Strategies for Retail Giants

Walmart, Target, and Costco are three of the most popular retailers in the country, drawing millions of shoppers through their doors each day. Each of these retail giants boasts distinct strengths and strategies that cater to their unique customer bases, allowing them to thrive in a highly competitive market.

This white paper takes a closer look at some of the factors that are helping the three chains flourish. How does Walmart’s positioning as a family-friendly retailer help it drive visits in its more competitive markets? How can Target leverage its reach to drive more loyal visits? And what does the increase in young shoppers frequenting membership warehouse clubs mean for Costco?

We dove into the location analytics to explore these questions further.

Year-Over-Year Visit Growth

Examining monthly visitation patterns for the three retail giants shows Costco’s wholesale club model leading the way with consistent year-over-year (YoY) visit growth – ranging from 6.1% in stormy January 2024 to 13.3% in June. Family favorite Walmart followed closely behind, seeing YoY foot traffic growth during all but two months, when visits briefly trailed slightly behind 2023 levels before rebounding.

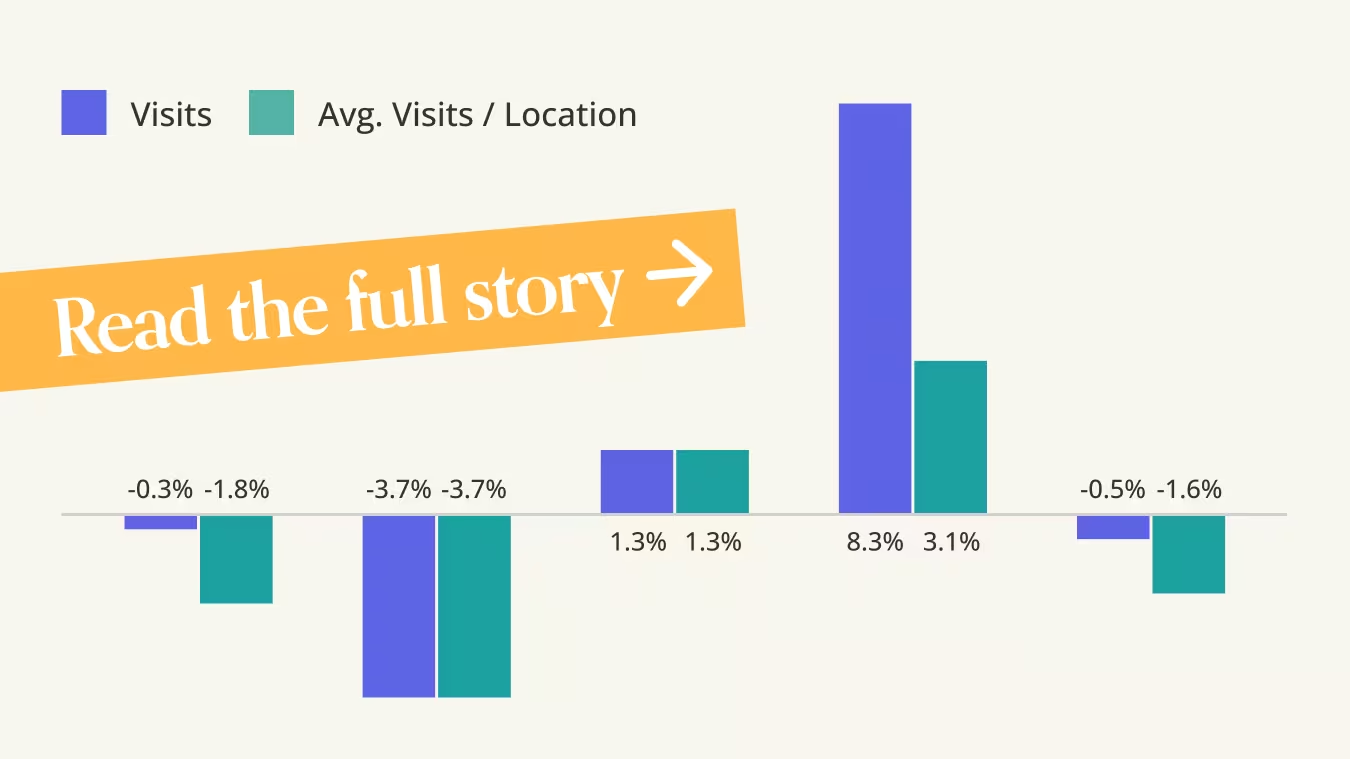

Target, meanwhile, had a slower start to the year, with visits trending below 2023 levels for most of January to April. Over this same period (the three months ending May 2024), Target reported a 3.7% decline in YoY comparable sales. But since then, things have begun to turn around for the chain, with YoY visits rising in May (2.5%), June (8.9%), and July (4.7%). This renewed visit growth into the second half of the year bodes well for the superstore – and the ongoing back-to-school season may well push visits up further as the summer winds down.

For all three chains, Q2 2024’s visit success has likely been bolstered in part by summer deals and intensifying price wars – as the retailers slash prices to woo inflation-weary consumers back to the store.

Changing Consumer Habits

Over the past few years, consumer behaviors have been changing rapidly in response to shifting economic conditions. This next section explores some of these changes at Walmart, Target, and Costco, to better understand what may be driving these shifts.

Less Mission-Driven Shopping – Except at Costco

One way that consumers have traditionally responded to inflation and other headwinds has been through the adoption of mission-driven shopping – making fewer, but longer, trips to retailers, so that every visit counts. Superstores and wholesale clubs, which offer one-stop shopping experiences, have long been prime destinations for these extended shopping trips. And even during periods when visits have lagged, these retailers have often benefited from extended dwell times – leading to bigger basket sizes.

