.svg)

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

0

0

0

0

----------

0

0

Articles

Article

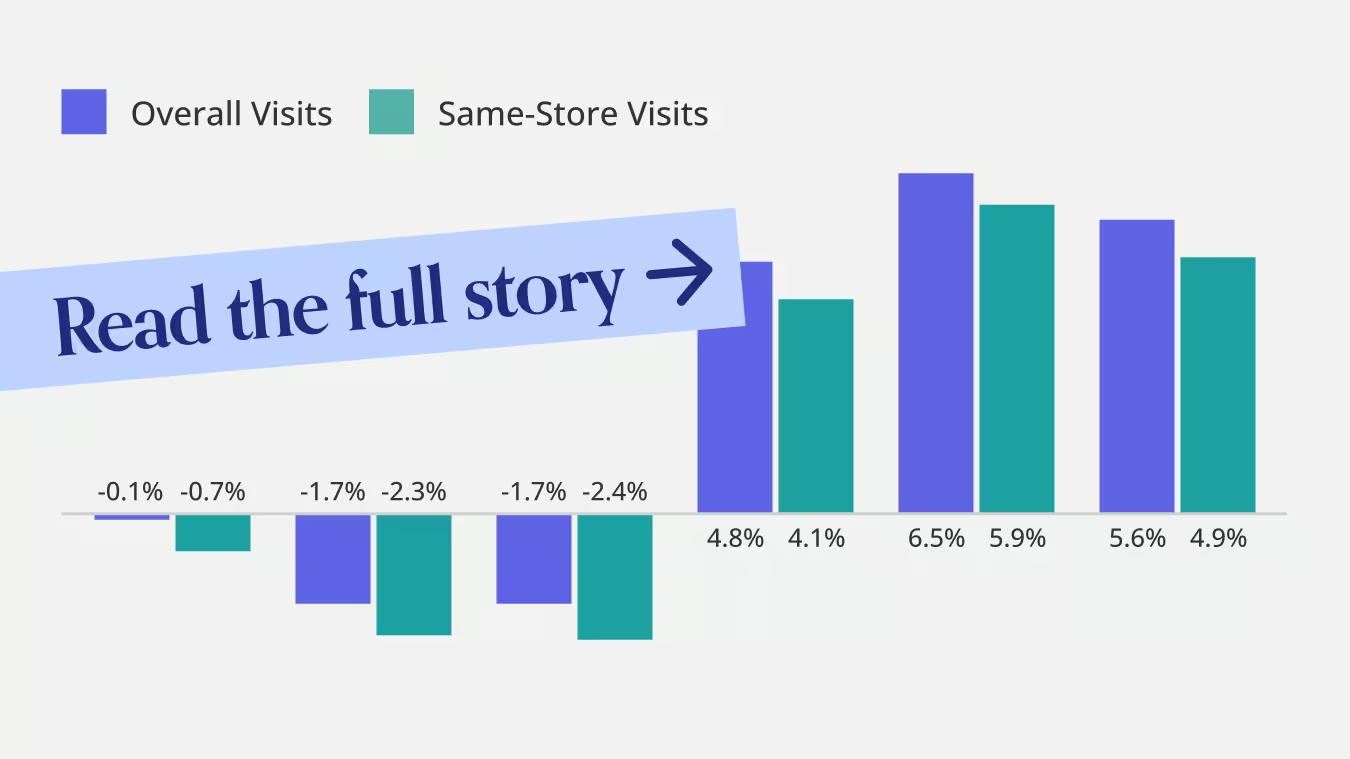

Chipotle’s Growth Is No Longer Just About New RestaurantsChipotle’s visit growth in 2025 was driven by expansion, but late-year data shows early signs of same-restaurant stabilization and faster pickup-driven visits gaining share.

Lila Margalit

Jan 22, 2026

3 minutes

Article

What Other QSR Brands Can Learn From McDonald’s Loyalty StrategyMcDonald’s ended 2025 with renewed visit momentum, driven in part by higher-frequency diners and its loyalty strategy. See what other QSR brands can learn about driving incremental growth through customer frequency.

Shira Petrack

Jan 21, 2026

3 minutes

Article

Opportunity vs. Operational Reality in Dollar Tree's 99 Cents Only AcquisitionDollar Tree’s 99 Cents Only lease acquisition reveals a smart real estate land grab complicated by cannibalization – but with long-term upside from a more affluent shopper base.

Shira Petrack

Jan 20, 2026

3 minutes

.avif)

Article

Which Gym Is Right For You in 2026?Using AI-powered location analytics, we reveal which gyms are less crowded at peak times, skew younger or older, and attract the most singles.

Ezra Carmel

Jan 16, 2026

4 minutes

Article

Placer.ai Overall Retail, E-Commerce Distribution, Industrial Manufacturing Index, December 2025Brick-and-mortar retail closed 2025 strong, with rising foot traffic across stores, logistics hubs, and a stabilizing manufacturing sector.

Shira Petrack

Jan 15, 2026

2 minutes

Article

PacSun Puts Gen Z in FocusAs Pacsun expands its physical footprint, location data reveals how the brand’s social strategy and creator partnerships are translating into Gen Z in-store visits.

Ezra Carmel

Jan 14, 2026

2 minutes

Reports

INSIDER

Report

2024 Holiday Lessons: Paving the Way for 2025 Dive into the 2024 holiday season retail and dining foot traffic data to uncover valuable insights for holiday success in 2025.

January 9, 2025

9 minutes

INSIDER

Report

The Local Economic Impact of Major Sports Events: Insights from the Copa América in Atlanta, GADive into the location intelligence analysis of the Copa América Games in Atlanta, GA, to find out how major sporting events impact local economies in general and the hospitality segment in particular.

January 2, 2025

6 minutes

INSIDER

Report

2024 Migration Trends: The Continued Draw of Mountain StatesFind out how affordable living, economic opportunities, and lifestyle appeal are transforming Idaho, Nevada, and Wyoming into top relocation destinations.

December 2, 2024

7 minutes

Loading results...

We couldn't find anything matching your search.

Browse one of our topic pages to help find what you're looking for.

For more in-depth analyses on a variety of subjects, explore Reports.

For more in-depth analyses on a variety of subjects, explore Reports.

INSIDER

Stay Anchored: Subscribe to Insider & Unlock more Foot Traffic Insights

Gain insider insights with our in-depth analytics crafted by industry experts

— giving you the knowledge and edge to stay ahead.