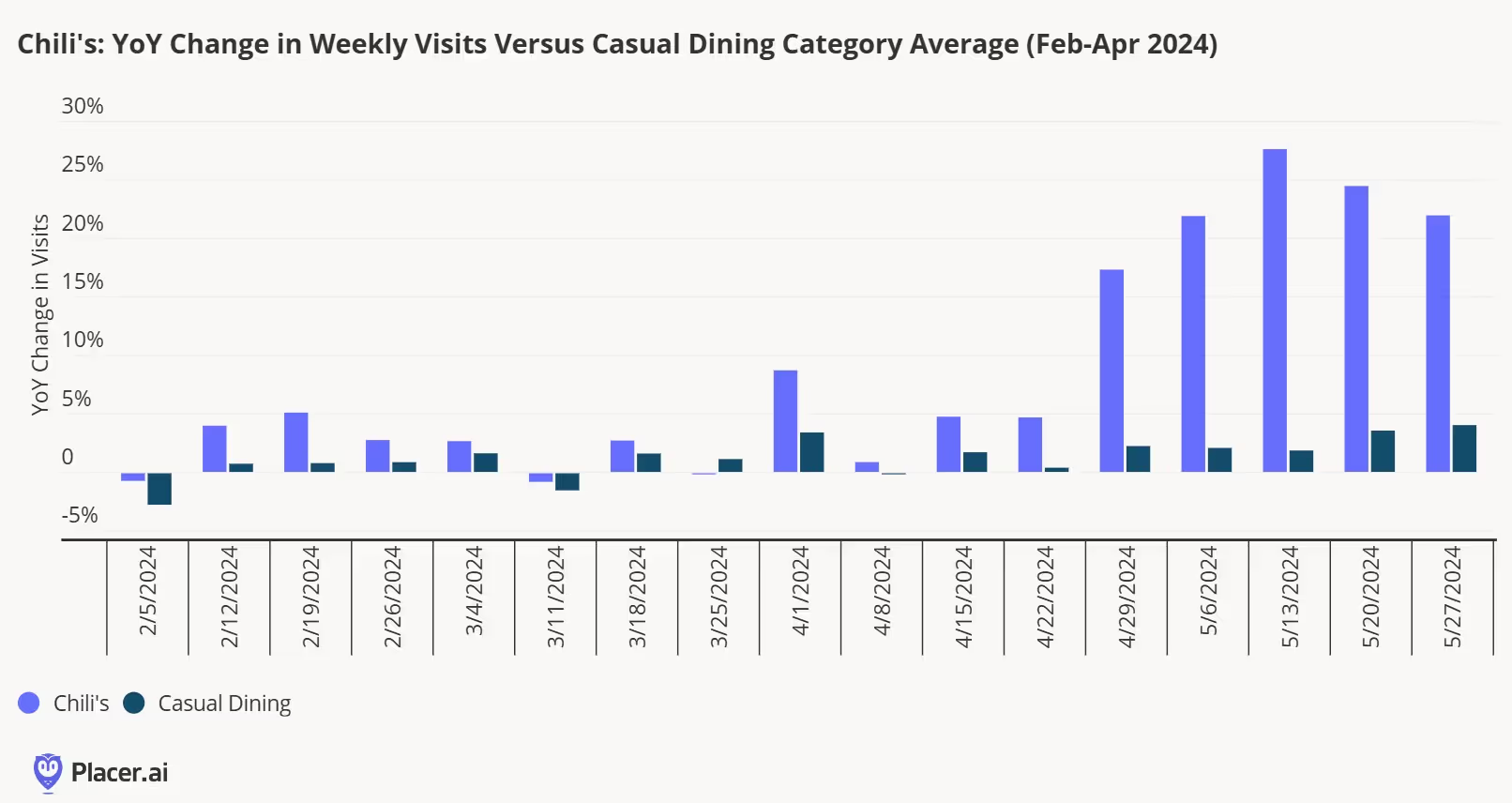

It’s early, but we’re starting to see the ripple effect of the minimum wage increase across the broader restaurant industry. First, we’ve started to see some operators close locations in the state, especially chains that were already facing financial difficulties. Earlier this week, Rubio’s Coastal Grill shut down almost 50 locations in California and filed for Chapter 11 bankruptcy protection, citing “significant increases to the minimum wage in California” as a reason for closing the restaurants. Second, the minimum wage hike and subsequent increase in QSR menu prices may be benefitting casual dining chains (many of which were already paying above the new minimum wages for many employees). Below, we see that Darden’s Olive Garden concept and Brinker International’s Chili’s concept in California have outperformed their national averages with respect to year-over-year visit trends starting in April (below). Finally, the minimum wage increase could make it more costly to do business across other retail and restaurant categories, something we called out in our recap of 99 Cents Only going out of business.

As we discussed following this year’s National Restaurant Association show, casual dining has been making a comeback the past several months, with many chains accentuating value proposition through promotions. Chili’s has seen visitation trends outperform casual-dining category averages by a significant amount the past several weeks (below) through its value messaging, while Buffalo Wild Wings All-You-Can Eat wings promotions on Monday and Wednesdays starting in mid-May has been one of the more successful promotions that we’ve seen in the full-service restaurant category in some time. However, with several QSR chains starting to get more promotional ahead of McDonald’s planned $5 value menu promotion at the end of the month, it’s clear that QSR chains are looking to also emphasize value in the coming months, even while facing higher labor costs.

Our May mall index examines visit performance at malls, indoor malls, outlet malls, and open-air shopping centers to see how visits rebounded from April's dip and explores how Mother's Day and Memorial Day drove visits across malls.

Maytal Cohen

Jun 6, 2024

3 minutes

About the Mall Index:The Index analyzes data from 100 top-tier indoor malls, 100 open-air shopping centers (not including outlet malls) and 100 outlet malls across the country, in both urban and suburban areas. Placer.ai leverages a panel of tens of millions of devices and utilizes machine learning to make estimations for visits to locations across the country.

Key Takeaways:

In May 2024, indoor malls, outlet malls, and open-air shopping centers all saw significant year-over-year (YoY) visit increases – providing further evidence that April’s slowdown was due to an Easter holiday calendar shift, rather than any real category weakness.

Both Mother’s Day and Memorial Day drove substantial visit spikes across mall types – with foot traffic outperforming last year’s levels.

Outlet malls experienced more pronounced visit bumps on Easter weekend and Memorial Day, while open-air shopping centers drew bigger spikes on Mother’s Day.

May Sees a Strong Rebound in Mall Visits

After a brief calendar-driven slowdown in April, May saw a resurgence in foot traffic to malls. Indoor malls led the way with an 8.6% YoY increase, followed by open-air shopping centers and outlet malls, which experienced YoY jumps of 6.2% and 5.7%, respectively.

This uptick is likely due to a variety of factors – from warmer weather to rising consumer confidence amidst slowly easing inflation. And malls’ particularly strong showing on two of May’s most important retail milestones – Mother’s day and Memorial day also helped propel the segment forward.

Category Strength Boosted and Showcased by Holiday Visit Spikes

Taking a closer look at visit patterns to the three mall types on Mother’s Day and Memorial Day shows how significant these special days were for mall foot traffic. On Mother’s Day (May 12th), indoor malls, open-air shopping centers, and outlet malls saw respective visit spikes of 15.8%, 26.0%, and 11.4%, compared to an average year-to-date (YTD) Sunday. And Mother’s Day visits were up significantly YoY as well – further highlighting the category’s robust positioning.

All three mall types also saw impressive visit bumps on Memorial Day – this time compared to an average YTD Monday. The relative spikes were bigger across the board, since malls tend to be less busy on Mondays than on Sundays. But for outlet malls, Memorial Day visits really hit it out of the park – with foot traffic up by a whopping 123.3%. As a day off work featuring plenty of markdowns, Memorial Day is an ideal time to make the longer trip to an outlet mall and hunt for bargains.

And in another promising sign for the category, Memorial Day visits to all three mall types increased YoY – showing that despite continued headwinds, malls are still on the rise.

Which Mall Kings Rule Special Calendar Days?

Comparing weekly mall visits to an early January baseline also shows the varying impact of different holidays on the three mall types.

On Easter, and even more so on Memorial Day – an extended weekend very much focused on savings – outlet malls won the day. On these holidays, shoppers may be more likely to have the time and state of mind to make a day of their shopping trip and lean into the treasure-hunting experience.

But on Mother’s Day, more upscale open-air shopping centers took the lead, as consumers embraced a more unique and luxurious shopping experience. Still, all three mall types drew increased traffic on the different special days – showing that each can benefit from a variety of calendar highlights.