A look at changes in average dwell times at Walmart and Target suggests that as YoY visits have picked up, dwell times have come down – perhaps reflecting a normalization of consumers’ shopping patterns. With inflation stabilizing and gas prices lower than they were in 2022 and 2023, customers may feel less pressure to consolidate shopping trips than they have in recent years.

In contrast, Costco’s comparatively long dwell times have remained stable over the past several years. The warehouse club’s bulk offerings, plentiful free samples, and inexpensive food court encourage shoppers to spend more time browsing the aisles than they would at other retailers. And even if mission-driven shopping continues to subside, Costco customers will likely keep on making extra-long shopping trips.

Increased Competition from Dollar Stores

While inflation is cooling faster than expected, prices remain high, and new players are stepping into the retail space occupied by Walmart, Target, and Costco – especially dollar stores. Though higher-income customers increasingly rely on the three retail giants for many of their purchases, customers of more modest means are often drawn to the rock-bottom prices offered at dollar stores.

And analyzing the cross-shopping patterns of visitors to Walmart, Target, and Costco shows that growing shares of visitors to the three behemoths also visit Dollar Tree on a regular basis. In Q2 2019, the share of visitors to Walmart, Target, and Costco who frequented Dollar Tree at least three times ranged between 9.8% and 13.7%. But by Q2 2024, that share rose to 16.7%-21.6%.

Dollar Tree is leaning into this increased interest among superstore shoppers. Over the past year, Dollar Tree added some 350 Dollar Tree locations, even as it shuttered nearly 400 Family Dollar stores. And the chain recently acquired the leases of some 170 99 Cents Only Stores – offering Dollar Tree access to a customer base accustomed to buying everything from groceries to household goods. As Dollar Tree continues to grow its footprint and expand its food offerings, the chain will be better positioned than ever to provide a real challenge to Walmart, Target, and Costco.

Still, the three retail giants each have unique offerings that distinguish them from dollar stores. This next section examines what sets Walmart, Target, and Costco apart – and how they can continue to strengthen their competitive edge.

Inside the Giants’ Playbooks

With competition on the rise, Walmart, Target, and Costco must display agility in navigating an ever-evolving market landscape. This section dives into the data for each chain’s more successful metro areas to see what factors are helping them outperform nationwide averages – and what metrics the retailers can harness to try to replicate these results nationwide.

