.svg)

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

0

0

0

0

----------

0

0

Articles

Guest Contributor

The Untapped Potential of Class-B Malls How are Class B malls evolving to meet the needs of today's consumer? We take a closer look.

Barrie Scardina & Richard Latella

May 6, 2025

4 minutes

Article

First Watch Traffic Continues to Climb Find out how First Watch performed over the past few months.

Shira Petrack

May 5, 2025

1 minute

Article

Warby Parker and Allbirds: Stabilization Trends Into 2025Find out how Warby Parker and Allbirds are faring thus far into 2025.

Bracha Arnold

May 5, 2025

3 minutes

Article

Resilience 5 Years Post-Covid: Spotlight on Victoria Gardens in Rancho Cucamonga, CAFind out what sets open-air shopping center Victoria Gardens apart from other shopping areas in the country.

Caroline Wu

May 2, 2025

3 minutes

Article

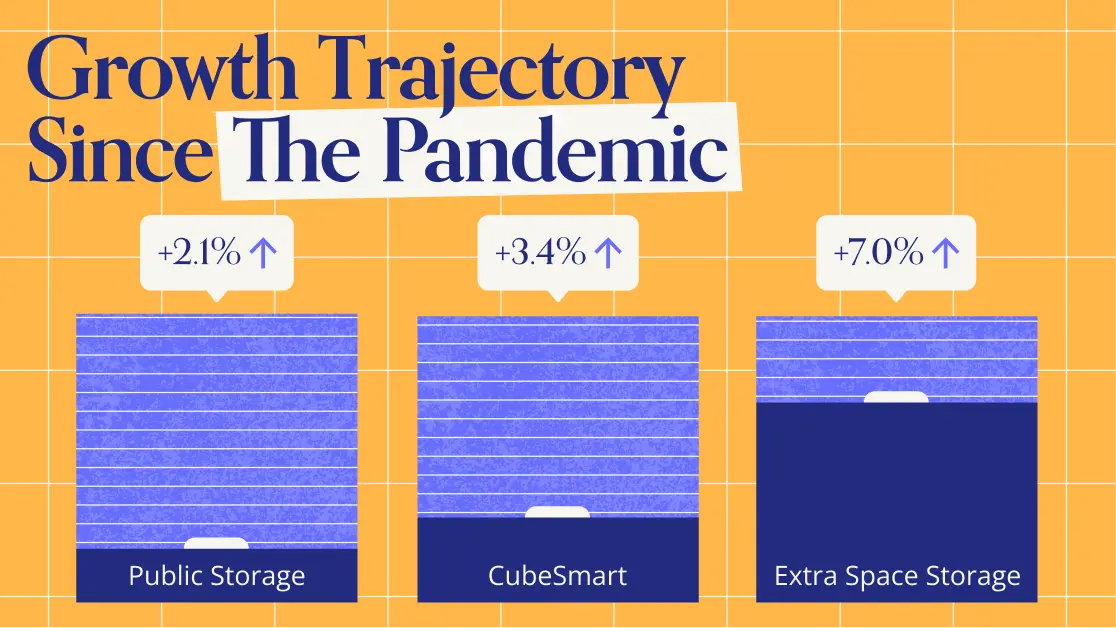

Self-Storage: Resilience in 2025Find out how the self-storage market has fared so far into 2025, and the audience segments behind the industry's growth.

Lila Margalit

Apr 30, 2025

3 minutes

Reports

.avif)

INSIDER

Report

The Forces Shaping Consumer Traffic in 2026Explore how higher gas prices, the search for value, and nostalgia-driven demand shaped consumer traffic and behavior in H1 2026.

July 27, 2026

.avif)

INSIDER

Report

Dining In 2026: All Roads Lead To ValueHow shifting consumer priorities are reshaping value perceptions across QSR, fast casual, and casual chains.

July 9, 2026

INSIDER

Report

Migration After the Boom: Where Americans Are Moving in 2026Find out where Americans are moving in 2026, why they're relocating, and how developers, investors, and retailers can stay ahead of the trends.

June 18, 2026

Show More

1 / 24

Loading results...

We couldn't find anything matching your search.

Browse one of our topic pages to help find what you're looking for.

For more in-depth analyses on a variety of subjects, explore Reports.

For more in-depth analyses on a variety of subjects, explore Reports.

INSIDER

Stay Anchored: Subscribe to Insider & Unlock more Foot Traffic Insights

Gain insider insights with our in-depth analytics crafted by industry experts

— giving you the knowledge and edge to stay ahead.