Looking Ahead

Malls’ strong May performance – especially on the holidays – shows that shopping centers are on the upswing once again. This could be an encouraging sign for the category heading into the summer, and may hint at a promising shopping season during the warm months ahead.

For more data-driven retail insights, visit our blog at Placer.ai.

With summer nearly upon us, we dove into the data to see how the return-to-office fared in May 2024. Did the post-pandemic visit recovery trajectory observed in April continue apace? And which major regional hub saw the most YoY visit growth?

Lila Margalit

Jun 5, 2024

3 Min

The Placer.ai Nationwide Office Building Index: The office building index analyzes foot traffic data from some 1,000 office buildings across the country. It only includes commercial office buildings, and commercial office buildings with retail offerings on the first floor (like an office building that might include a national coffee chain on the ground floor). It does NOT include mixed-use buildings that are both residential and commercial.

With summer nearly upon us, we dove into the data to see how the return-to-office fared in May 2024. Did the post-pandemic visit recovery trajectory observed in April continue apace? And which major regional hub saw the most YoY visit growth?

May Office Visits Hold Steady

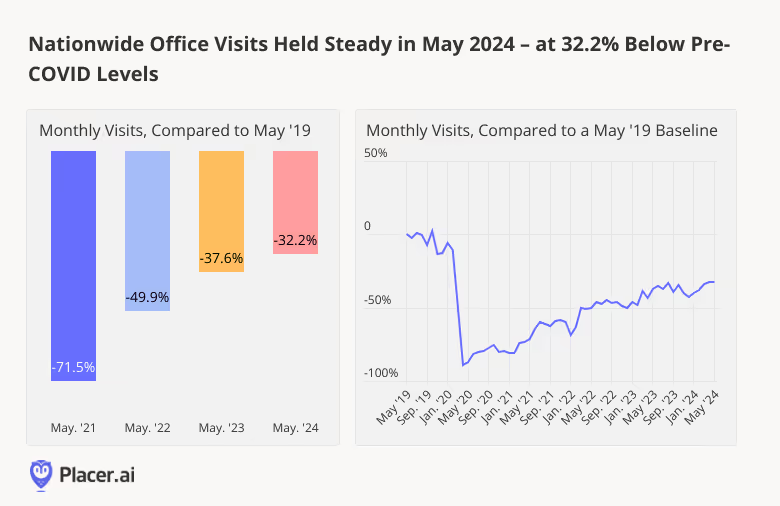

The office recovery is still very much underway. Visits to office buildings nationwide in May 2024 were just 32.2% lower than in May 2019 – and slightly higher than they’ve been during any other month since COVID. Year-over-year (YoY), office foot traffic in May increased by 8.6%.

Regional Round Robin

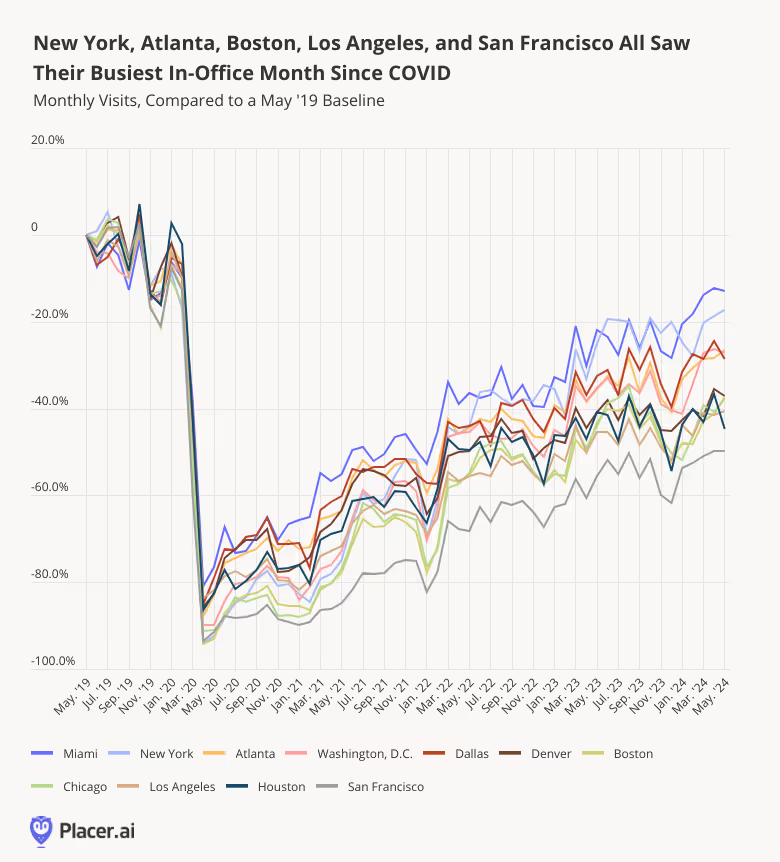

And drilling down into the data for 11 major business hubs nationwide shows recovery continuing unabated throughout (most of) the country. For New York, Atlanta, Boston, Los Angeles, and San Francisco, May 2024 was the single busiest in-office month since February 2020. And for Miami, Washington, D.C., and Denver, it was the second-busiest month.

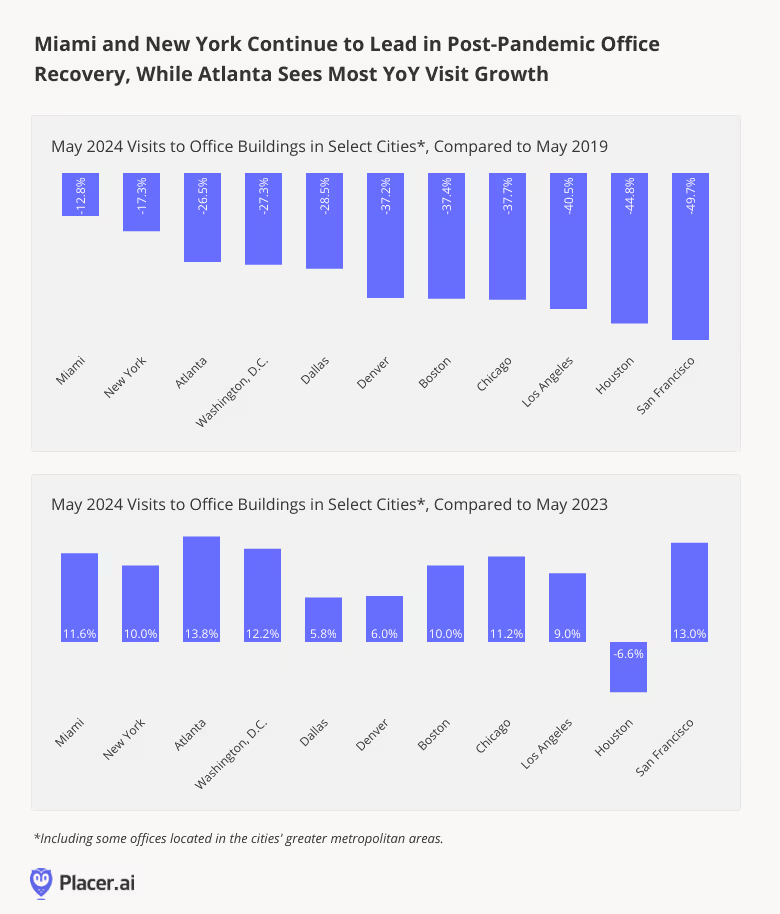

Consistent with recent trends, Miami continued to lead the post-COVID recovery pack, followed by New York: Foot traffic to the two cities was just 12.8% and 17.3%, respectively, below May 2019 levels.

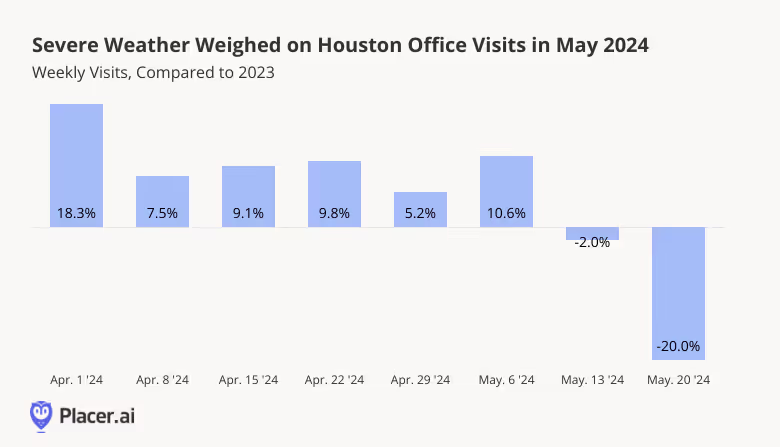

But the data also contained some surprises. Atlanta, which saw the biggest YoY visit jump of any analyzed city, pulled into third place – outpacing Washington, D.C. And Houston, the only city to see a YoY decline in visits, fell significantly in the rankings.

