The Challenge

The Outcome

Gain hands on experience with the data

Meet our advisors to learn more about Placer

Read the report to find out how the grocery space is adapting to changing times, with immersive experiences, small-format stores, affordable alternatives and advertising innovations.

Read White PaperThe grocery segment demonstrated remarkable strength over the pandemic, with year-over-year (YoY) visits to the category increasing for much of 2020 and 2021. But inflation hit the category in mid 2022, and grocery visit growth began to slow down – even though traffic remained ahead of pre-pandemic levels. But YoY growth stalled, and by Q1 2023, YoY grocery visits were down almost every week.

Now, nearly halfway through 2023, location intelligence shows that grocery traffic is still lower than last year. And this contraction in grocery visits is not happening in a vacuum – retail visits in general have been on a downward trend over the past several months, with few sectors remaining unaffected by current economic headwinds.

Yet even within this challenging retail climate, plenty of bright spots can be found, with grocers well positioned to adapt to changing consumer behaviors. Some brands are relying on their attractively priced product mix to find success in spite of – or perhaps because of – rising prices. Other chains are doubling down on convenience by experimenting with smaller formats, while others are finding success by creating immersive shopping experiences. And some are leveraging their physical platforms for additional revenue streams by entering the advertising space.

This white paper dives into the latest location analytics to explore how the grocery segment is adapting to continued challenges and navigating a stormy economic climate.

As inflation drives out-of-home food prices up, value grocery formats are benefitting, with visits to discount grocers rising in the face of increases in food prices. In particular, discount grocery chains like Aldi and Lidl have been outperforming the overall grocery industry. These establishments tend to favor their private-label brands and carry a relatively restrained product selection, which allows them to reduce overhead costs and transfer these savings directly to shoppers through lower prices.

The traffic growth to discount grocery chains seems to correlate with the increase in food inflation.On the other hand, the higher-priced fresh format grocers, which carry a wider selection of products and offer a more upscale shopping experience, have been underperforming the wider grocery industry. And visits to these chains, which include Fresh Market and Natural Grocers, dipped significantly as U.S. food inflation rose. It seems, then, that during periods of high food inflation, consumers are likely to favor value-priced supermarkets to the detriment of more quality-focused grocery retailers.

Diving deeper into the visitation data indicates that the impact of rising prices extends beyond store choice – consumer behavior in the store itself also seems to be shifting. The COVID-19 pandemic saw the emergence of mission-driven shopping as consumers, mindful of potential health risks, adopted a more strategic approach to their grocery outings, leading to fewer, but more carefully planned excursions.

And while the pandemic may have officially ended, mission-driven shopping seems to be making a comeback – foot traffic data reveals an increase in median visit duration across several grocery chains. Simultaneously, the average visit frequency has dropped, with only one analyzed chain, Piggly Wiggly, seeing any year-over-year (YoY) increase in average visit frequency. This suggests that shoppers are approaching their grocery runs more carefully – perhaps planning them to coincide with sales and specials – while minimizing extra trips to help save on gas costs and stick to a newly-tightened budget.

With mission-driven shopping on the rise, the potential value of each shopping trip also increases. And to make sure consumers choose their chain for their longer, less frequent grocery runs, grocery chains may be looking to enhance the overall shopping experience

H-E-B, the grocery darling of Texas, recently unveiled a new store format on Lake Austin Blvd. in Austin, TX. This two-story grocery emporium is nearly double the size of H-E-B’s standard 50,000-square-foot store and includes a second-floor café and bar, indoor and outdoor seating, and a full-service pharmacy. Also on-site are several restaurants and an outdoor department for sprucing up a home garden. In deciding to invest in an immersive shopping experience, H-E-B is following in the footsteps of other grocers who have begun incorporating experiential offerings alongside more standard supermarket staples.

Recent foot traffic data indicates that consumers are responding positively and dedicating some of their leisure time to visit the new store. The new H-E-B saw a much higher share of weekend visits than other Austin-area H-E-B venues. In March and April 2023, 37.6% of visits to the Lake Austin H-E-B location took place over the weekend, compared to an average 33.8% share of weekend visits for other Austin DMA locations. Similarly, the median visit duration at the immersive H-E-B was 27.6% longer than that at its local counterparts in the wider Austin DMA.

H-E-B already attracts enthusiastic shoppers who come in to browse and enjoy the product selection – and now, it looks like the new store format is amplifying those trends. This strategic addition is providing customers with an enhanced shopping experience that extends beyond the bounds of traditional grocery and keeps shoppers coming back.

