.svg)

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

0

0

0

0

----------

0

0

Articles

Article

Convenience Stores: A Strong Start to the Unofficial Summer SeasonElizabeth Lafontaine

Jun 14, 2024

Article

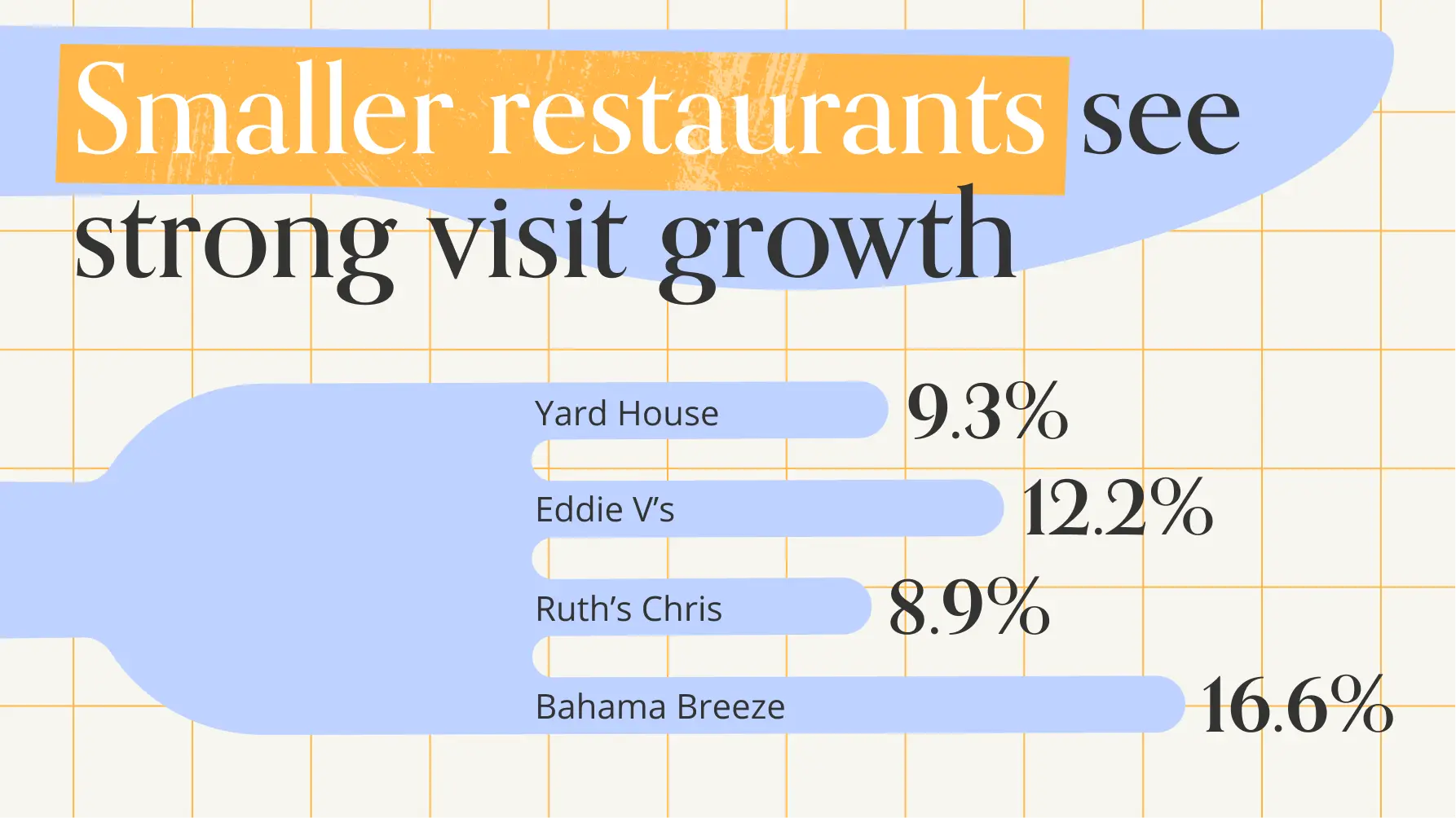

Digging Into Darden: Q2 2024 UpdateWe take a closer look at how Darden Restaurants, Inc.'s portfolio of restaurants is doing as Q3 2024 approaches.

Bracha Arnold

Jun 13, 2024

3 minutes

Article

TRU and avid: Midscale Hotels on the Rise Find out who is staying at midscale hotel chains TRU by Hilton and avid hotels.

Bracha Arnold

Jun 11, 2024

3 minutes

Article

Diving Into Kroger: A Strong Start to 2024 Find out how Kroger's wide portfolio of grocery stores is performing in 2024.

Samuel Roche

Jun 10, 2024

3 minutes

Reports

INSIDER

Report

Office Attendance Drivers in 2026: The New Rules of Showing UpDive into the data to learn how convenience-driven behaviors are impacting the office recovery – and how stakeholders from employers to office owners and local retailers can best adapt.

February 5, 2026

INSIDER

Report

Five Ways Retailers Can Leverage AI Without Losing What WorksRead the report to learn how AI is changing store roles, operations, marketing, and fleet strategy – and how to apply it without undermining what already works.

January 29, 2026

INSIDER

Report

10 Top Brands to Watch in 2026Meet the ten retail and dining powerhouses, including H-E-B, Walmart, and Dave’s Hot Chicken, redefining success and winning consumer loyalty in 2026.

January 12, 2026

Loading results...

We couldn't find anything matching your search.

Browse one of our topic pages to help find what you're looking for.

For more in-depth analyses on a variety of subjects, explore Reports.

For more in-depth analyses on a variety of subjects, explore Reports.

INSIDER

Stay Anchored: Subscribe to Insider & Unlock more Foot Traffic Insights

Gain insider insights with our in-depth analytics crafted by industry experts

— giving you the knowledge and edge to stay ahead.