Houston Office Visits Impacted by Storm

Why did Houston YoY office visits drop in May? A look at weekly YoY visits to local office buildings confirms that this was likely due to the extreme weather that engulfed the city during the second half of the month. On Thursday, May 16th, Houston was hit by a particularly violent storm that caused significant damage to the downtown area – breaking windows, downing power lines, and leaving a battered city in its wake. Additional severe weather events pummeled the region as the month wore on – forcing many residents to hunker down at home. And it was when the storm hit that YoY visits began to turn negative, with the week of May 20th seeing a significant 20.0% drop. As the weather improves in the southeast Texas hub, office recovery will likely resume.

Final Thoughts

Five years after COVID upended office routines, employees and companies are still feelingout the ideal balance between WFH and in-person interaction. Will office attendance increase or decrease as the weather warms up?

Follow Placer.ai’s data-driven office analyses to find out.

With summer upon us, we dove into the data to explore Memorial Day foot traffic trends. How did people spend the long weekend? And how did major dining and retail categories fare on the holiday?

Lila Margalit

Jun 4, 2024

3 minutes

With summer upon us, we dove into the data to explore Memorial Day foot traffic trends. How did people spend the long weekend? And how did major dining and retail categories fare on the holiday?

Road Tripping

Gas stations were bustling on Friday, May 24th, as people filled their tanks in anticipation of a long, travel or activity-filled weekend. Visits to gas stations were up 32.3% compared to an average day this year – and the highest they’ve been since January 1st, 2024.

Year over year (YoY), gas station foot traffic increased 1.5%. And compared to pre-COVID, too, gas station visits were up 1.8% – showing that people are once again hitting the road, whether to go on weekend getaways or to visit nearby parks and attractions.

Seeing the Sights

Indeed, Americans partake in many different activities on Memorial Day – from attending parades and memorial events to sight-seeing or enjoying the great outdoors. And visiting museums is a time-honored holiday tradition: On Monday, May 27th, museums nationwide drew a whopping 71.5% more visits than on an average Monday this year.

YoY, Museums were 1.6% busier on May 27th than in 2023 – and museum-goers spent more time exploring the exhibits (who says attention spans are decreasing?), browsing the gift shop, or fueling up at the cafeteria.

Enjoying A Nice Meal

Memorial Day weekend is a prime time for picnics and barbecues. But for many Americans, it’s also an opportunity to enjoy a nice meal at a restaurant with friends and family.

Like on Mother’s Day, full-service restaurants get a much bigger Memorial Day visit boost than either fast-casual eateries or fast-food (QSR) joints. But all three dining segments enjoyed a significant YoY holiday visit increase this year – proving that despite still-high food-away-from-home prices, people are finding room in their budgets to treat themselves on their day off.

Hitting the Sales

And the last Monday in May is, of course, a big day for savings, on everything from big-ticket items like mattresses, furniture, and major appliances, to clothing and other discretionary items. This year, apparel stores saw the biggest Memorial Day visit spike, with foot traffic up 40.5% compared to an average day and 88.2% compared to an average Monday. But home furnishing stores, home improvement stores, electronics retailers, and (to a lesser extent), grocery stores, all experienced considerable holiday visit spikes of their own.

And comparing Memorial Day retail activity to last year shows most of the analyzed categories seeing minor visit increases or holding steady – no small feat in today’s challenging retail environment. Like dining segments, grocery stores impressed with a 9.3% YoY visit increase – perhaps buoyed by consumers buying last-minute ingredients for their picnics or barbecues.

Final Thoughts

People were on the move this year on Memorial Day – fueling up their cars, and enjoying museums, restaurants, and retail sales. What does the rest of the summer hold in store for American consumers?

Follow Placer.ai’s data driven analyses to find out.

We dove into tourism and migration data for Las Vegas, NV to take a closer look at changing visitor and resident populations in the entertainment capital of the world.

Ezra Carmel

Jun 3, 2024

3 minutes

Known as the entertainment capital of the world, Las Vegas has always been a tourist hotspot. But for a growing segment of the population, Vegas is also becoming a popular place to lay down permanent roots. We dove into the tourism and migration data for the region in order to take a closer look at Las Vegas’ changing visitor and resident populations.

Viva Las Vegas: Overnight Stays Are Up

Like many vacation destinations, Las Vegas took a significant tourism hit at the onset of COVID. But with travel restrictions now a thing of the past, visitation to Las Vegas is roaring back.

Analyzing travel to Las Vegas using the Travel & Tourism Report shows that since the halfway mark of 2023, the total number of visit nights spent by travelers in the city (i.e. by those staying up 31 days) have consistently outperformed pre-pandemic levels. And with the sole exception of July 2023, visit nights have increased year-over-year (YoY) as well.

Alongside robust demand for experiences, investment in new, one-of-a-kind entertainment venues like the Sphere – which opened towards the end of 2023 – has likely played a part in reigniting tourism.

High Rollers: A Steady Increase in Affluent Visitors to The Strip

Who are the tourists driving this comeback? To explore the demographic characteristics of today’s visitors to Las Vegas, we zoomed in on the Las Vegas Strip – the iconic epicenter of it all, where most of the city’s luxury hotels, shops, restaurants, and casinos are concentrated.

Analysis of the Strip’s captured market with demographic data from AGS: Demographic Dimensions reveals that as tourist activity in the city began to pick up again, the median household income (HHI) of visitors to the Strip increased steadily. In Q1 2024, the median HHI of visitors to the Strip reached $93.0K, perhaps aided by tourism surrounding this year’s Super Bowl.

This indicates that the Strip is becoming a more upscale visit destination, and that demand for Vegas’ luxury offerings are driving visits. As more consumers with ample discretionary dollars make their way to Vegas, pricey shows – in addition to retail – are likely to become ever-more lucrative advertising opportunities.

Full House: Net-Positive and High-Income Migration to the Region

A tourism boom isn’t the only phenomenon making waves in Sin City. In recent years, more and more out-of-towners have made Greater Las Vegas their home, and unlike some pandemic-era migration hotspots, Las Vegas continues to attract new residents.

Between December 2019 and December 2023, the Las Vegas-Henderson-Paradise CBSA experienced net-positive domestic migration of 3.9%. In other words, the total number of people that moved to Las Vegas over the four-year period from elsewhere in the U.S., minus those that left, was equivalent to 3.9% of the region’s December 2023 population. Meanwhile, analysis of the CBSA’s origin to destination HHI ratio reveals that between December 2019 and December 2023, the median HHI of incoming residents was 20% higher than the median HHI of the local population.

And comparing migration data in December 2023 to December 2020, 2021, and 2022, revealed consistently positive net migration and origin to destination HHI ratios in the years since 2019. This indicates that the Las Vegas-Henderson-Paradise CBSA continues to attract many new and affluent residents. When planning future amenities and services, the region may want to take into account the opportunities – and challenges – presented by these population shifts.

The Desert Oasis Calls

Be it for a quick trip or full-on relocation, Las Vegas remains a prime destination in both the U.S. tourism and domestic migration landscapes. New entertainment venues and amenities keep Vegas top-of-mind for upscale vacationers while economic incentives drive moves from a high-income cohort.

For more tourism and migration insights, visit Placer.ai.

Last summer’s touring sensations Taylor Swift and Beyonce held concerts that will remain in the hearts of many. With thousands in attendance, both live tours were absolute juggernauts. It was like an adrenaline shot for the performing arts category after COVID-induced closures. Remember the days of drive-in concerts as a panacea? While these two reigning Queens of Music took top billing, there are hundreds of local venues around the country that cater to smaller audiences at a time but are no less impactful on their communities. These are the heart and soul for local plays, musicals, symphonies, operas, touring bands, and art exhibitions. Fundraisers are often held at community performance venues, and they can be incubators for performers to move on to a larger stage.