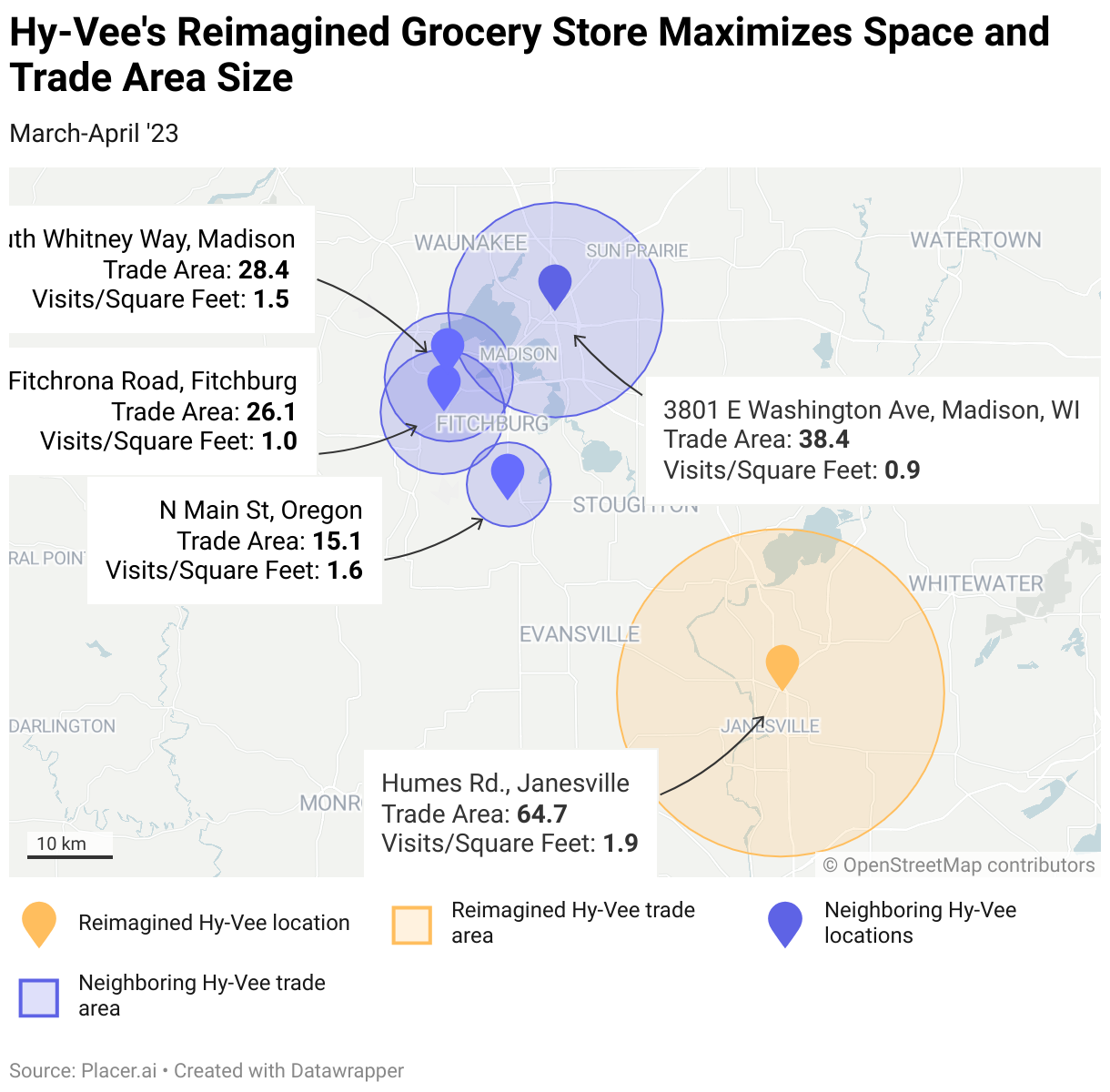

Beloved Midwestern grocery chain Hy-Vee is another brand that has recognized the power of offering more at the store. The company recently opened an extra large store in Janesville, WI. The new location, which spans nearly 97,000 square feet, boasts a floral department, a pharmacy, a gift shop, clothing options, eyewear, a shoe department, and an in-store Starbucks. The store is the sixth of its kind nationwide, and its broad range of products is positioning it to become a local hotspot.

Location intelligence reveals how customers are reacting to this new shopping mecca. The store sees a higher number of visits per square foot on average than neighboring Wisconsin Hy-Vee locations – 1.9 visits per square foot compared to a Wisconsin average of 1.5 visits per square foot. The new store also pulls visits from a larger trade area than comparable stores, with a True Trade Area size of 64.7 square miles compared to the Wisconsin Hy-Vee average of 47.3 square miles. These findings underscore the draw of the reimagined Hy-Vee location, providing an exceptional shopping experience that attracts more customers from farther away.

