Article

Aldi & Lidl's Winning FormulaA strong value proposition has never been more important to shoppers – and discount powerhouses like Aldi and Lidl are prime examples. We took a closer look at some of the location intelligence to see where the two grocers stand.

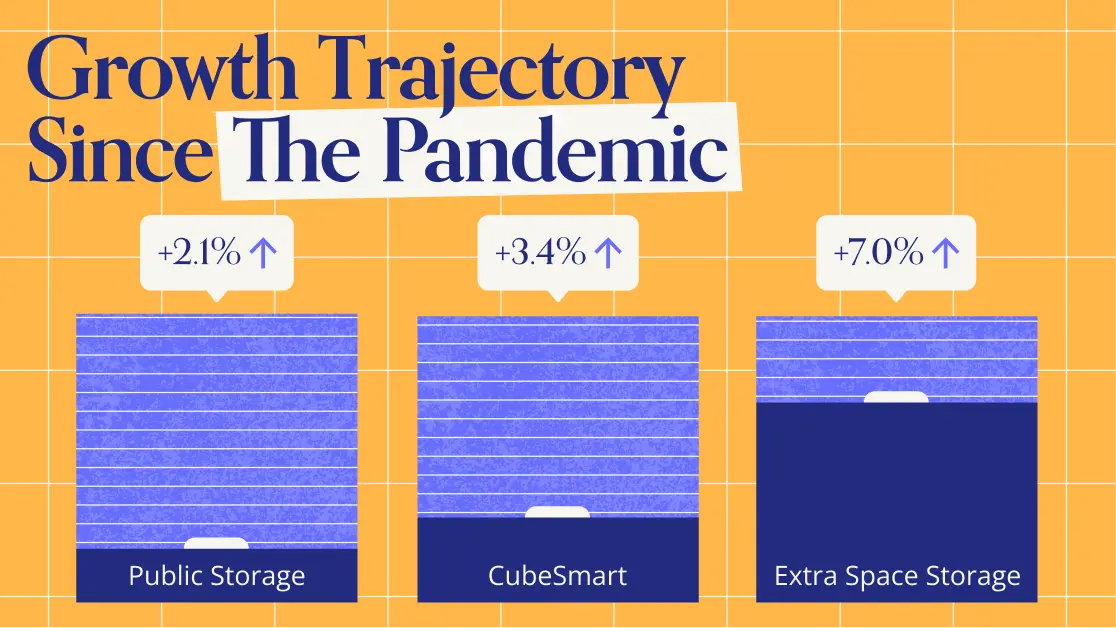

Visit & Visit per Location Growth

Aldi and Lidl have firmly established themselves as discount powerhouses. The two German retailers entered the United States market at different times, with Aldi opening its first location in 1976 and Lidl making its way stateside in 2017 – and diving into the foot traffic shows that both are thriving.

In the first quarter of 2025, visits to Aldi and Lidl saw significant year-over-year (YoY) increases of 8.9% and 4.2%, respectively – well above the industry-wide average (0.9%.)

Aldi, which has been on an expansion tear for the past few years, saw a YoY increase in average visits per location – but so did Lidl, which has been slower to add new locations. And this growth – 4.7% at Aldi and 1.9% at Lidl – highlights that their stores, whether new locations or already-existing ones, are driving sustained demand.

The Weekend Rush

A closer look at visitor behavior offers valuable insights into the factors driving the foot traffic success of Aldi and Lidl.

A significantly larger proportion of Aldi and Lidl's visits – 37.2% and 37.7%, respectively – took place on Saturdays and Sundays compared to visits to traditional and value grocery stores. This suggests that the attractive price points offered by Aldi and Lidl position them as prime destinations for shoppers making weekend stock-up trips.

Expansion Against Discount & Value Segments

On a chain level, both Aldi and Lidl are finding their own paths to success. Aldi is currently undergoing a significant growth phase, aiming to operate 800 stores by the end of 2028. This ambitious trajectory includes adding at least 225 new locations in 2025 alone – and examining the visit distribution across Aldi's largest markets provides valuable insights into how its strategy is unfolding. Contextualizing Aldi’s performance against the wider grocery segment provides a birds-eye view of the value grocer’s performance.

Over the past few years, Aldi has consistently increased its visit share when compared to the overall grocery segment, both nationally and across its major markets. For instance, in Florida, one of Aldi’s largest markets, its visit share grew from 4.8% in Q1 2022 to 7.0% in Q1 2025. And in Illinois, now its second-largest market, Aldi increased its visit share from 12.2% to 14.8% over the same period.

This consistent growth in visit share underscores the broad appeal of Aldi's value proposition to shoppers across the country, suggesting that its ambitious expansion plans are likely to be well-received by consumers.

Lidl’s Suburban Potential

Lidl also plans to grow its store count, though at a more modest pace than Aldi. And the chain is focusing on its already-existing markets in hopes of entrenching itself further in areas where it already has strong brand recognition.

Geographic segmentation data from the Esri: Tapestry Segmentation dataset within Lidl’s potential and captured markets reveals promising insights into where the retailer might find its most receptive audiences. In its potential market – calculated by weighting each Census Block Group (CBG) within Lidl’s trade area according to population size – the share of visitors from "Suburban Periphery" areas was 41.5%. However, in its captured market, determined by weighting each CBG according to its share of actual visits to Lidl – so better representing its current visitor profile – this suburban segment constitutes a significantly larger 56.4%. Conversely, the proportion of visitors originating from "Principal Urban Centers" and "Metro Cities" was higher in Lidl’s potential market compared to its captured market.

These metrics strongly suggest that Lidl has more demand in the suburbs than it may realize – and as it expands, focusing on these areas might prove to be a winning strategy for the chain.

Limited Assortment, Major Visits

Aldi and Lidl are thriving, growing their audiences during a challenging economic climate.

Will visits to the two chains continue to increase throughout 2025? Visit Placer.ai to keep up with the latest data-driven grocery insights.

.svg)