Placer recently attended the California Presenters Conference, which includes representatives from California, Oregon, Washington, Nevada, Arizona, New Mexico, and Texas. Programming directors, events managers, and community liaisons all met to share best practices, challenges, and successes. One box office manager, Jonathan Lizardo of the Lisa Smith Wengler Center for the Arts at Pepperdine University, noted that “Nostalgia” was an important theme at his performing arts center, with a recent live show of the Animaniacs in Concert proving to be a hit with adults and kids alike. In this case, his patrons were seeking some escapism and levity in their lives. On the other end of the spectrum, the arts can also be a powerful way to engage the audience in more serious issues, as one panel on Responding to Global Conflict at arts venues drew a crowd. Another topic of interest was the importance of engaging youth with the arts, through school-sponsored visits or after school enrichment. Many University performing arts centers reps were also in attendance, such as USC Vision and Voices, Stanford Live, Caltech Presents, and Seattle University.

Placer’s presentation touched on macrotrends around discretionary spend, examples of venue attendance around the US, an analysis of the visitation trends, audience profile, and economic impact of Taylor Swift’s US tour, and in depth look at a select group of performing arts centers in Arizona to see the role that they play in their community.

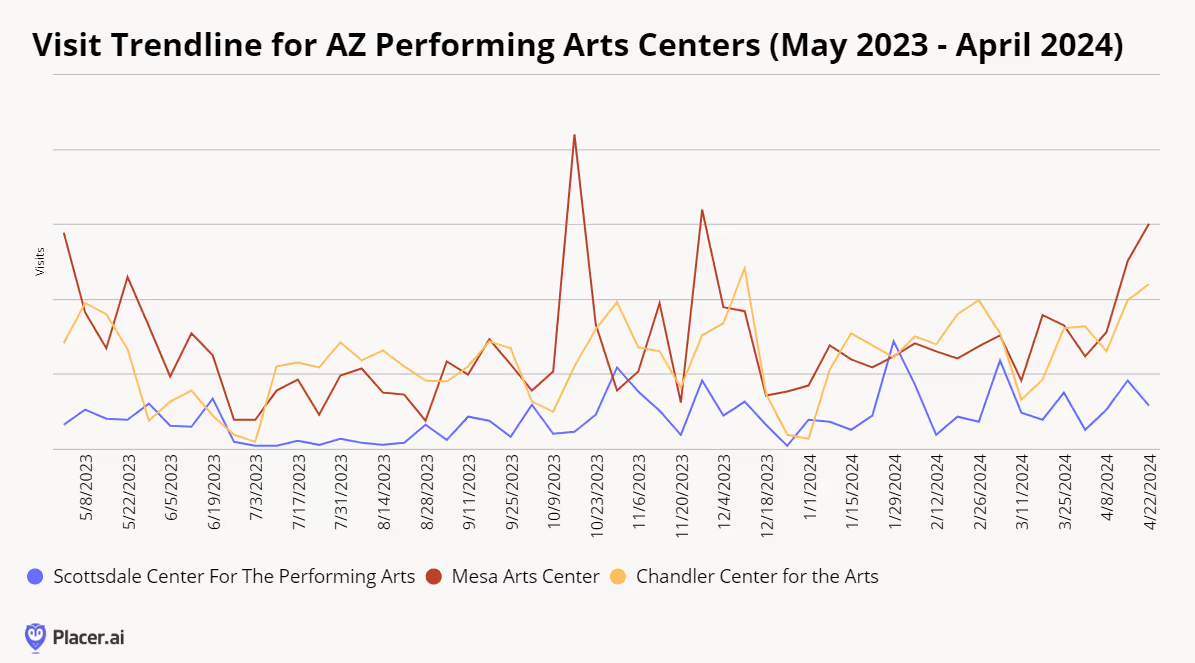

Mesa Arts Center has had the highest overall visitation in the past 12 months. Located in Mesa, AZ, it encompasses over 210,000 sq ft and was completed in 2005 at the cost of $95 million. In addition to four performance venues, it is also home to Mesa Contemporary Arts Museum. Programming is suited to a multitude of interests, including National Geographic Live, Broadway, classical music, popular music, ethnic artists, western artists, and dance. It also offers Art Studio for visual arts classes; Opportunities for Ages 55+ such as flamenco classes; and Festivals and Events, such as Dia de Los Muertos. Within the theaters complex, there are four theaters--the 1,570-seat Tom and Janet Ikeda Theater, 550-seat Virginia G. Piper Repertory Theater, 200-seatNesbitt/Elliott Playhouse, and the 99-seat Anita Cox Farnsworth Studio.

The Chandler Center for the Arts recently celebrated its 35th season. Upcoming performances include ballet like Coppelia or live music, such as Billy Joel’s The Stranger. Entertaining acts such as Stomp, Piano Battle, and Cirque du Soleil will also make their way over during the 2024-2025 season. Located in downtown Chandler, the venue includes three dynamic performance spaces (the 1,500-seat Main Stage, the 350-seat Hal Bogle Theatre, and the 250-seat Recital Hall) as well as two extensive art galleries (The Gallery at CCA and Vision Gallery).

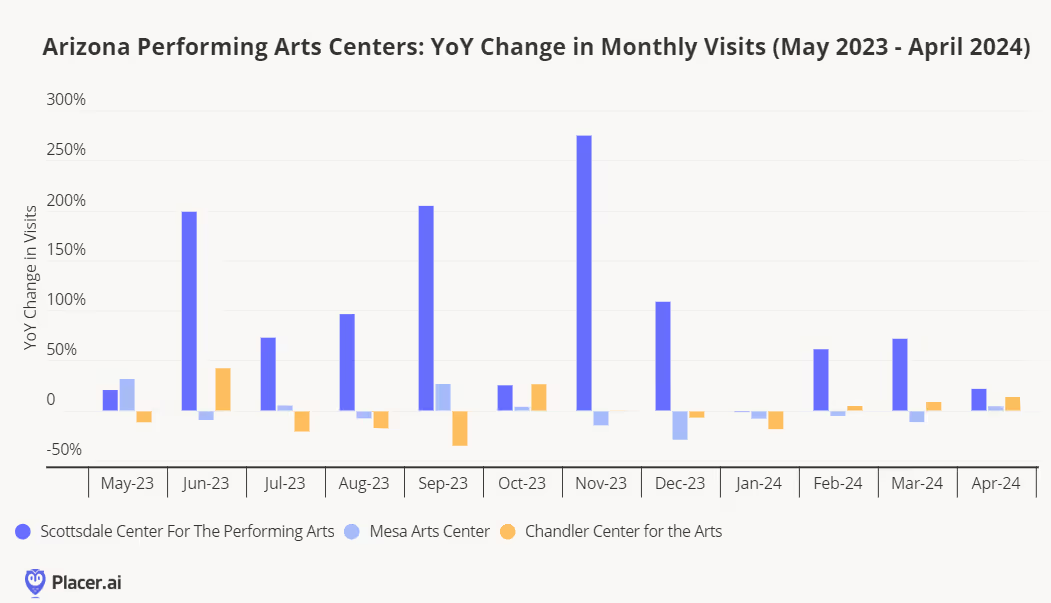

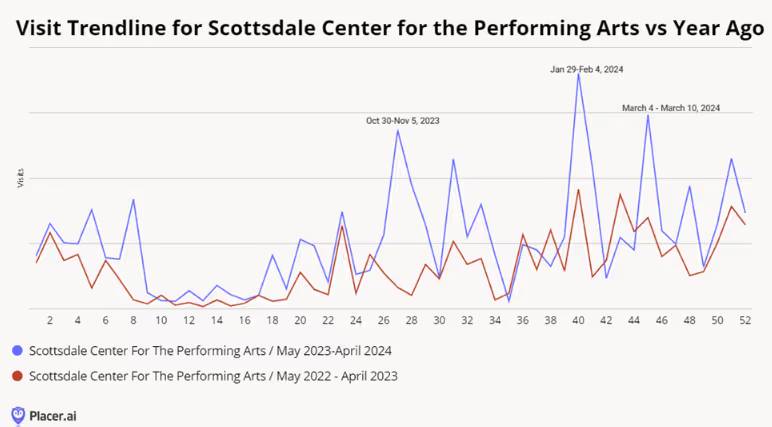

While Scottsdale Center for the Performing Arts had the fewest absolute visits in the past 12 months, its year-over-year variance increase has been the highest.

What might account for the difference, one might wonder. Fortunately, Placer data enables one to compare a venue against itself in order to highlight differences from one year to the next. According to the 2023-2024 calendar, it appears that Hubbard Street Dance Chicago playing 2 nights in a row, was a hit with the audience during the week of Jan 29-Feb 4.

