.svg)

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

0

0

0

0

----------

0

0

Articles

Article

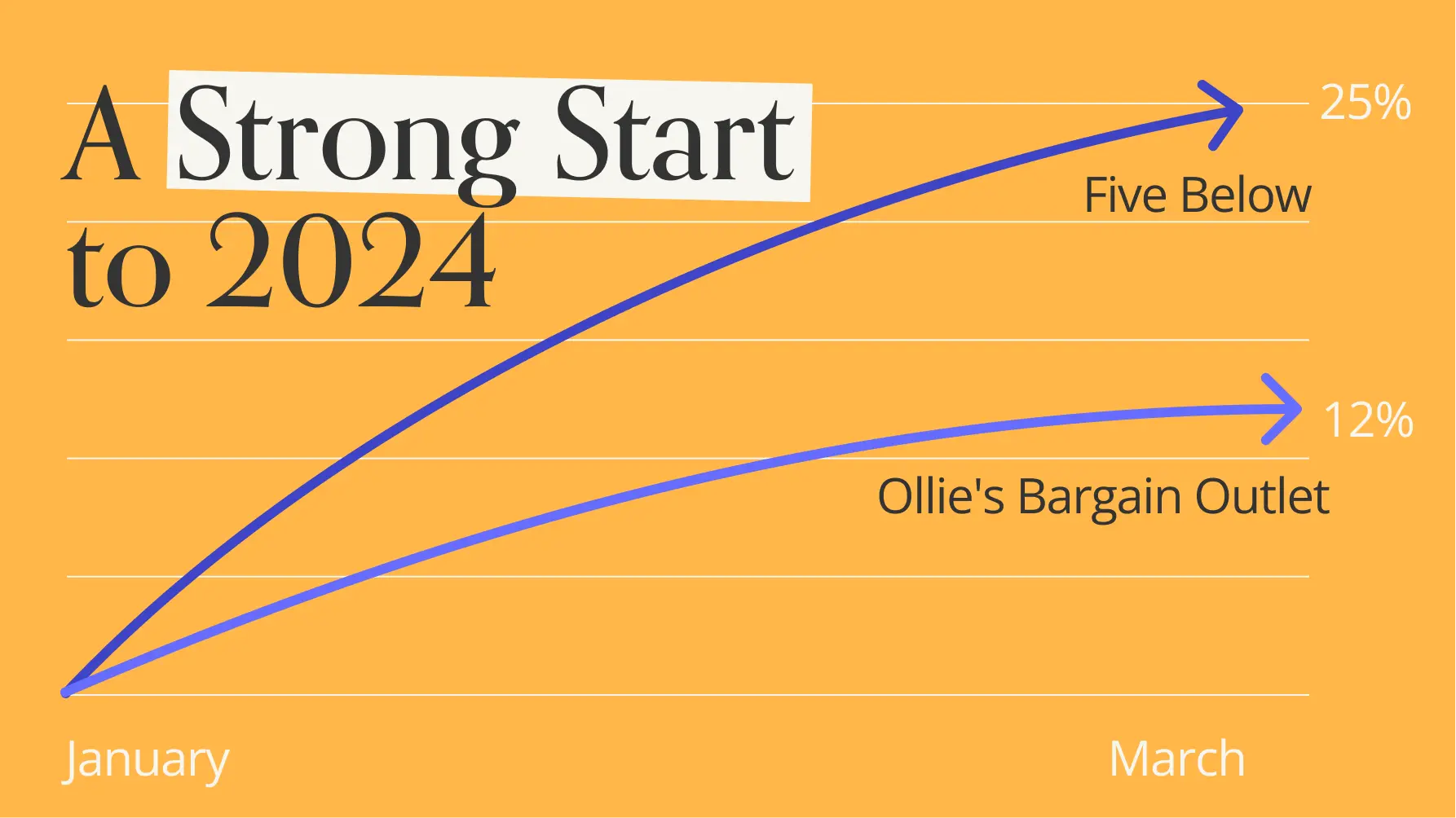

Ollie’s Bargain Outlet and Five Below: Q1 2024 Treasure TrovesFind out how specialty discount stores Ollie's Bargain Outlet and Five Below are driving visits in a challenging retail environment.

Ezra Carmel

May 27, 2024

3 Minutes

Article

Urban Outfitters: High Income, Specialty Fleets Still ThrivingElizabeth Lafontaine

May 24, 2024

Article

National Restaurant Association Show Takeaways: Who’s Winning the Food Fight?R.J. Hottovy

May 24, 2024

Article

Checking in With DICK’S Sporting Goods How is DICK'S Sporting Goods faring into 2024? Find out here.

Bracha Arnold

May 23, 2024

Reports

INSIDER

Report

Rethinking the Mall Anchor in 2025: A Visit-Focused Approach Discover how mall anchors are transforming in 2025 – and how a foot-traffic-focused approach to choosing key tenants can drive visits and shopper engagement.

May 29, 2025

8 minutes

INSIDER

Report

Grocery in 2025: Visitation Trends and Consumer BehaviorDive into the data to see the trends shaping the grocery space in 2025 and uncover actionable insights for strategic decision-making in the competitive food-at-home market.

May 15, 2025

8 minutes

INSIDER

Report

The Current Pace of the Fitness SpaceDive into the data to explore recent visitation patterns and consumer trends in the fitness space - and uncover potential keys to success, rooted in location intelligence.

May 5, 2025

8 minutes

Loading results...

We couldn't find anything matching your search.

Browse one of our topic pages to help find what you're looking for.

For more in-depth analyses on a variety of subjects, explore Reports.

For more in-depth analyses on a variety of subjects, explore Reports.

INSIDER

Stay Anchored: Subscribe to Insider & Unlock more Foot Traffic Insights

Gain insider insights with our in-depth analytics crafted by industry experts

— giving you the knowledge and edge to stay ahead.