.svg)

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

0

0

0

0

----------

0

0

Articles

Article

Thrift Store Visit Growth Outpaces Apparel as Tariffs LoomThrift store foot traffic has been on an upward trajectory since COVID – outpacing the wider apparel space. Discover how sustainability, savings, and in-person appeal fuel secondhand’s boom.

Lila Margalit

Sep 3, 2025

3 minutes

Article

America’s Parks Are Calling: Later, Longer, BusierAmerica’s local parks are busier and changing. Discover how visits are shifting – including seasonal patterns, visitor behavior and demographics.

Maytal Cohen

Sep 2, 2025

4 minutes

Article

How Economic Realities Are Redefining Vegas TourismDiscover how rising costs are reshaping Las Vegas tourism. Explore visit slowdowns, shifting demographics, and strategic buffers for growth.

Bracha Arnold & Lila Margalit

Aug 29, 2025

4 minutes

Article

Nordstrom Anniversary Sale: An Event that Continues to Find Success Amid ReinventionSee how the 2025 Nordstrom Anniversary Sale outperformed previous years by shifting away from influencer-driven marketing, and attracting wealthier, older consumers.

Elizabeth Lafontaine

Aug 28, 2025

5 minutes

Article

Manufacturing Visits Drop Post-Tariff ImplementationPost-tariff implementation, manufacturing site visits decline. Businesses adjust supply chain strategies and work through inventory.

Lila Margalit

Aug 28, 2025

1 minute

Article

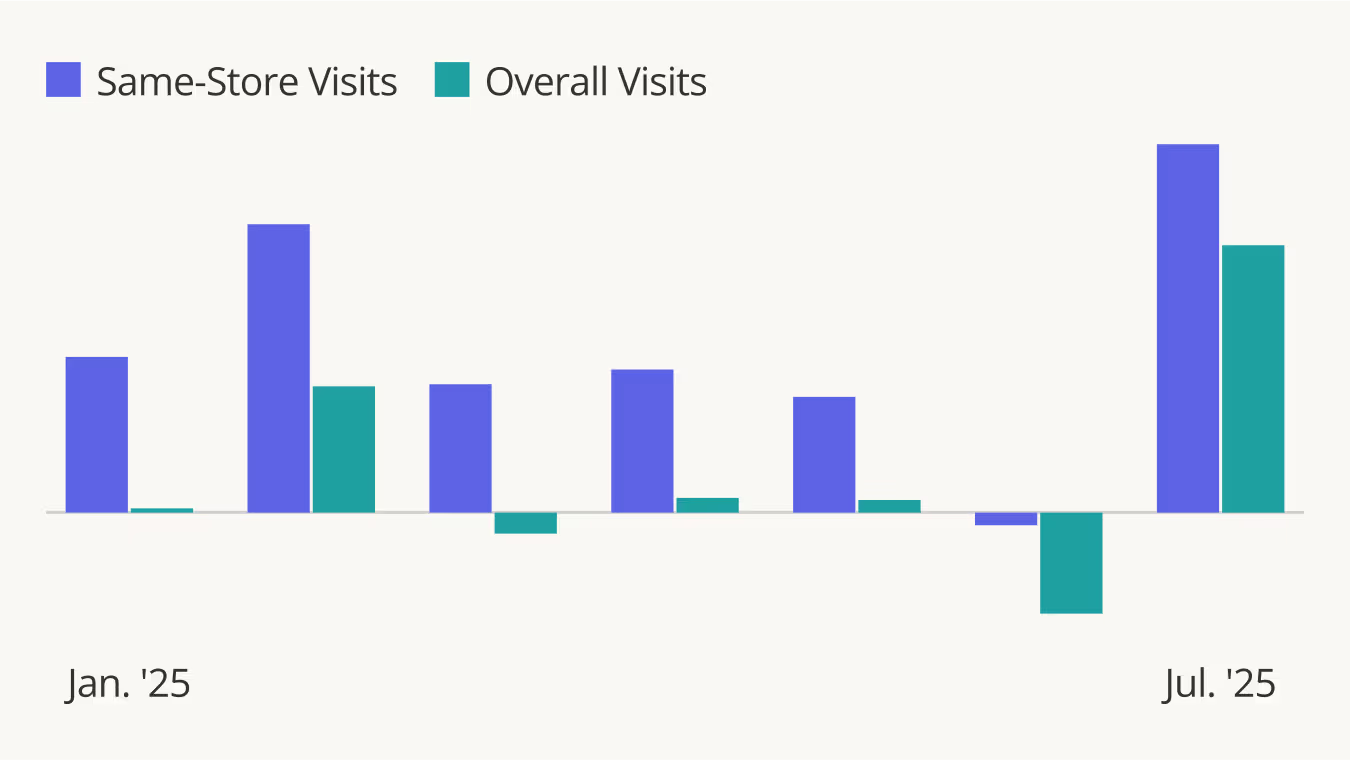

Semi-Annual Sale Drives Visit Surge For Bath & Body Works Bath & Body Works' semi-annual sale drove traffic surges in July 2025 following a decline in same-store visits in Q2 2025.

Bracha Arnold

Aug 27, 2025

1 minute

Reports

.avif)

INSIDER

Report

The Forces Shaping Consumer Traffic in 2026Explore how higher gas prices, the search for value, and nostalgia-driven demand shaped consumer traffic and behavior in H1 2026.

July 27, 2026

.avif)

INSIDER

Report

Dining In 2026: All Roads Lead To ValueHow shifting consumer priorities are reshaping value perceptions across QSR, fast casual, and casual chains.

July 9, 2026

INSIDER

Report

Migration After the Boom: Where Americans Are Moving in 2026Find out where Americans are moving in 2026, why they're relocating, and how developers, investors, and retailers can stay ahead of the trends.

June 18, 2026

Show More

1 / 24

Loading results...

We couldn't find anything matching your search.

Browse one of our topic pages to help find what you're looking for.

For more in-depth analyses on a variety of subjects, explore Reports.

For more in-depth analyses on a variety of subjects, explore Reports.

INSIDER

Stay Anchored: Subscribe to Insider & Unlock more Foot Traffic Insights

Gain insider insights with our in-depth analytics crafted by industry experts

— giving you the knowledge and edge to stay ahead.