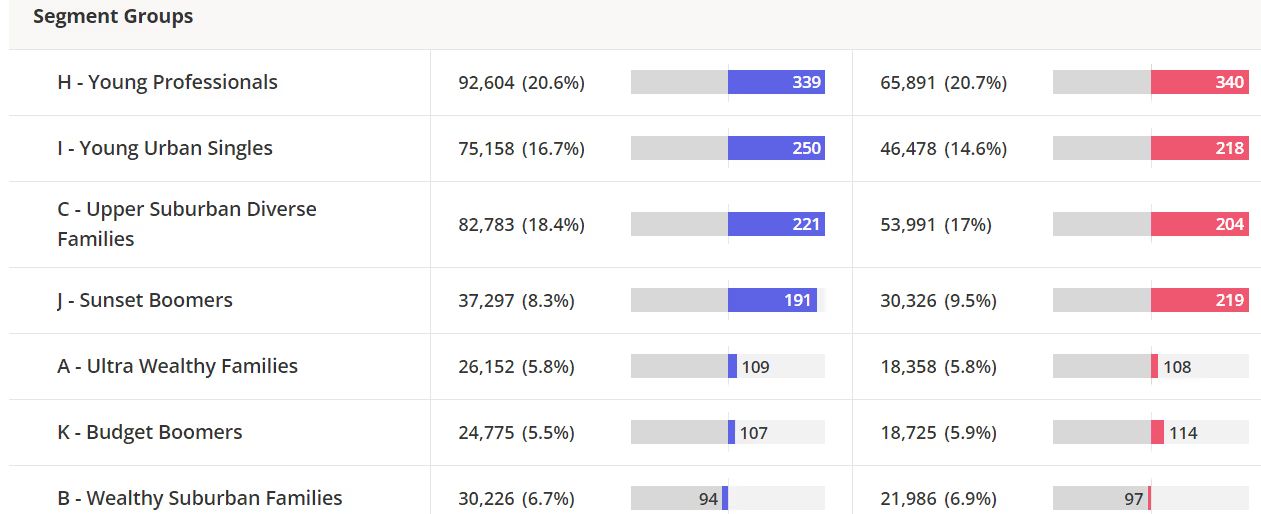

It appears the increase in visits cannot be attributed to a single segment. In fact, visits across multiple segments increased year-over-year when comparing May 2023 - April 2024 (blue) vs. May 2022-April 2023 (red) per Spatial.ai PersonaLive.

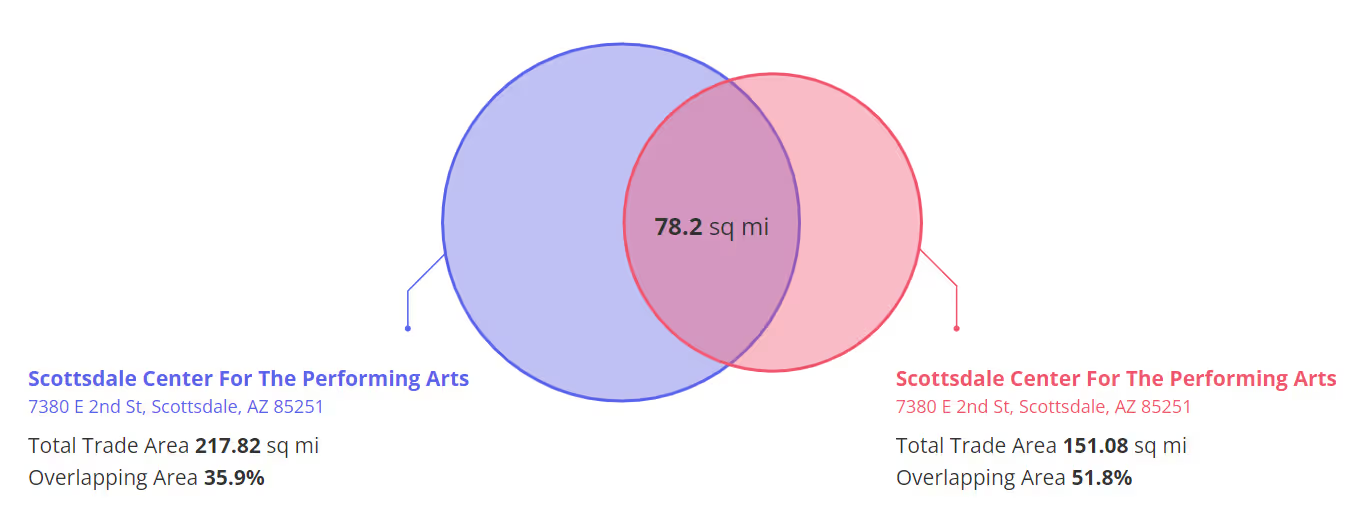

The most recent 12 months also attracted visits from a much larger trade area.

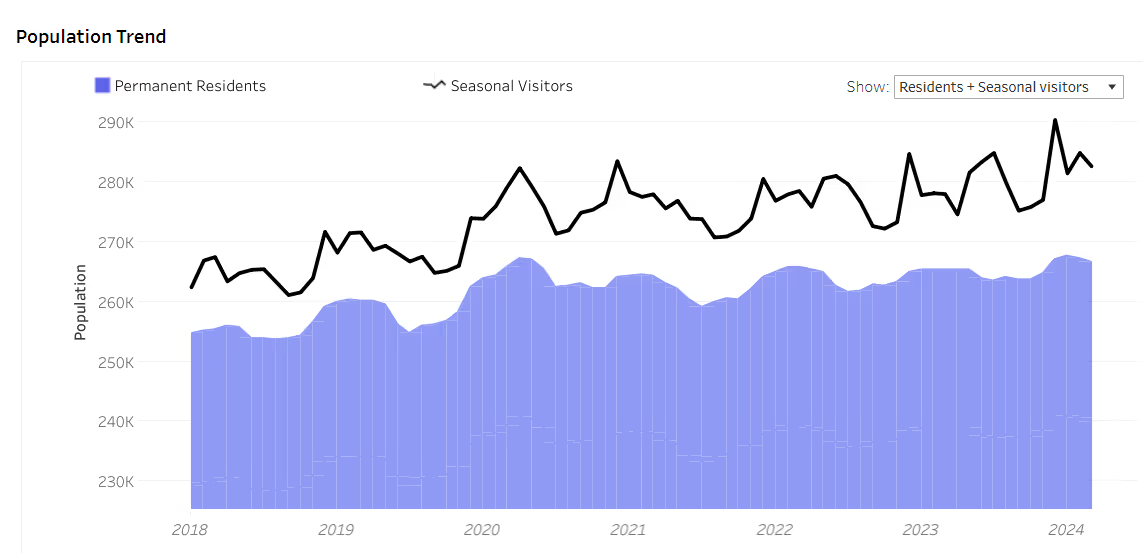

Migration may also be a factor in the increase of visits to the Scottsdale Performing Arts Center. Placer’s Migration Dashboard is noting an increase in both residents and seasonal visitors over the years.

How shifting consumer priorities are reshaping value perceptions across QSR, fast casual, and casual chains.

July 9, 2026

The New Definition of Value

As consumer sentiment hovers near historic lows and the cost of goods remains elevated, value has become a defining theme across the dining industry. Yet within the sector's diverse restaurant categories – and for individual brands – the question is no longer whether consumers are seeking value, but what value actually means. A closer look at chains across the industry suggests that, amid ongoing economic pressure, perceptions of value are evolving. For some consumers, value may be tied to affordability and promotions; for others, it may come from quality, convenience, or experience. The result is a market with multiple paths to winning consumer traffic.

Dining Traffic Remains Unstable in 2026

After an uneven but largely resilient 2025, dining traffic in 2026 tipped into a sustained decline.

Monthly visits to the overall dining industry have trailed year-ago levels throughout 2026, with February standing as the lone exception. That month saw a 3.7% year-over-year (YoY) increase in visits, driven in part by comparisons to the period of initial tariff announcements in early 2025. But broader trends remained challenged, and May's 2.5% YoY decline marked the steepest monthly drop of the past twelve months as rising gas prices and weakening consumer sentiment appear to have added pressure to an industry already navigating a difficult environment.

Breaking Down the Industry

These headwinds, though, have not landed evenly. Across the dining sector, some segments have faced more intense pressure than others, with much of the divide coming down to how consumers are perceiving value against experience.

