The Challenge

The Outcome

Gain hands on experience with the data

Meet our advisors to learn more about Placer

Dive into the data to see how convenience stores are faring in 2023 and explore key trends shaping the future of the c-store industry.

Read White PaperWith clean, shiny venues, ever-expanding product selections, and built-out menus rivaling those of quick-service restaurants (QSRs), today’s c-stores are a far cry from the establishments of days gone by. Gasoline and other car services remain an important part of the convenience store business model. But the c-stores have also emerged as attractive destinations in their own right – places to grab a specialty coffee, get a quick dinner, or pick up a few grocery items on the way home from work.

This white paper dives into the data to identify key trends shaping the c-store industry in 2023. How have c-stores fared in the face of rising gas prices – and how does their performance compare to that of overlapping categories like fueling stations, grocery stores, and fast-food restaurants? Which brands dominate the highly competitive c-store space, and when do their locations attract the most visitors? (Hint: it starts with “s” and ends with “ummer”). Do customers interact differently with standalone c-stores than with locations that boast car services? And what can be learned from the customer journeys of shoppers that frequent different c-store chains?

Convenience stores have done remarkably well in recent years. Year over year (YoY), c-store visit growth outpaced some related categories, including grocery. And though the sectors’ YoY gains fell behind those of the coffee and QSR segments, this appears to be due largely to convenience stores’ already-stellar 2022 performance. When comparing visits to 2019, c-stores hit it out of the park with a 15.9% foot traffic increase – leaving coffee and QSR, which maintained respective 1.7% and 5.0% year-over-four-year (Yo4Y) visit gaps, in the dust. And notably, c-stores have also outperformed gas stations. (More on this below.)

C-stores’ rising popularity appears to be driven, in part, by inflation: When prices are high, people seek out inexpensive, affordable luxuries that don’t break the bank. And over the past several years, c-stores have upped their prepared food games, offering affordable fresh coffee and baked goods and introducing more varied fast-food fare. Rather than go on big, expensive grocery runs, some consumers may have preferred to pop into a local c-store, where they could grab a few essentials and treat themselves at the same time.

