The Challenge

The Outcome

Gain hands on experience with the data

Meet our advisors to learn more about Placer

Discover four metro areas where retail is thriving despite the wider macroeconomic challenges and find out the unique factors driving success in each region.

Read White PaperThe retail segment has experienced a dramatic few years. Visits to stores spiked in the second half of 2021 as shoppers engaged in revenge shopping – but the rally was short-lived as the Omicron wave of early 2022 followed by record gas prices and subsequent inflation hampered the burgeoning recovery. Still, consumer demand for in-person shopping remains strong – although foot traffic data indicates that brick-and-mortar retail performance in 2023 exhibits significant regional variations.

This white paper takes a closer look at four regions that exhibited strong year-over-year (YoY) retail growth between January and May 2023 to see what’s driving their recovery. We analyzed three CBSAs (core-based statistical areas) – New York-Newark-Jersey City, NY-NJ-PA; San Jose-Sunnyvale-Santa Clara, CA; and Washington-Arlington-Alexandria, D.C.-VA-MD-WV – as well as one region consisting of three additional CBSAs (the New Haven-Milford, Bridgeport-Stamford-Norwalk, and Hartford-West Hartford-East Hartford CBSA). The analysis leverages location intelligence to explore what the office recovery means for local businesses, where value-priced chains are succeeding, and how an influx of newcomers is boosting home improvement stores. The report also reveals where luxury shopping is thriving and how student populations can help drive brand awareness and growth.

Read on to discover what is helping these four regions thrive and how location analytics can help retailers tap into this success for their own cities.

Manhattan is the heart of the New York-Newark-Jersey City, NY-NJ-PA CBSA, capturing about a quarter of retail visits in its CBSA. And although the city was hard-hit by the pandemic – with many speculating that the Big Apple was “over” – Manhattan has made a strong comeback.

Foot traffic data so far into 2023 reveals that YoY visits to Manhattan offices have surpassed the nationwide average. This recovery, impressive in its own right, also seems to be helping drive retail visits up. May 2023 visits to retailers in the New York CBSA were down just 5.4% YoY, compared to an 8.2% YoY drop in retail visits nationwide.

Looking at the performance of specific Manhattan retail corridors (high street areas with a high concentration of shops) further emphasizes Manhattan’s strength. May 2023 visits to Times Square & 42nd Street, North 5th Ave., and the Flatiron retail corridors were 12.8%, 10.2%, and 13.8% higher than in May 2022, compared to just a 1.7% YoY visit increase in nationwide retail corridor visits.

The correlation between increased office occupancy and retail visits helps illustrate why a return to in-person work has been a priority for many cities. Office foot traffic can drive consumer spending, helping prop up both small and large businesses.