QSR’s Value Proposition Under Pressure From Grocery Stores & Superstores

Over the past several years, inflation and rising menu prices have gradually weakened a cost-based value proposition that has long been central to the QSR segment. More recently, elevated gas prices have added another deterrent, making a trip through the drive-thru a less compelling choice for some consumers.

Strong performance at grocery stores and superstores suggests that competition for share-of-stomach is increasingly extending beyond traditional restaurant rivals. With expanding selections of ready-to-eat and pre-prepared meals, these channels are offering consumers a combination of value, convenience, and quality that can increasingly match limited-service dining options. At the same time, ongoing pressure on household budgets appears to be driving more consumers toward lower-cost meals made at home, creating additional headwinds for the QSR segment.

Fine Dining and the Fast Casual Middle Hold Firm

Yet for many consumers, there is still a time and place for dining out, and in the face of mounting economic pressure, several dining formats have found foot traffic success. Fine dining has posted traffic growth in nearly every month of 2026, with March standing as the lone exception. That decline was likely influenced by a calendar shift, as March 2026 contained one fewer Saturday than March 2025 – a meaningful headwind for full-service restaurants given the outsized role weekends play in driving visits. The segment's sustained growth points to the resilience of higher-income consumers and the enduring appeal of premium, occasion-driven dining experiences.

Fast casual and casual dining have also proven relatively resilient. The fast casual category saw positive YoY foot traffic in every month of 2026 so far, while casual dining's performance has rebounded since the March calendar shift that likely weighed on YoY traffic. A second calendar shift in May 2026 led to an extra Saturday in the month, which likely helped the segment's overall trend. These trends suggest that both fast casual and casual dining occupy an increasingly attractive middle ground where value is defined as a combination of affordability and experience. At the same time, years of menu price hikes at QSR chains have altered the cost equation in fast casual and casual dining's favor, narrowing the price gap between fast food and more elevated dining formats. As that gap has narrowed, consumers may be placing greater emphasis on experience and quality when deciding where to dine.

Inside the Playbooks of Fast Casual Standouts

The balance between price and elevated experience has made fast casual a favorite for value in the dining industry in 2026. A closer look at two of the segment's largest players, CAVA, a relatively young concept, and Chipotle, a legacy chain navigating operational challenges, shows how brands can deliver on that value proposition in different ways and win in today’s dining landscape.

Chipotle Creates Value With LTO Experiences and Loyalty Perks

Chipotle's traffic trends in 2026 have improved compared to 2025, with the brand offering a clear example of how fast casual brands can create value by pairing menu innovation with loyalty perks.

Chipotle outpaced the broader fast casual category in YoY visits nearly every week of 2026 so far. And the graph below shows that the chain's strongest traffic gains tended to coincide with major menu launches and loyalty initiatives – a key component of its ongoing "Recipe for Growth" strategy.

The return of fan-favorite Chicken al Pastor in the week of February 9, 2026 helped drive a 16.6% YoY increase in visits. Two months later, the launch of "Rewards on Repeat" – a refreshed loyalty program offering freebies upon sign-up – generated the period's largest weekly traffic gain, with visits rising 18.2% YoY. And the introduction of Honey Chicken on April 28 provided another boost, as the chain continued to rotate limited-time protein offerings and give customers reasons to return.

These performance peaks suggest that Chipotle has been particularly effective at pairing menu novelty with loyalty perks to reinforce a value proposition anchored by quality and experience.

Chipotle's "Recipe for Growth" Drives Traffic With Loyalty and LTO Launches

Year-over-Year Change in Weekly Visits, Chipotle vs. Fast Casual, Jan.–Jun. 2026

ChipotleFast Casual

Dashed lines mark key Chipotle promotional launch dates. Week-of dates shown; launches may have occurred mid-week.

Share

Embed:

CAVA Expansion and Differentiated Dining Experience

If Chipotle illustrates the power of menu innovation and loyalty-driven engagement, CAVA highlights a different approach to creating value – one rooted in variety, customization, and a consistently differentiated dining experience.

CAVA's overall visits climbed well above 20% YoY in every month of 2026, a pace largely driven by aggressive unit expansion. Meanwhile, same-store visits, which measure traffic at locations open for at least twelve months, sustained positive YoY growth – evidence of genuine demand at existing restaurants alongside a rapidly growing footprint.

While Chipotle leans on limited-time offers, CAVA's growth rests on a consistent, customizable experience. A deep roster of proteins paired with a wide range of bases, dips, and toppings, gives the chain built-in variety that helps keep the concept feeling fresh. In addition, CAVA's Mediterranean-inspired menu offers flavors and combinations that are less easily replicated at home, helping the brand maintain a differentiated experiential value proposition and drive growth.

O Though Chipotle and CAVA are at different points in their evolution and have taken different paths to growth, both highlight the enduring appeal of fast casual's balance of value and quality. In a dining environment where consumers are increasingly weighing cost against experience, the segment's ability to deliver on both has helped make it one of the industry's strongest-performing formats.

Casual Chains Thrive On Everyday Value

Fast casual isn't the only dining segment benefiting from consumers' evolving perception of value. In 2026, several casual dining chains have found success by pairing accessible price points with the elevated experience of a sit-down meal.

Brands such as BJ's Restaurant & Brewhouse, Chili's Grill & Bar, Bonefish Grill, Cicis, and The Cheesecake Factory all posted positive YoY visit growth in multiple months this year, demonstrating that even in a challenging economic environment, diners are motivated when they feel they are getting more in return. These results are particularly notable given the impact of calendar shifts, which weighed on March 2026 comparisons – and provided a tailwind to May performance.

Unlike many fast casual chains, these brands have not relied heavily on a steady stream of limited-time offers to drive traffic. While menu innovation remains part of the playbook, promotions often serve as ticket builders or engagement tools rather than primary traffic catalysts. Instead, these successful casual dining chains have focused on creating everyday value that diners can depend on, narrowing the price gap between limited-service restaurants and full-service dining.

The result is a value equation that encompasses table service, a more relaxed dining environment, and a place to socialize or celebrate an occasion. In an environment where consumers are increasingly weighing cost against overall experience, that combination appears to be helping several casual dining chains maintain positive traffic momentum.

The State of Dining in 2026

Although dining traffic has softened in 2026, the industry's performance suggests that consumers have not stopped spending on restaurants altogether. Instead, they have become more selective about where they dine and what they expect in return.

Across segments, the strongest performers have found different ways to deliver value. For some brands, that means menu innovation, loyalty engagement, and differentiated experiences. For others, it means dependable affordability paired with the service and atmosphere of a sit-down meal. As economic pressures continue to shape consumer behavior, the data suggests that value is no longer defined by price alone, but by the balance of cost, convenience, quality, and experience.

Find out where Americans are moving in 2026, why they're relocating, and how developers, investors, and retailers can stay ahead of the trends.

June 18, 2026

The Geography of Domestic Migration

During the pandemic and its aftermath, Americans were on the move. Millions left expensive coastal markets for lower-cost destinations across the Sun Belt, while boomtowns such as Bozeman, Boise, and Austin struggled to keep pace with the influx of new residents.

That wave of relocation has since cooled, as return-to-office mandates, higher mortgage rates, and a shrinking affordability gap between coastal cities and many COVID-era hotspots have dampened the incentive to move. But even in a slower market, domestic migration remains one of the most powerful forces shaping local economies, housing markets, and consumer demand.

This report leverages AI-powered location analytics to examine the relocation patterns reshaping the United States in 2026 – where Americans are moving, the demographic and economic forces driving those decisions, and how retailers, investors, developers, and policymakers can respond to the opportunities and challenges created by these shifts.

Which major metros are attracting the most new residents? Which pandemic-era standouts have seen growth stall or reverse? And what factors best predict a large metro area's domestic migration growth potential in 2026?

Interstate Flows: Which States Gained and Lost Residents?

South Carolina and Delaware Set the Pace

The latest statewide migration data shows that the slower relocation pace observed in 2024 persisted into 2025. No state recorded net inflows or outflows exceeding 0.7% of its starting population. And while several smaller states continued to attract new residents at meaningful rates, none of the nation's six most populous states saw net in-migration exceed 0.2%.

Among those smaller states, South Carolina and Delaware led the nation with net in-migration equal to 0.7% of their populations, followed by Idaho (0.6%), Maine (0.5%), Tennessee (0.4%), and North Carolina (0.3%). For most of these states, migration accelerated relative to 2024, though Delaware's inflow rate moderated slightly and North Carolina held steady.

Despite their differences, these states tend to offer a similar mix of lifestyle amenities, relatively low congestion, and opportunities for growth. Many also benefit from business-friendly climates, favorable taxpolicies, or housing costs that remain attractive relative to the higher-cost markets from which they draw new residents.