Wealthier Visitors Drive Loyalty at Target

Target recently expanded its Target Circle Rewards program, rolling out three new tiers for its 100 million members. And this focus on loyalty has proven successful for the chain. Demographic and visitation data reveal a strong correlation between the median household incomes (HHIs) of Target locations’ captured markets across CBSAs (core-based statistical areas), and their share of loyal visitors in Q2 2024: CBSAs where Target locations’ captured markets had higher median HHIs also tended to draw more repeat monthly visitors.

Target’s captured markets in the Los Angeles-Long Beach-Anaheim, LA CBSA, for example, featured a median HHI of $89.8K in Q2 2024 – and 48.0% of the chain’s LA visitors frequented a Target at least twice a month during the quarter. Target stores in the Chicago-Naperville-Elgin, IL-IN-WI CBSA, where the chain’s captured markets had a median HHI of $88.7K in Q2 2024, also had a loyalty rate of 48.0%.

Target generally attracts a more affluent audience than Walmart. And even as the superstore slashes prices to attract more price-conscious consumers, the retailer is also taking steps likely to enhance its popularity among higher-income households. In April 2024, Target debuted a paid membership tier within its loyalty program offering perks like same-day delivery for a fee. Maintaining and expanding these premium offerings will be key for Target as it seeks to attract more affluent customers and replicate its high-performing results in CBSAs nationwide.

Costco’s Younger Audience

The persistent inflation of the past few years, while challenging for some retailers, has also created new opportunities – particularly for wholesalers. Membership warehouse clubs, including Costco, are gaining popularity among younger shoppers, a cohort often looking for new ways to stretch their more limited budgets. An October 2023 survey revealed that nearly 15% of respondents aged 18 to 24 and 17% of those aged 25 to 30 shop at Costco.

A closer look at some of Costco’s best-performing CBSAs for YoY visit-per-location growth highlights the significance of these younger shoppers: In H1 2024, the company’s YoY visit-per-location growth was strongest in areas with higher-than-average shares of young urban singles.

For example, the San Diego-Chula Vista-Carlsbad, CA CBSA experienced visit-per-location growth of 10.4% YoY in H1 2024, while the nationwide average stood at 7.9%. And the CBSA’s share of Young Urban Singles, defined by the Spatial.ai: PersonaLive dataset as “singles starting their careers in trade and service jobs,” was 12.1%, well above Costco’s nationwide average of 7.3%.

Walmart’s Family-Friendly Focus

Walmart is a one-stop shop for everything from affordable groceries to clothing to home furnishings, making it especially popular among families. The retailer actively courts this segment with baby offerings designed to meet the needs of both kids and parents, virtual offerings in the metaverse, and collectible toys.

And visitation data reveals a connection between the extent of different Walmart locations’ YoY visit growth and the share of households with children in their captured markets.

In H1 2024, nationwide visits to Walmart increased by 4.1% YoY, while the share of households with children in the chain’s overall captured market hovered just under the nationwide baseline. But in some CBSAs where Walmart outpaced this nationwide growth, the retail giant also proved especially adept at attracting parental households – outpacing relevant statewide baselines.

In Boston-Cambridge-Newton, MA, for example, Walmart experienced 5.0% YoY visit growth in H1 2024 – while the share of households with children in the chain’s local captured market stood 7% above the Massachusetts state average. And in Grand Rapids-Kentwood, MI, where Walmart’s share of parental households outpaced the Minnesota state average by an even wider 15% margin, the retailer saw impressive 7.3% YoY visit growth. This pattern repeated itself in other metro areas, suggesting that there may be a correlation between local Walmart locations’ visit growth and their relative ability to draw households with children.

Walmart can continue solidifying its market position by leaning into its family-oriented offerings and expanding its footprint in regions with growing populations of young families.

The Winning Retail Edge

Walmart, Target, and Costco all experienced YoY visit growth in the final months of H1 2024, with Costco leading the way. And though the three chains still face considerable challenges, each one brings unique strengths to the table. By continuously innovating and responding to changing market conditions, Walmart, Target, and Costco can not only overcome obstacles but also leverage them to reinforce their market positions and drive continued growth.

.svg)