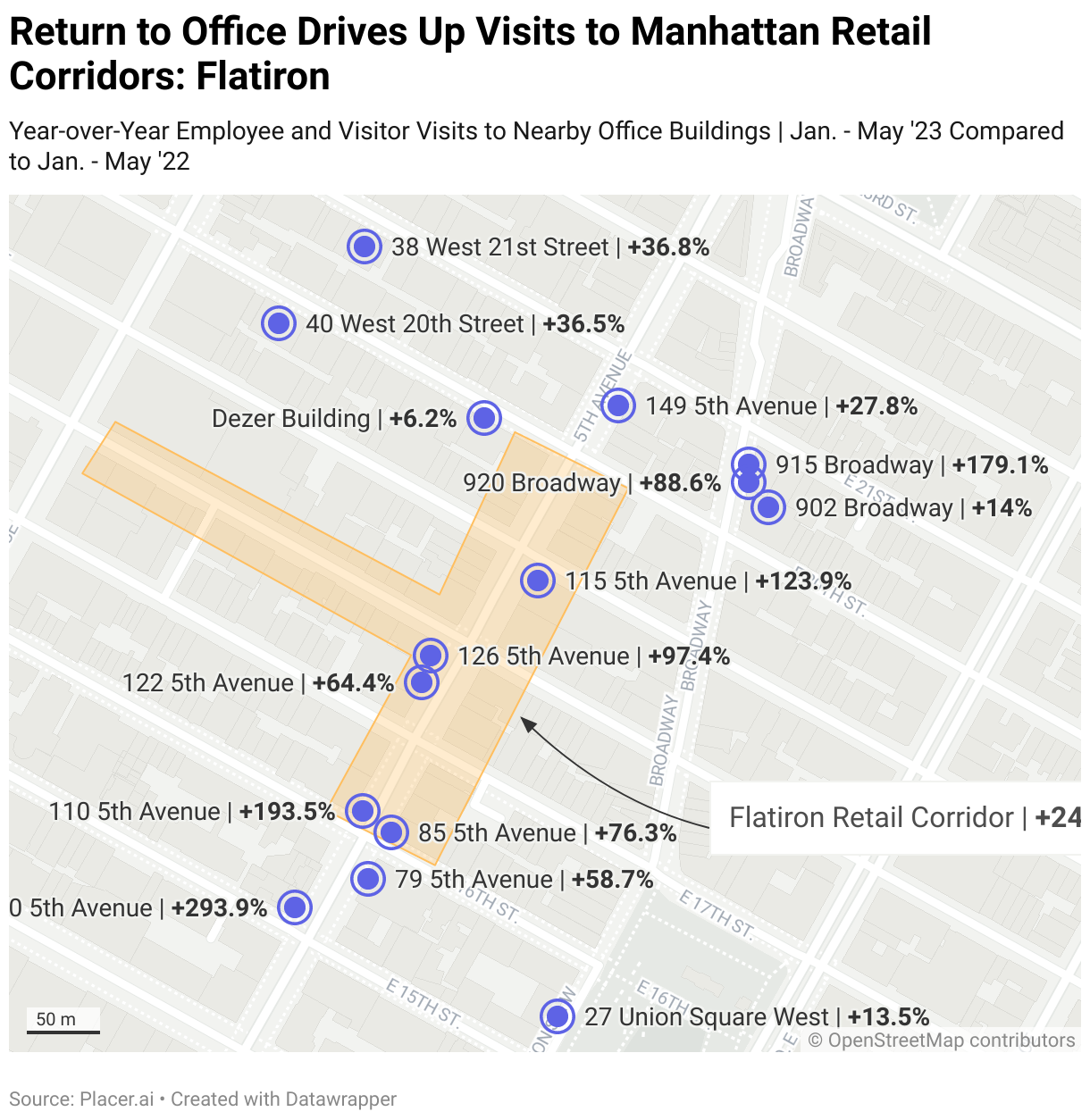

The Flatiron retail corridor, named for its iconic building, is home to a wealth of shops and office buildings. As workers returned to their offices – full-time or in a hybrid model – visits to local businesses followed.

A closer look at office buildings surrounding the Flatiron neighborhood highlights the symbiotic relationship between offices and retail visits. The retail corridor saw visits increase by 24.3% YoY between January and May 2023, and the office buildings surrounding the area also experienced impressive foot traffic growth.

Diving deeper into the visitor journey data for select Flatiron businesses further supports the connection between return to office and local retail performance. January – May 2022 and January - May 2023, the Flatiron retail corridor as a whole, as well as several stores within it, saw an increase in the share of visitors coming from work. As more employees return to in-person work, local businesses can once again rely on lunchtime or post-work visits to help drive sales and improve growth.

Manhattan's retail and office recovery reveal the important role that office blocks play in supporting local establishments.

On the West Coast, the San Jose-Sunnyvale-Santa Clara CBSA is thriving. The CBSA, nestled within the tech-heavy Silicon Valley, has seen its consumer activity remain strong during economic uncertainty.

So far into 2023, shopping centers in the CBSA outperformed their counterparts nationwide and within California on a YoY visit basis, suggesting that there is something in the valley keeping visits up.

A closer look at shopper demographics suggests that people frequenting these shopping centers come from higher-income trade areas than visitors to other California retail destinations. Between January and May 2023, 44.4% of the trade areas of San Jose-Sunnyvale-Santa Clara CBSA shopping centers consist of census blocks where the median HHI is over $200K/year. In contrast, during that same period, only 24.7% of trade areas of shopping centers in California consisted of census blocks with that HHI, and most – 27.5% – fell into the $50K to $100K/year bracket.