Going big is certainly one way to bring in customers, but good things also come in small packages. As real estate, construction, and labor costs continue to skyrocket, more and more grocery chains are pivoting to smaller-format locations that cost less to operate and make for a more efficient shopping experience.

Rochester, NY-based Wegmans introduced three smaller-format grocery stores – one each in Philadelphia, PA, Wilmington, DE, and Washington, D.C. – in 2022. While an average Wegmans can be as large as 140,000 square feet, the small-format locations cover about half of that, at approximately 80,000 square feet. The Delaware small-format store – also the first Wegmans in the state – is located near the Pennsylvania border within the Philadelphia DMA.

The store, which serves as the anchor of a mixed-use development, was met with enthusiasm upon its opening. And despite its size – the Wilmington, DE venue is around 40% smaller than the average Wegmans in the Philadelphia DMA – the store received more visits per square foot than other Wegmans in the Philadelphia DMA in Q1 2023.

Wegmans has long been a popular retailer with a dedicated customer base – and the grocer looks poised to continue its success with its small-format expansion.

Small-format locations do more than just use store space efficiently to increase visits per square foot – in some cases, larger chains can also use small-format venues to attract a specific consumer segment. Meijer, a family-owned, regional supercenter with nearly 240 stores across six states, also launched two grocery-centered smaller-format concepts called Meijer Grocery in early 2023. The two new stores, located in Michigan, are designed to offer a more convenient and personalized shopping experience, with a strong emphasis on fresh, locally sourced food and innovative technology.

The Meijer Grocery locations span around 75,000 to 90,000 square feet – hardly small by most standards – but significantly smaller than the average Meijer supercenter.

Analyzing the foot traffic data from February to April of 2023 shows that the trade areas for the two Meijer Grocery locations attracted a customer base from a trade area with a higher-than-average median household income (HHI). While the median HHI for Michigan Meijer trade areas ranged from $51K/year to $81K/year, the Meijer Grocery attracted visitors from trade areas with median HHIs of $90K/year and $103K/year.

The share of “Flourishing Families” – based on the Experian: Mosaic Consumer Lifestyle Segmentation – was also higher for both Meijer Grocery stores than neighboring Meijer supercenters. Meijer’s decision to locate these new grocery-focused stores in more affluent areas seems to be driving visits from local residents who may prioritize a more personalized and convenient shopping experience.

Retail media networks are poised to transform the advertising space, with the industry seeing around $40 billion invested in it in 2022. And, this number is only expected to grow – analysts predict that by 2024, the retail media industry will be worth $60 billion.

Over the past couple of years, more and more grocery chains have been tapping into the potential of retail media networks to increase and diversify revenue streams. As of Q1 2023, 22% of all grocery visits in the United States went to grocery chains that operate retail media networks – a share that is expected to grow as the format continues to evolve.

Sprouts Farmers Market recently announced its online retail media platform in partnership with popular online grocery delivery service Instacart, which launched a retail advertising product called Carrot Ads on its new Instacart Platform. Grocers can use Carrot Ads to monetize their owned e-commerce properties and build retail media networks without investing heavily in the technical infrastructure.

The strategic partnership between Sprouts and Instacart should benefit both companies by combining Instacart's well-established advertising platforms with Sprout's customer base. It also presents an opportunity for consumer packaged goods (CPG) companies to target specific segments within Sprouts’ online customer base by leveraging Sprouts’ first-party data.

Still, most grocery shopping continues to take place in person, so chains that leverage the massive advertising platforms created by a physical store fleet and build omnichannel retail media networks will get the most out of this emerging format. And location intelligence, which provides visibility into the shopping habits and preferences of brick-and-mortar consumers, makes offline retail media networks just as data-driven and effective as their online counterparts.

Were Sprouts to incorporate its brick-and-mortar fleet into its retail media network offline, location intelligence could provide granular data on the demographic and psychographic segments that visit each store. For example, the AGS: Behavior and Attitudes dataset could be combined with True Trade Area analysis to reveal which locations attract visitors with a higher-than-average interest in dogs or organic food. This information could help retailers and marketers better tailor their in-store advertising and reach the right consumer segments with the right ads directly at the point of purchase.

For now, it looks like the grocery sector’s growth streak is on hold as inflation continues squeezing budgets – although food inflation does appear to be easing, which may bring visitors back to the space. In the meantime, grocery chains that understand what their customers are looking for in 2023 can adapt their offerings and adjust their stores to cater to shifting consumer habits. By analyzing purchasing preferences, shifts in consumer behavior, and demographic attributes of shoppers, grocery chains can continue giving their patrons what they want. And by expanding beyond their core business to provide more experiences alongside grocery products and to create new revenue opportunities through retail media networks, grocers can continue seeing strength even during grocery downtimes.