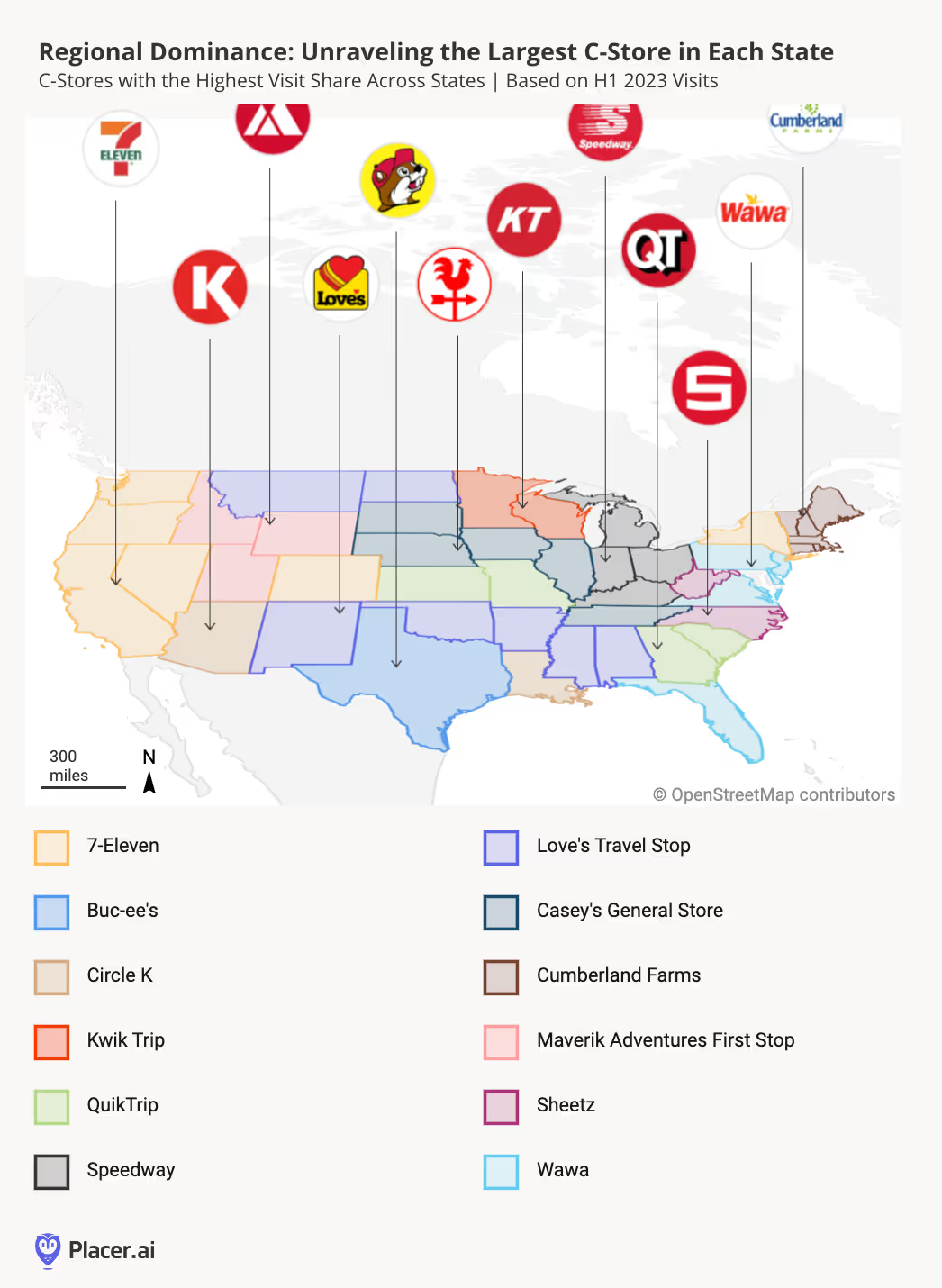

Like grocery chains, convenience stores are a highly localized affair. Every region of the country has its favorite go-to mini-mart, from Casey’s in the Midwest to Buc-ee’s in Texas. Indeed, while 7-Eleven remains America’s largest convenience store chain – boasting nearly 9,500 venues across 38 states and territories – the c-store landscape is a varied one, with visit share distributed among several leading brands.

To identify the most popular c-stores in different regions of the country, we analyzed the statewide visit shares of leading chains during the first half of 2023. On the West Coast, as well as in Hawaii, New York, Colorado, Nevada, and Washington, D.C., 7-Eleven reigns supreme – while Speedway, also owned by 7-Eleven, prevails in Alaska and in parts of the Midwest. But in Idaho, Wyoming, and Utah, Maverik – a brand that has positioned itself as a prime destination for people engaged in outdoor activities – has emerged as the local favorite. New England, for its part, is Cumberland Farms country, and in Florida, Maryland, Pennsylvania, Virginia, and New Jersey, people can’t get enough of their local Wawa. Several other chains, including Love’s Travel Stops & Country Stores, Sheetz, Circle K, and others, top statewide visit rankings nationwide.

Given how closely associated c-stores are with car services, the finding that convenience stores have thrived despite dwindling visits to gas stations may seem surprising. So to explore the evolving relationship between the two, we charted monthly visits to each segment, comparing them to a January 2019 baseline – and a striking pattern emerged. Since 2019 – and with the exception of the early months of COVID – both categories experienced highly correlated seasonal visitation patterns, with peaks in the summer – especially in July – and dips in winter.

But while c-stores and gas stations followed relatively similar growth trajectories in 2019 and 2020, by March 2021 their paths began to diverge. As skyrocketing gas prices put a damper on visits to fueling stations, foot traffic at convenience stores trended sharply upwards. This divergence highlights the growing demand for c-stores as independent entities, rather than gas station side shows.

But what drives these unmistakable seasonal trends? Why do people visit convenience stores more in the summer than in the winter?

Some of this seasonality is undoubtedly fueled by increased demand for cool treats like 7-Eleven’s signature Slurpee in the sweltering summer months. Regionally speaking, colder northern states generally experienced greater summer peaks than warmer states like Florida and California.

But looking at differences between individual brands suggests that there are additional factors at play. Topping the seasonality rankings was Buc-ee’s, the Lone Star State’s cult favorite, which drew a whopping 79.2% more visits in July 2023 than in January 2023. With 45 massive venues across seven states – most of them in Texas – and arguably the best bathrooms in America (apparently, they’re so clean you can eat off the floor), Buc-ee’s has emerged as a top travel stop for locals and tourists alike. And the chain’s low-priced food, friendly, well-paid staff, and whimsical vibe – complete with a buck-tooth beaver mascot – position it firmly as an attraction in its own right.

Maverik, another recreation-oriented c-store, came in a close second, with July foot traffic 70.6% higher than winter levels. Known for its “Adventure’s First Stop” slogan and action-themed decor, Maverik has carved out a niche as the perfect place to load up on supplies while conquering the great outdoors. And Maverik’s own-label BonFire food line makes the chain a prime refreshment stop for area residents as well as visitors to Mountain state attractions like Yellowstone National Park.

Given c-stores’ outsize performance, it may come as no surprise that industry leaders from Wawa to Buc-ee’s have been gripped by “expansion fever,” building new stores and seeking out additional ways to grow their footprints.