Perhaps unsurprisingly, then, high-end retailers are thriving in the region. Brands like Tesla, Williams-Sonoma, and Burberry are seeing impressively high YoY visits, particularly when put in context with the wider retail performance in California. Visits to Williams-Sonoma and Burberry decreased YoY by 2.3% and 3.4%, respectively, between January and May 2023 in California as a whole, but grew in the San Jose-Sunnyvale-Santa Clara CBSA. Similar patterns repeated across other luxury brands examined, indicating that these brands have set up within reach of a receptive audience.

The retail strength of the San Jose-Sunnyvale-Santa Clara CBSA highlights how understanding the spending capabilities of a given region and catering to that niche can lead to strong retail growth.

Connecticut became a go-to destination for New Yorkers during the pandemic. Despite a slight decrease in population from its peak in June 2022, the number of residents within the New Haven-Milford, Bridgeport-Stamford-Norwalk, and Hartford-West Hartford-East Hartford CBSAs was up by 1.2% in April 2023 compared to March 2019. Today, these three metro areas, collectively considered here, are seeing some of the strongest retail performance in the country.

The counties of Fairfield (Bridgeport), Hartford, and New Haven are also seeing an influx of newcomers from areas with higher median home values. An analysis of Zillow’s housing data layered onto Connecticut’s population change reveals a pattern of higher-income homeowners moving into more affordable areas. Among the top nine origin counties, only one – Hampden County – has a lower median home value ($305K) than its destination, Hartford County, where the median home value is $385K.

The combination of the shift from higher to lower HHI area and from areas more likely to see home rental than home ownerships indicates that these newcomers likely sold their higher-priced homes in their origin counties, and purchased new, more affordable homes in Connecticut – leading to an increase in disposable income available to spend at local retailers. And with a new house comes the motivation to undertake various home improvement projects – so, unsurprisingly, visits to local home improvement stores jumped along with the population.

Comparing home improvement foot traffic data to a March 2019 baseline of zero reveals a surge in visits to stores like Harbor Freight Tools and Ace Hardware. And while visits have moderated since 2021 – when counties first saw the major influx in newcomers and home improvement visits spiked nationwide – they still remain substantially and consistently higher than they were in March 2019.

The impact of these wealthier newcomers extends beyond the rise in foot traffic to home improvement stores. Analyzing the trade areas of home improvement retailers reveals that the median HHI in the trade areas of three out of the four major chains in the three CBSAs analyzed increased between Q1 2022 and Q1 2023.

The domestic migration to Connecticut and subsequent increase in home improvement visits and trade area median HHI highlights the positive impact that new residents can have on a region’s retail.