Vermont Trails Behind

At the other end of the spectrum was Vermont, which saw the nation’s largest net outflow as share of population in 2025, losing 0.4% of its population to domestic relocation. The decline deepens a reversal that first emerged in 2024, when the state swung to a net loss of 0.2%, after attracting inflows of 0.8% and 0.5% in 2022 and 2023, respectively.

Vermont's reversal likely reflects a combination of factors, including return-to-office mandates and the waning appeal of remote work. Housing undersupply in the state may have alsocontributed, illustrating how important infrastructure investments are to sustaining migration gains over time.

South Carolina, Delaware, and Idaho Lead the Nation in Domestic Migration Growth in 2025

Net Domestic Migration as a Share of Each State's Starting Population, 2025

Net Migration by State

−0.4%0.0%0.7%

Top Migration Magnets

2024

2025

*Analysis for each year is from Jan. – Dec.

Share

Embed:

Florida Sees Accelerated Inflow as Legacy Exodus States Slow Losses

Among the nation's six most populous states, Florida was the only one to see accelerating net in-migration in 2025, attracting new residents equal to 0.2% of its starting population, up from 0.1% the year before. Texas, by contrast, slowed from 0.1% net in-migration in 2024 to essentially flat in 2025, highlighting the cooling of what was once one of the country's strongest pandemic-era migration magnets.

Meanwhile, the legacy "exodus" states continue to lose residents, but at a slower pace than in previous years. Illinois and California have seen their migration deficits steadily narrow, with further improvement in 2025. Between 2022 and 2025, Illinois moved from -0.8% → -0.2% → -0.2% → -0.1%, while California moved from -0.9% → -0.4% → -0.3% → -0.2%. And though New York has held steady at -0.2% over the past two years, this marks a significant moderation from 2022, when the state experienced net outmigration equal to 1.1% of its population.

Major Insights:

Smaller states dominated migration gains in 2025, led by South Carolina, Delaware, Idaho, Maine, Tennessee, and North Carolina.

Vermont posted the nation's largest outflow after attracting strong inflows just a few years earlier.

Florida was the only top-population state to see meaningful net in-migration in 2025.

Texas' migration boom continued to cool, with net in-migration falling to flat in 2025.

Outmigration from New York, Illinois, and California is slowing, but these states are still losing residents overall.

Zooming In: Net Migration Across Metro Boundaries

Statewide trends reveal important shifts, but a closer look at the nation's ten largest metropolitan areas suggests that broader interstate averages increasingly mask diverging local realities. Several metros are attracting residents through interstate domestic migration even when their states as a whole are experiencing little or no net migration growth.

Phoenix (+0.3%), for example, stood out as the nation's top-performing large metro in 2025, despite Arizona's absence from the list of leading migration destinations – with the majority of its inflow coming from out of state.

Dallas (+0.2%) ranked second, continuing its rebound from -0.1% in 2023 even as Texas' statewide migration gains cooled. Like Phoenix, Dallas drew a majority of its new residents from outside the state, underscoring its growing appeal as a national migration destination. Houston, meanwhile, moved in the opposite direction, falling from 0.1% net in-migration in 2023 to -0.1% in 2025. While it is too early to call this a sustained reversal, the divergence between the two metros may reflect Dallas's growing pull as a corporate magnet alongside rising housing costs and weather-related challenges in Houston.

Metro-level data also suggests that the pandemic-era "big-city exodus" narrative is continuing to fade. Los Angeles improved from -0.8% in 2023 to -0.3% in 2025, while New York held steady at -0.3% after improving in 2024. Even Miami (-0.6%), which ranked last among major metros despite Florida's continued statewide gains, saw its outflows moderate from 2023 levels. And while Illinois continued to post net outmigration, Chicago (0.0%) reached migration neutrality in 2025 after recording losses in both 2023 and 2024.

Major Insights:

Phoenix was the nation's top large-metro migration destination in 2025.

Dallas gained momentum while Houston lost ground, highlighting growing divergence within Texas.

Miami continued to post the largest outflows among major metros despite Florida's broader migration success.

The LosAngeles, Chicago, and the New York metro areas all saw migration losses ease.

Florida Dominates Large Metros

Despite Miami's struggles – and Florida’s relatively modest 0.2% inflow – a look beyond the top 10 large metros reveals that the Sunshine State is home to six of the nation's eight fastest-growing large metros nationwide.

Those top-performing metros, defined as CBSAs with 500K+ residents that added at least 0.8% of their population through net domestic migration over the past year, share a similar profile: lower housing costs, retiree appeal, suburban density, and an easy drive to a larger economic hub.

Much of the growth of these Florida metro areas, however, is being fueled from within Florida itself. While major out-of-state metros such as New York (6.1%) and Chicago (2.0%) remained important sources of new residents, nearly half of the net migration into Florida's top destination metros came from elsewhere in the state. In 2025, Miami (22.5%), Orlando (13.0%), Tampa (5.8%), and Naples (4.2%) together accounted for 45.5% of the net positive migration feeding these fast-growing markets.

Major Insights:

Mid-sized Florida metros dominate the national migration leaderboard.

Florida's migration pipeline is overwhelmingly driven by in-state movement.

The Affordability Factor

The migration flows feeding the nation’s fastest-growing large metros suggest that affordability remains a powerful driver of domestic relocation.

In 2025, seven of the eight top destination metros analyzed above had lower typical home values than their largest feeder markets. Lakeland–Winter Haven, FL, for example, had a typical home value of $313.4K in December 2024, compared with $404.9K in Orlando and $380.2K in Tampa – its two largest sources of net migration. Even North Port–Bradenton–Sarasota, FL – the most expensive Florida metro in this group – drew its largest share of net migration from the New York metro area, where home values are substantially higher.

The lone exception was Charleston–North Charleston, SC, whose largest source of net migration was Baltimore – a market with lower typical home values than the destination. Even in Charleston, however, affordability appears to have played a role. New York, a significantly more expensive market, ranked a close second in 2025, accounting for 6.5% of net positive migration into Charleston, just behind Baltimore’s 6.8%.

While housing costs are only one factor influencing migration decisions, the data suggests that households continue to gravitate toward markets where homeownership is comparatively more attainable than in the places they leave behind.

Most Top Migration Destinations Pull Residents From More Expensive Housing Markets

Typical Home Values* in Top Feeder Markets to Destination Hubs, 2025

Destination HubTop Feeder Market

*Typical home value based on Zillow Research’s Zillow Home Value Index (ZHVI) for Dec. 2024, immediately preceding the analyzed migration period (Jan.–Dec. 2025).

Share

Embed:

Major Insights:

Most high-growth metros attract residents from more expensive housing markets.

Relative affordability continues to be a primary driver of domestic migration.

Demographics Over Dollars

But as important as affordability is in explaining today’s domestic migration patterns, age appears to be an even stronger determinant of where people choose to relocate.

Among mid-sized and large metros (250K+ residents) experiencing significant population shifts – defined as gaining or losing at least 1.0% of their starting population through domestic migration over the past two years – households are increasingly moving toward older, more established communities.

The data reveals a clear negative relationship between migration performance and age differential – a metric calculated by subtracting the median age of the destination market from the weighted median age of its feeder markets. Negative values indicate movement toward older communities, while positive values indicate movement toward younger ones. In other words, the metros attracting the strongest migration inflows tend to be older than the markets sending them residents.

The data also shows a clear positive relationship between migration performance and retiree concentration. Metros with larger shares of residents aged 65 and older generally saw stronger migration gains over the past two years, while younger metros tended to attract fewer newcomers. This suggests that retiree-driven relocation has become an increasingly important driver of migration. At the same time, the influx of younger residents points to the broader appeal of these communities, which offer a mix of affordability, amenities, and lifestyle advantages.

Relocators are Gravitating Towards Older, More Established Communities – With Retirees Helping Fuel the Trend

Net Migration as Share of Starting Population, 2024–2025*

Net Migration vs. Weighted Age Differential

Net Migration vs. Share of Residents 65+

*Analysis includes metro areas with 250K+ residents and domestic migration gains or losses of at least 1.0% during the study period. Weighted Age Differential compares the destination market’s median age with the weighted median age of origin markets, with positive values indicating migration toward younger markets and negative values indicating migration toward older markets. Age data: Census ACS 2020–2024.

Share

Embed:

Major Insights:

People are moving to older, more established communities.

Markets with larger 65+ populations are attracting more domestic relocators.