Against this backdrop, the c-store space has seen a flurry of mergers and acquisitions in recent months. In 2020, 7-Eleven added Speedway to its family of brands. And in April 2023, Maverik moved to acquire Iowa-based chain Kum & Go – paving the way for the popular Mountain state brand to expand into the Midwest. The merger added nearly 400 venues to Maverik’s fleet, doubling its store count and giving it a foothold in eight additional states.

The merging of the two companies has also connected Maverik with new customer segments. To see how Kum & Go’s acquisition stands to broaden Maverik’s demographic reach, we analyzed the two chains’ captured markets* using geosocial data from Spatial.ai’s PersonaLive.

In the first half of H1 2023, Kum & Go shoppers were more likely to hail from less affluent rural and small-town households, while Maverik customers were more likely to be wealthy or upper-middle-class suburbanites. This very different positioning may be a product of Maverik’s unique recreational slant – and may also stem from the two chains’ varying geographical placements. Either way, by acquiring Kum & Go, Maverik is gaining access to a new customer base, presenting the company both with new challenges and with the exciting opportunity to grow and diversify its audience.

*A chain or venue’s captured market refers to the population residing in its trade area, weighted to reflect the actual share of visits from each Census Block Group comprising the trade area. Analyzing a chain’s captured market provides insight into its customer base – the people that visit the chain.

What are the implications of c-stores’ growing success? Does the fact that they’ve established themselves as independent grocery and QSR destinations mean they don’t need car services anymore? Should c-stores with fuel services ditch the gas stations and double down on standalone venues?

To examine the impact that car services have on c-store performance, we analyzed venues that boast car washes or fueling stations, and compared them to chain-wide averages. And the results show that despite c-stores’ growing role in the grocery and fast-food spaces, c-store chains have not shed their core identities as popular car service and travel stops.

7-Eleven, to take one example, has done well overall – with positive year-over-year (YoY) visit growth during every month of H1 2023. But 7-Eleven locations with car washes outperformed brand averages significantly throughout the first half of the year. In April 2023, venues with car washes experienced a whopping 12.6 times more foot traffic growth than the chain as a whole.

And while 7-Eleven’s 7REWARDS loyalty program has more than 80 million eager customers coming back for more, much of the c-store industry’s success is driven by impulse purchases made on the go. People stop for gas at the closest fueling station, or pass a store on the street, and run in to grab a snack for the way. C-stores seeking to grow their audiences need to draw on a healthy pool of these one-time visitors – shoppers who happen upon the brand as they go about their day and may become loyal fans in the future.

Analyzing visit patterns to 7-Eleven stores across multiple states shows that locations with gas stations consistently drew greater shares of one-time visitors in H1 2023 than the chain as a whole. This strongly suggests that a significant portion of customers visit these venues primarily for the convenience of their gas station amenities – highlighting the pivotal role car services play in helping c-stores reach new customers.

Still, the way consumers interact with c-stores is far from uniform. Some chains serve primarily as corner stores or mini-marts – places to go when you’ve run out of milk or need to snag a few ingredients for dinner. Other brands function more as travel destinations or highway rest stops – ideal spots to get caffeinated during long road trips, take restroom breaks, or get the kids something to finally stop all that fighting in the back seat.

One way of distinguishing between these two kinds of c-stores is to examine customer journey: Where do people go after they’ve visited the chain? Do they head home, or do they continue on to other retail destinations? Do customers treat the chain more as a corner grocery store or more as a travel rest stop?

Looking at the behavior of visitors to popular c-stores during the first half of 2023 shows that leading chains occupy different positions on the spectrum between mini-marts and travel stops – with most falling somewhere in the middle. On one end of the spectrum lies Love’s Travel Stop, which caters to truckers – offering the showers, vehicle care, and refreshments that drivers need on their long hauls. Visitors to Love’s behave very much like visitors to typical road stops (think Flying J Travel Center), with less than a quarter heading home after visiting the chain.

On the other end of the spectrum lie brands like Sheetz, Cumberland Farms, and Wawa – c-stores that people visit for a more varied blend of routine errands, quick bites to eat and fueling needs. About half of H1 2023 visitors to these chains returned home after stopping in. And in the middle are stores like Buc-ee’s and Maverik, which are geared towards travelers and adventurers, but have also established themselves as independent destinations.

C-stores have found success in what continues to be a challenging economic environment. By positioning themselves as inexpensive grocery and QSR venues, they’ve flourished even as high fuel prices kept gas station visits down. And as category leaders seek to expand and find new markets, the future of the industry will likely be defined by how they navigate their dual roles as food stops and car service providers.