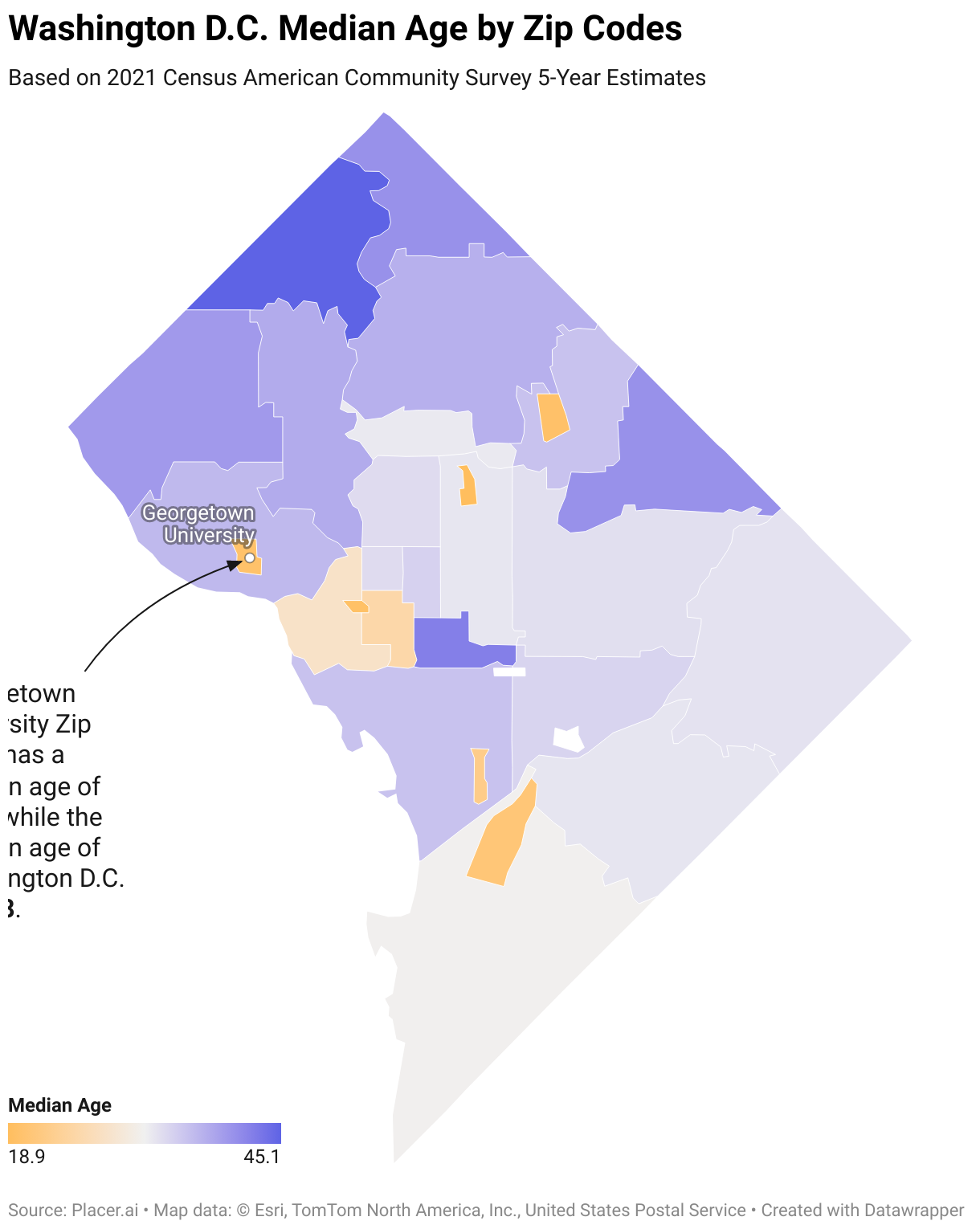

Diving into the retail data for the Washington-Arlington-Alexandria, D.C.-VA-MD-WV CBSA reveals that Washington, D.C. is becoming a magnet for direct-to-consumer (DTC) and digitally native brands (DNBs). DNBs typically establish their presence through online platforms, with some making the leap from digital to physical storefronts. And the Georgetown neighborhood in the nation's capital has emerged as an ideal location for these brands to test the waters of a brick-and-mortar format before expanding their presence to other cities.

Georgetown is home to the eponymous university and a vibrant community of young students and professionals. And perhaps unsurprisingly, the area around the university (depicted in light yellow) skews younger than other D.C. neighborhoods. This demographic composition creates an attractive opportunity for DNBs to establish their presence, as they can tap into a population of Internet-savvy students who are enthusiastic about exploring the physical stores of a favorite online brand.

Another benefit to establishing an experimental brick-and-mortar location in a neighborhood like Georgetown is that many of the residents are transient. With consumers under the age of 40 tending to prefer brands with a strong omnichannel presence, DNBs can effectively target a cohort that is particularly receptive to their products. And since many of the area’s shoppers are students who come to the city for a few years and move on – taking their brand preferences with them – the investment in Georgetown stores can boost these brands’ long-term nationwide performance.