The New Migration Map: Strategic Implications

The pandemic-era urban exodus is giving way to a more nuanced migration landscape. Large urban markets are stabilizing, while growth is increasingly concentrated in smaller states, secondary metros, and intra-state corridors. Affordability remains a powerful pull, but retirees, lifestyle considerations, and local market dynamics are also playing an increasingly important role in where Americans choose to live.

To capitalize on these shifts in 2026, civic leaders, commercial real estate (CRE) investors, retailers, and developers should:

Monitor smaller states gaining migration momentum. Among the nation's most populous states, only Florida saw (modest) net in-migration in 2025. By contrast, smaller states like South Carolina, Delaware, Idaho, Maine, Tennessee, and North Carolina continued to attract substantial inflow. Investors, retailers, and developers that monitor these patterns may be better positioned to identify emerging growth opportunities.

Invest ahead of growth. Vermont's reversal shows how important it is for housing supply and infrastructure to keep pace with demand. High-growth communities will also need the retail, healthcare, transportation, and service capacity required to support expanding populations.

Look beyond state-level narratives that can obscure local opportunities. Florida led the nation in fast-growing large metros even as Miami lost residents, while Texas saw Dallas gain momentum as Houston fell behind. Likewise, although Arizona was not a top destination state, Phoenix remained the nation's leading major metro for migration gains.

Treat states as migration ecosystems. In Florida, for example, domestic migration is increasingly redistributed across a network of interconnected metros – as costs rise in one market, residents shift to nearby alternatives. Tracking these spillover effects can help identify tomorrow's growth markets before they show up in the rankings.

Don't write off major urban markets. While New York, Los Angeles, and Miami continue to experience net outflows – and Chicago has yet to return to positive territory – migration losses have moderated substantially from their pandemic-era peaks. As these markets stabilize, investments in livability, affordability, and quality of life could help strengthen their long-term competitiveness and economic vitality.

Protect affordability as a competitive advantage. Across the nation's fastest-growing metros, migration flows continue to move from more expensive housing markets to less expensive ones. As demand rises, preserving attainable housing will be critical to maintaining the cost advantages that attract new residents and businesses.

Prepare for a retiree-driven demographic realignment. Older Americans are playing an outsized role in shaping domestic migration patterns, but the communities attracting them are increasingly appealing to a broader range of households as well. As these markets grow, demand is likely to increase for healthcare, recreation, hospitality, and housing, creating opportunities across a wide range of sectors.

Explore key signals guiding data-driven site selection from brands actively expanding their brick-and-mortar footprints.

May 21, 2026

Predicting The Next Best Location

Across segments, retail and dining expansions converge on a common set of priorities, including identifying markets with strong demand, ensuring alignment with target audiences, and leveraging local consumer behavior to drive synergy. Using AI-powered location intelligence, we analyzed five expanding brands and segments to uncover the core principles driving successful site selection.

1. Identifying Sustainable Growth in an Increasingly Saturated Market

Nationwide visits to coffee chains are up in 2026, with established brands and newcomers alike seeing their traffic increase as consumer headwinds lead some to shift their discretionary spend towards more affordable indulgences. But past visit growth does not necessarily indicate future opportunity – it may instead signal market saturation. Relying solely on overall visit trends to guide expansion could lead chains into highly competitive markets where existing supply already meets demand.

For example, analyzing traffic trends in 10 major metro areas where coffee visits increased year-over-year (YoY) in Q1 2026 reveals significant gaps between overall traffic trends and per-location demand. In some CBSAs, overall traffic growth significantly outpaced per-location traffic trends – suggesting that supply is already meeting (or exceeding) demand and limiting room for new coffee locations despite overall category growth. But in other metro areas, where overall visit growth appears smaller, per-location traffic is actually booming – indicating that the underlying demand is resilient enough to support additional coffee concepts.

These patterns highlight the importance of looking beyond topline growth to identify where true whitespace still exists.

Strategic Takeaways:

Relying solely on aggregate category performance can obscure regional white space. A market-level view may reveal opportunities for stronger returns in areas where consumer demand is gaining momentum.

Combining overall visit and visits per location data offers a more complete view of where demand is both strong and sustainable.

2. Ensuring Demographic Alignment on the Hyperlocal Level

Effective site selection matches both regional and local demographics to a brand’s target customer, supporting performance and reinforcing positioning. But even in well-aligned metros, results depend on site-level precision – locations where the trade area visitor profile most closely reflects the brand’s core audience are best positioned to drive incremental upside.

An analysis of Alo locations in the DC area suggests that the company is adopting this strategy. Within the already high-income metro area of Washington-Arlington-Alexandria, individual Alo Yoga stores are placed in centers that draw even more affluent visitors – maximizing the revenue potential of each location.

In fact, Alo's newest stores in the metro area – One Loudoun and Bethesda Row – drive traffic from households with higher median incomes than even the established area locations. This signals a clear focus on premium retail corridors and affluent consumer segments, which reinforces the brand’s positioning while capturing higher-spending customers at the site level.

Strategic Takeaways:

Beyond traffic potential, effective site selection requires a clear understanding of both regional and hyperlocal demographics, as well as the brand’s target audience.

As brands expand, aligning locations with core customer bases can drive success while reinforcing brand positioning.

3. Finding Retail Nodes With Complementary Visitation Patterns

Beyond driving traffic potential and demographic alignment, site selection should also ensure that a brand’s identity and operating model are well matched to the visitation patterns of prospective locations. Barnes & Noble offers a clear example. The company’s ongoing resurgence has relied in part on repositioning itself as a local cultural and social hub, with a stronger emphasis on local curation and community-driven events.

And analyzing Barnes & Noble’s 2026 openings shows a clear tilt toward centers with a higher share of local traffic than the chain average – supporting its shift away from a purely transactional retail model toward a more community-centric experience built around local curation, events, and repeat visitation. By prioritizing locally driven centers, the company’s site selection strategy not only captures relevant traffic but also reinforces its broader repositioning as a neighborhood-oriented brand.

Strategic Takeaways:

Site selection strategy should look to align a brand’s identity and operating model with real-world visitation patterns at prospective locations.

For brands leaning into local curation, choosing centers with predominantly nearby visitors may be the key to performance and preserving brand identity.

4. Understanding the Benefits of Competitor Proximity

Effective site selection recognizes that proximity to competitors can function as a demand driver, amplifying traffic rather than diluting it.

In practice, this often takes the form of clustering – deliberately locating near similar or complementary concepts to capture shared demand. Shake Shack provides a clear example. Analyzing the chain's store fleet shows that many locations sit near other QSR and fast-casual concepts, creating opportunities to capture dining-based traffic. At the same time, strong cross-visitation patterns indicate that these co-located brands share a common customer base, positioning the brand closer to consumers who are already likely to visit. And, at least for Shake Shack, this strategy appears to be working – traffic to the chain increased 19.9% YoY in Q1 2026.

Strategic Takeaways:

As in retail, co-tenancy in the restaurant space can be mutually beneficial – establishing a center as a dining destination, driving incremental traffic, and increasing a brand’s opportunities to win share-of-stomach.

Incorporating cross-visitation analysis into site selection helps pinpoint locations where target customers are already visiting nearby brands. Centers that already attract a brand’s overlapping customer base provide a stronger foundation for incremental growth.

5. Balancing Growth and Cannibalization Risk

Incorporating trade area analysis into site selection can also help determine whether a new location will generate new traffic or risk cannibalizing existing demand. Aldi, a rapidly expanding grocery chain, offers a relevant example.

The company opened a fourth Las Vegas store on S Decatur Blvd in October 2025, positioned between existing locations on W Craig Rd and S Rainbow Blvd, approximately eight miles from each. And analyzing the core trade area of each of the four Las Vegas locations indicated limited visitor cannibalization over the last six months, despite the stores’ close proximity. Only 6.2% and 7.6% of the S Decatur Blvd store’s trade area overlapped with the W Craig Rd and S Rainbow Blvd stores’ trade areas, respectively.

These findings show that there is no one-size-fits-all approach to store spacing – it varies by brand, category, and market. Analyzing a company’s existing store network alongside competitor density and overall demand can help determine how closely locations can be placed without hurting performance. In many cases – especially in high-frequency categories like grocery – markets can support stores that are closer together than expected.

Strategic Takeaways:

Site selection strategy needs to take into account local demand and visitation behavior typical of the category as a whole and of existing locations in particular.

Trade area analysis can reveal where a market allows for network densification without significant risk of visit cannibalization.

.svg)

.avif)