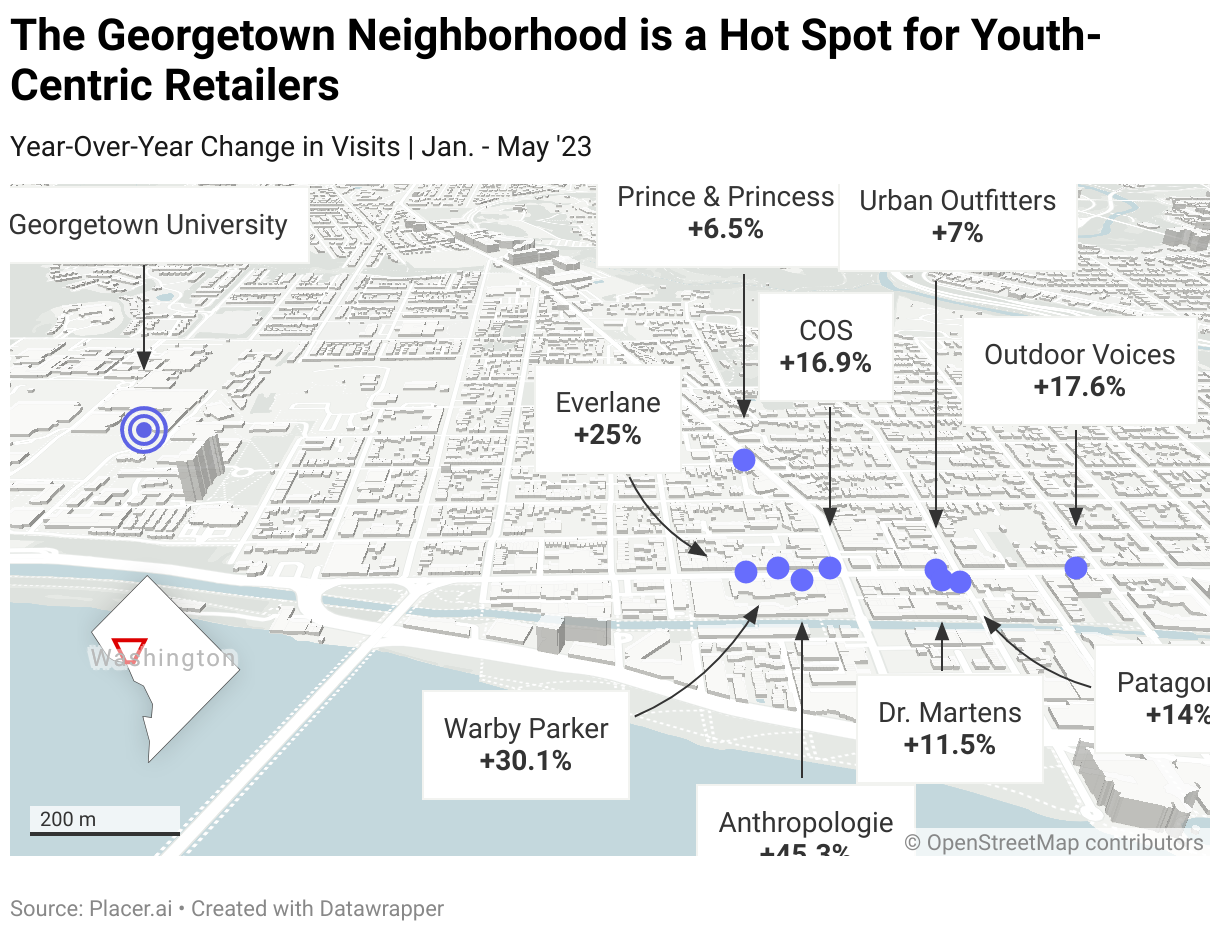

And aside from its role as a DNB launching pad, the Georgetown area experienced impressive YoY growth in retail visits, especially among brands popular with younger audiences, like Urban Outfitters (7.0%), Outdoor Voices (17.6%), and Dr. Martens (11.5%). Popular DNBs Warby Parker and Everlane also showed visit growth, with visits up 30.1% and 25.0%, respectively, for the two companies.

Younger consumers are a crucial demographic for retailers to capture, and brands that can establish themselves in student-heavy areas will be well positioned to continue leveraging a growing preference for omnichannel retail.

While the retail world has faced significant challenges in recent years, plenty of regional bright spots abound. From a symbiotic office-retail relationship to the importance of placing affordable and high-end chains where they are welcomed, adapting to local needs and preferences can drive retail success.